2021 guide for non-EU B2C sellers and marketplaces

How the largest, most fundamental overhaul of the European Union’s VAT could impact your business

STEP

01

Introduction

STEP

02

A single EU VAT return for ecommerce

STEP

03

Closing the low value consignment stock loophole

STEP

04

EU and non-EU marketplaces become the deemed supplier

STEP

05

Conclusion

STEP

01

Introduction

STEP

02

A single EU VAT return for ecommerce

STEP

03

Closing the low value consignment stock loophole

STEP

04

EU and non-EU marketplaces become the deemed supplier

STEP

05

Conclusion

01

Introduction

02

A single EU VAT return for ecommerce

03

Closing the low value consignment stock loophole

04

EU and non-EU marketplaces become the deemed supplier

05

Conclusion

STEP 01

Making compliance easier and fraud harder

After July 1, 2021, member states of the European Union (EU) will introduce sweeping reforms to the VAT obligations of B2C ecommerce sellers and marketplaces.

The key reform will allow some sellers to report all their Pan-EU distance sales on a single VAT return in just one member state instead of having multiple VAT registrations across the EU. The aim is both to boost cross-border online trade and promote trade across the EU’s digital single market by reducing compliance obligations.

The changes also seek to tackle the €7 billion ecommerce VAT fraud gap, with member states looking to close import loopholes and obligate online marketplaces to collect VAT in place of sellers (deemed supplier rules).

Three fundamental changes to ecommerce EU VAT

This guide provides an overview of the three major reforms planned for 2021 and discusses how the reforms will affect sellers and marketplaces’ obligations. Post-Brexit, the U.K. implemented its own version of these reforms beginning January 1, 2021. You can review Avalara’s separate guide on this topic .

A single EU VAT return for ecommerce

When the reforms take effect, existing distance selling threshold rules will be withdrawn.

The reforms will be accompanied by the rollout of a single EU VAT return, One Stop Shop (OSS). Sellers shipping goods from one or multiple EU member states to customers across the EU may opt to use OSS to report their Pan-EU sales.

OSS will replace the current requirement that sellers VAT register in each country. OSS is an extension of the 2015 Mini One Stop Shop (MOSS), which successfully tested allowing sellers to file a single EU return for B2C sales of digital services (streaming media, ebooks, apps, etc.).

Implications

After July 1, 2021, some ecommerce sellers within the EU will be able to close their foreign VAT registrations. Instead, they can complete an OSS return in just one EU member state tax authority.

Non-EU sellers, including those in North America, can also use OSS. They must register with a single member state to file an OSS return for their B2C sales of goods within the EU.

NOTE: Sellers holding inventory in warehouses in other EU states will have to remain foreign VAT registered following the 2021 reforms. This includes sellers using the Fulfillment by Amazon (FBA) program. There will be exceptions for sellers using marketplace facilitators (see section 4).

A single EU VAT return for ecommerce

When the reforms take effect, existing distance selling threshold rules will be withdrawn.

The reforms will be accompanied by the rollout of a single EU VAT return, One Stop Shop (OSS). Sellers shipping goods from one or multiple EU member states to customers across the EU may opt to use OSS to report their Pan-EU sales.

OSS will replace the current requirement that sellers VAT register in each country. OSS is an extension of the 2015 Mini One Stop Shop (MOSS), which successfully tested allowing sellers to file a single EU return for B2C sales of digital services (streaming media, ebooks, apps, etc.).

Implications

After July 1, 2021, some ecommerce sellers within the EU will be able to close their foreign VAT registrations. Instead, they can complete an OSS return in just one EU member state tax authority.

Non-EU sellers, including those in North America, can also use OSS. They must register with a single member state to file an OSS return for their B2C sales of goods within the EU.

NOTE: Sellers holding inventory in warehouses in other EU states will have to remain foreign VAT registered following the 2021 reforms. This includes sellers using the Fulfillment by Amazon (FBA) program. There will be exceptions for sellers using marketplace facilitators (see section 4).

Closing the import VAT exemption loophole

After July 1, 2021, the €22 VAT exemption on low value parcels imported into the EU for delivery to customers will be withdrawn.

This exemption has been exploited by many sellers mistakenly or deliberately under- declaring the import values of goods to avoid VAT. Under the new rules, VAT can now be charged at the point of sale for transactions up to the value of €150.

The VAT charged may then be declared and paid via a new submission, the Import One Stop Shop (IOSS). This process is designed to create an efficient green channel customs clearance

Implications

After July 1, 2021, EU sellers will no longer have a disadvantage on price, as all sellers will have to charge VAT on all imported goods.

EU sellers can opt to register for IOSS in just one EU state to declare the VAT on any affected imports on shipments €150 or less.

However, non-EU sellers will be required to register for IOSS or use an intermediary registered for IOSS in one EU member state. There are instances where a facilitating marketplace (see EU and non-EU marketplaces become the deemed supplier), or delivery service may step in to report and pay the VAT.

If any seller chooses not to use the IOSS, the customer will have to pay the delivery or customs agent to access their goods. This can profoundly impact the customer experience and repeat business.

Closing the import VAT exemption loophole

After July 1, 2021, the €22 VAT exemption on low value parcels imported into the EU for delivery to customers will be withdrawn.

This exemption has been exploited by many sellers mistakenly or deliberately under- declaring the import values of goods to avoid VAT. Under the new rules, VAT can now be charged at the point of sale for transactions up to the value of €150.

The VAT charged may then be declared and paid via a new submission, the Import One Stop Shop (IOSS). This process is designed to create an efficient green channel customs clearance

Implications

After July 1, 2021, EU sellers will no longer have a disadvantage on price, as all sellers will have to charge VAT on all imported goods.

EU sellers can opt to register for IOSS in just one EU state to declare the VAT on any affected imports on shipments €150 or less.

However, non-EU sellers will be required to register for IOSS or use an intermediary registered for IOSS in one EU member state. There are instances where a facilitating marketplace (see EU and non-EU marketplaces become the deemed supplier), or delivery service may step in to report and pay the VAT.

If any seller chooses not to use the IOSS, the customer will have to pay the delivery or customs agent to access their goods. This can profoundly impact the customer experience and repeat business.

Marketplaces become the deemed seller and VAT collector

The 2021 reforms will oblige marketplaces that facilitate cross-border sales to customers via third parties to become the deemed sellers in certain cases.

The EU has defined facilitating as “electronic platforms assisting sellers and customers to come together and strike a contract for the supply of goods on a cross-border basis.”

The new deemed supplier regime will apply in two use cases when the marketplace is facilitating a B2C sale: imports with a cross-border transaction not exceeding €150 by EU and non-EU sellers; and sales within the EU by non- EU sellers for transactions of any value.

The marketplace may be able to opt out of IOSS by way of a special arrangement process in which VAT obligations are transferred to the delivery company of the seller.

Implications

As a deemed seller, marketplaces (including non-EU marketplaces) will be responsible for charging and collecting VAT on deemed seller transactions after July 1, 2021.

For imports of €150 or less, rather than import VAT, the marketplace will charge the customer output VAT at the point of sale and declare it instead of the seller. As a result, both EU and non-EU sellers benefit from reduced VAT obligations and may be able to close their registrations in some EU states, while marketplaces could have new obligations to contend with. The marketplace will not take on product liability or regulatory obligations.

Marketplaces become the deemed seller and VAT collector

The 2021 reforms will oblige marketplaces that facilitate cross-border sales to customers via third parties to become the deemed sellers in certain cases.

The EU has defined facilitating as “electronic platforms assisting sellers and customers to come together and strike a contract for the supply of goods on a cross-border basis.”

The new deemed supplier regime will apply in two use cases when the marketplace is facilitating a B2C sale: imports with a cross-border transaction not exceeding €150 by EU and non-EU sellers; and sales within the EU by non- EU sellers for transactions of any value.

The marketplace may be able to opt out of IOSS by way of a special arrangement process in which VAT obligations are transferred to the delivery company of the seller.

Implications

As a deemed seller, marketplaces (including non-EU marketplaces) will be responsible for charging and collecting VAT on deemed seller transactions after July 1, 2021.

For imports of €150 or less, rather than import VAT, the marketplace will charge the customer output VAT at the point of sale and declare it instead of the seller. As a result, both EU and non-EU sellers benefit from reduced VAT obligations and may be able to close their registrations in some EU states, while marketplaces could have new obligations to contend with. The marketplace will not take on product liability or regulatory obligations.

STEP 02

A single EU VAT return for ecommerce

At the heart of the 2021 ecommerce EU VAT reboot is the introduction of the One Stop Shop (OSS) single EU VAT return.

After July 1, 2021, B2C sellers dispatching their goods from a single country will no longer be required to register for foreign VAT and complete multiple VAT filings in countries where they are selling. Instead, they may opt out and simply complete a single OSS filing listing all their Pan-EU sales along with their regular domestic VAT return. If sellers have physical locations in several member states, they may choose any of those states in which to remit VAT. If a seller has no physical locations, other rules apply.

This reform builds on the successful launch of the single VAT return for B2C digital services in 2015 referred to as the Mini One Stop Shop (MOSS) return.

Ending the distance selling threshold rules

The current EU VAT regime place of supply rules (known as “the destination principle”) require sellers to charge the VAT of their customer’s country of residence. For EU cross- border sales, this means sellers must VAT register in each country where they sell goods.

Currently, to reduce the burden on small sellers, the EU operates a special VAT registration simplification for ecommerce known as distance selling thresholds. This simplification is generally available only for sales from a seller’s inventory.

After July 1, 2021, this registration threshold simplification will be withdrawn. Sellers who are not established in the EU will have to charge the VAT rate of the customer’s country of residence from their first sale and remit it to the foreign tax authorities.

EU distance selling

thresholds before July 2021

€100,000 per annum: Germany, the Netherlands, Luxembourg.

€35,000 per annum or local

currency equivalent: all other

members of the EU.

Beginning January 1, 2021, the U.K. threshold was reduced to zero for

EU and non-EU sellers.

More information on these distance selling thresholds can

be found at avalara.com.

Ending the distance selling threshold rules

The current EU VAT regime place of supply rules (known as “the destination principle”) require sellers to charge the VAT of their customer’s country of residence. For EU cross- border sales, this means sellers must VAT register in each country where they sell goods.

Currently, to reduce the burden on small sellers, the EU operates a special VAT registration simplification for ecommerce known as distance selling thresholds. This simplification is generally available only for sales from a seller’s inventory.

After July 1, 2021, this registration threshold simplification will be withdrawn. Sellers who are not established in the EU will have to charge the VAT rate of the customer’s country of residence from their first sale and remit it to the foreign tax authorities.

EU distance selling

thresholds before July 2021

€100,000 per annum: Germany, the Netherlands, Luxembourg.

€35,000 per annum or local

currency equivalent: all other

members of the EU.

Beginning January 1, 2021, the U.K. threshold was reduced to zero for

EU and non-EU sellers.

More information on these distance selling thresholds can

be found at avalara.com.

Launching the single OSS EU VAT return

In addition to withdrawing the distance selling thresholds, the EU is extending the single VAT return, OSS, to ecommerce cross-border distance selling of goods and services (see below). This will replace the obligation to VAT register in every country where sellers are making sales to EU customers from inventory in a single EU location — typically their home state.

The existing obligation to register in all countries is often called out as the principal barrier to cross-border trade in the EU. A single VAT return listing all Pan-EU sales known as the Mini One Stop Shop (MOSS) has been in place since 2015 for B2C cross-border sales of digital, telecommunications, and broadcast services.

Sellers with existing foreign VAT registrations who sell from inventory and are registered where their customers are based may opt to close these registrations after July 1, 2021, and use the OSS return instead.

NOTE: Sellers holding inventory in other EU countries may benefit from OSS if they sell through electronic platforms. However, they must remain VAT registered in each country where they are holding inventory to record any intra-community goods movements. This includes selling using the Fulfillment by Amazon (FBA) program.

The existing obligation to register in all countries is often called out as the principal barrier to cross-border trade in the EU. A single VAT return listing all Pan-EU sales known as the Mini One Stop Shop (MOSS) has been in place since 2015 for B2C cross-border sales of digital, telecommunications, and broadcast services.

Sellers with existing foreign VAT registrations who sell from inventory and are registered where their customers are based may opt to close these registrations after July 1, 2021, and use the OSS return instead.

NOTE: Sellers holding inventory in other EU countries may benefit from OSS if they sell through electronic platforms. However, they must remain VAT registered in each country where they are holding inventory to record any intra-community goods movements. This includes selling using the Fulfillment by Amazon (FBA) program.

OSS may be used to report cross-border B2C traditional services and, for EU-based sellers, certain domestic sales facilitated by marketplaces.

Sellers will charge VAT at the rate of their customer’s country of residence. They can use the delivery address of their customer to identify the country of residence and determine the standard VAT rate (or apply a reduced or nil (0) VAT rate) according to the varying rates and goods classifications of each customer’s member state.

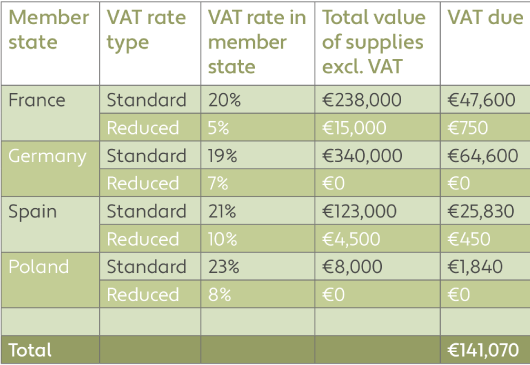

The OSS filing will be a quarterly return. It is intended as a simple listing to declare VAT due by the seller to each EU country. The OSS return will be standardized across all the EU member states and will be similar to the following template:

Example OSS return from 2021

Non-EU sellers

Sellers who are not residents of the EU, including North American sellers, may also use the OSS simplified filing.

They can file regular OSS returns like any EU ecommerce seller. There is no need to file a regular domestic VAT return unless the non-EU seller holds inventory in the relevant country.

Non-EU sellers

Sellers who are not residents of the EU, including North American sellers, may also use the OSS simplified filing.

They can file regular OSS returns like any EU ecommerce seller. There is no need to file a regular domestic VAT return unless the non-EU seller holds inventory in the relevant country.

The amounts should be shown in the local currency where the seller is registered for OSS. In the case of a foreign currency conversion, such as the U.S. or Canadian dollar, sellers should follow the guidance of that country on rates to use at the date of the transaction.

Filing OSS

The OSS filing should be submitted by the end of the month following the tax period covered by the return (calendar quarter). The VAT due should be remitted by the same deadline.

The tax authority will then be responsible for dividing up the VAT received from the seller to each country as appropriate.

Exemption for EU microbusinesses does not apply to non-EU businesses

The EU will grant EU-based microbusinesses selling less than €10,000 per annum cross-border on B2C goods and services an exemption from the OSS rules. Non-EU microbusinesses are not exempt from the OSS rules. This reflects the experience of the 2015 MOSS return that imposed overly complex customer tracking and VAT calculations on the smallest of sellers.

B2C services via OSS

In addition to reporting B2C goods on the new OSS VAT return, EU and non-EU businesses may report certain services, such as:

- Electronic, telecom, and broadcast services currently reported via the single MOSS return. These include streaming or downloadable media, apps, ebooks, subscriptions to journals or membership sites, and web services.

- As performed services, or traditional services sold online. These include training and education, ticket sales for events, transportation, valuation, work on immovable property, and other services connected to immovable property.

Non-EU sellers must use a separate non-EU OSS registration and filing procedure for the as performed services listed above.

B2C services via OSS

In addition to reporting B2C goods on the new OSS VAT return, EU and non-EU businesses may report certain services, such as:

- Electronic, telecom, and broadcast services currently reported via the single MOSS return. These include streaming or downloadable media, apps, ebooks, subscriptions to journals or membership sites, and web services.

- As performed services, or traditional services sold online. These include training and education, ticket sales for events, transportation, valuation, work on immovable property, and other services connected to immovable property.

Non-EU sellers must use a separate non-EU OSS registration and filing procedure for the as performed services listed above.

Closing the delivery VAT avoidance loophole

EU member states have also agreed to close a delivery loophole being exploited by some ecommerce sellers in their efforts to avoid charging and reporting foreign VAT.

A limited number of sellers are not delivering directly to foreign customers. Instead, they’re organizing third-party fulfillment firms and requiring customers to sign separate delivery contracts. This, potentially, allows sellers to charge only their national VAT rate instead of the customer’s country of residence rate.

To ensure the tax authorities of the customers receive their fair share of VAT, the EU is closing this avoidance loophole in 2021.

Where the seller indirectly intervenes to provide transportation on a cross-border sale, they will now have to charge the VAT of their foreign EU customers and report VAT through their OSS filing or nonresident VAT return.

Recovering foreign VAT

OSS does not allow sellers to recover local VAT incurred on hotel or taxi travel, for example.

EU sellers will have to complete an 8th Directive VAT recovery claim to recover these expenses. Similarly, non-EU sellers will still be required to complete a 13th Directive claim. The 8th Directive does not apply to the U.K. after Brexit.

OSS is voluntary

Lastly, it will not be obligatory to use the OSS return. Sellers may still keep their foreign VAT registrations open and report local sales and VAT through them.

STEP 03

Closing the low value consignment stock loophole

Before July 1, 2021, EU and non-EU sellers selling goods online to EU customers can ship goods into the EU directly to the customer, import VAT-free, if the goods are valued at €22 or below.

This exemption, called the low value consignment stock relief, was intended to relieve customs from the burden of checking large volumes of packages for small amounts of potential tax revenues.

However, it is leaving EU-based sellers at a price disadvantage since they must charge VAT when the goods are dispatched from within the EU. The exemption has also encouraged abuse by sellers deliberately under-declaring the values of goods to escape the import VAT bill.

Switching import VAT to point of sale for efficient green channel clearance

The EU has agreed to remove the import VAT-exempt threshold. Instead, it will require EU and non-EU sellers to charge VAT at the point of sale for consignments of €150 or below. This is designed to create a more efficient green channel with quick and easy customs clearance. Note: Alternatively, the delivery agent may act as the import VAT collector through the special arrangement process.

Sellers will charge the VAT rate of their customer’s EU country of residence at the point of sale on the website. Sellers can use the customer’s delivery address to determine the country VAT rate. No VAT is due at the point of import in this case.

IOSS import VAT simplified reporting

To report VAT charged at the point of sale, Import One Stop Shop (IOSS) is being introduced. IOSS will report distance selling across EU borders of imported consignments not exceeding €150. Sellers, or deemed supplier marketplaces, may register for IOSS in just one EU member state. They will be issued a unique IOSS identification number that should be listed on all custom declarations sent to the EU. This will indicate to customs that VAT is being properly declared and help ensure speedy customs clearance.

Like the OSS, IOSS will be a regular filing submitted to a tax authority in one nominated EU member state. IOSS will declare output VAT due in all EU countries. The format will be similar to the VAT OSS. Sellers will have to make a single cash payment of VAT due to the country where they are IOSS-registered. IOSS requires a monthly return and OSS requires a quarterly return.

Non-EU sellers and the IOSS

U.S.-based sellers selling goods located outside of the EU to EU customers may also use the IOSS. It could be useful where the seller’s customers are located in EU member states and the seller wants to take care of the import VAT on behalf of their customer. It also relieves the seller of having to undertake a full VAT registration in each country it is importing into.

U.S.-based sellers will have to appoint an intermediary, a type of fiscal representative, in their chosen member state of identification.

What will this mean for a typical non-EU seller?

To understand the effects for a typical non-EU seller, let’s compare VAT obligations before July 1, 2021 with VAT obligations after the 2021 reforms. A fictitious non-EU seller, SamEagleTrading LLC from the United States, will serve as our example:

Before July 2021

SamEagleTrading LLC can sell and ship goods under €22 to EU customers VAT-free. Over that limit, either the customer or SamEagleTrading LLC must pay import VAT at the rate of the country of import. To provide a good seller experience, SamEagleTrading LLC pays the import VAT on behalf of its customers

July 2021

SamEagleTrading LLC will charge VAT at the point of sale and declare it in an IOSS return if it is below €150. The customer is then exempted from paying import VAT at customs.

SamEagleTrading LLC may also declare sales to customers around the EU via its OSS return, as discussed in the above section.

For goods above the new €150 IOSS threshold, the import VAT must still be paid to customs. This could still trigger a regular VAT registration in the country of importation for SamEagleTrading LLC if they wish to sell the goods locally or to customers in other EU countries.

Before July 2021

SamEagleTrading LLC can sell and ship goods under €22 to EU customers VAT-free. Over that limit, either the customer or SamEagleTrading LLC must pay import VAT at the rate of the country of import. To provide a good seller experience, SamEagleTrading LLC pays the import VAT on behalf of its customers

July 2021

SamEagleTrading LLC will charge VAT at the point of sale and declare it in an IOSS return if it is below €150. The customer is then exempted from paying import VAT at customs.

SamEagleTrading LLC may also declare sales to customers around the EU via its OSS return, as discussed in the above section.

For goods above the new €150 IOSS threshold, the import VAT must still be paid to customs. This could still trigger a regular VAT registration in the country of importation for SamEagleTrading LLC if they wish to sell the goods locally or to customers in other EU countries.

Special arrangements: The postal services’ role

IOSS is not compulsory for sales less than €150. Alternatively, sellers may elect to have import VAT collected from the final customer by the customs declarant. This is generally the postal operator, courier firm, or customs agent.

The final customer can settle the VAT collected with tax authorities via a monthly payment known as a special arrangement.

In certain circumstances, marketplaces facilitating a sale will be responsible for the import VAT being charged at the point of sale for the EU or non-EU seller. This scenario is detailed in the next section.

Brexit — the effect on IOSS

The U.K. withdrew its EU £15 low value consignment stock relief threshold when it left the EU VAT rules on December 31, 2020, the end of the Brexit transition period. The U.K. has introduced a new £135 VAT parcel system similar to the EU’s €150 IOSS scheme.

Non-U.K. sellers are required to obtain a regular U.K. VAT registration to report the output VAT charged at the point of sale to U.K. customers on import sales not exceeding £135.

Simplified customs declaration

To help importers and customs authorities cope with the ballooning volume of low value consignments, the standard customs declaration for goods not exceeding €150 is to be condensed. After July 1, 2021, sellers will be able to provide a simplified declaration at the point of import into the EU. This is a significantly reduced dataset for the party declaring the import.

The existing duties exemption for most sales not exceeding €150 will remain in place.

STEP 04

EU and non-EU marketplaces become the deemed supplier

Ecommerce VAT evasion is estimated to cost EU member states €5 billion per annum, a figure expected to grow to €7 billion by 2021.

Because online marketplace platforms now play such a significant role in facilitating the growth of online selling, EU member states have agreed to employ them in the fight against ecommerce VAT fraud.

After July 1, 2021, online marketplaces (OMPs) may become the deemed supplier when they facilitate certain cross-border B2C transactions of their third-party sellers. OMPs will therefore be liable to collect, report, and remit the VAT due from the customer.

While the marketplace takes on the VAT rights and obligations of the sale, they will not take on other obligations, such as product liabilities. This new rule is part of the ecommerce package of reforms intended to help simplify VAT compliance and tackle online VAT fraud.

To understand where the new rules will apply, examine the following: the definition of a marketplace, what is facilitation, and which transactions are included in either. Once identified as a deemed supply, a new, two-stage VAT transaction process must be applied to the transaction.

While the marketplace takes on the VAT rights and obligations of the sale, they will not take on other obligations, such as product liabilities. This new rule is part of the ecommerce package of reforms intended to help simplify VAT compliance and tackle online VAT fraud.

To understand where the new rules will apply, examine the following: the definition of a marketplace, what is facilitation, and which transactions are included in either. Once identified as a deemed supply, a new, two-stage VAT transaction process must be applied to the transaction.

Defining a marketplace

The EU Council implementing regulation for the July 2021 ecommerce package refers to electronic interfaces, which include online marketplaces, platforms, portals, or similar means. The role of the marketplace is to introduce customers to sellers who then enter into a contract that results in a taxable sale.

Is the marketplace facilitating the sale?

A marketplace facilitates a sale when it participates in any of the following:

- Controlling the terms and conditions of the sale

- Authorizing the charge to the customer with respect to the payment for the supply

- Ordering or delivering goods

The marketplace does not facilitate a sale if it exclusively provides any of the following services in relation to the sale:

- Payment processing

- Listing or advertising goods

- Redirecting customers to other marketplaces where the goods are offered without any further

Which transactions are included?

Two types of cross-border transactions are included for the July 2021 deemed supplier rule changes when facilitated by a marketplace:

- Import sales by EU or non-EU sellers to customers of sales not exceeding €150.

- Goods sales already in the EU sold by non-EU sellers to an EU customer of any value. This may be on a distance sale (cross-border) or domestic sale basis.

Two-stage VAT transaction for deemed supplier marketplace sales

Once a seller and customer have agreed to a sale, the existing single-transaction procedure between the seller and customer will be split in two:

- The seller will sell goods to the marketplace on a B2B VAT exempt-with-credit basis. This means the seller remains free to deduct any input VAT suffered on the purchase of the goods. The transport of the goods will be attached to this transaction, entitling the transport to a zero rating.

- The marketplace will sell the goods to the customer, charging the VAT rate of the customer’s country of residence. The VAT is due when the marketplace receives the order, the commitment, or the order to pay from the customer.

To understand the marketplace facilitation use case, let’s look at an example:

Example: Non-EU selling goods across EU borders for any value

U.S. Seller Inc. is a U.S.-based seller. It buys goods in France for resale to French and Austrian customers via a facilitating marketplace.

Before July 1, 2021:

U.S. Seller Inc. is French VAT registered to charge 20% French VAT on domestic sales and to recover the French import and input VAT it’s charged when importing and buying local inventory. It is also Austrian VAT registered (assume it’s over the Austrian distance selling threshold of €35,000) to charge 20% Austrian VAT to customers on goods sent from France.

After July 1, 2021:

The facilitating marketplace will become the deemed supplier for the French and Austrian sales to local customers. The marketplace will make use of OSS and IOSS portals from France or Germany where it is already registered for VAT. Or, if the marketplace does not have an EU VAT registration, it can instead receive a VAT number for IOSS and OSS purposes in France or Austria.

U.S. Seller may deregister from France and Austria — unless it is selling on its own website or holding inventory locally. It must keep open its French VAT registration and deduct input VAT on purchases from France. Lastly, U.S. Seller can recover the Austrian VAT it paid when initially buying its inventory via a 13th Directive VAT recovery claim.

Calculating the €150 intrinsic consignment value

A major challenge for the new import program will be calculating the €150 consignment threshold for the IOSS reporting. This relates to the customs declared value of a single package or consignment being cleared through customs to a single customer. If the consignment is made up of multiple goods, the value of these goods must be added together to determine whether the consignment qualifies for the IOSS program.

For marketplaces, often a customer will buy goods from multiple sellers and then check out. The organizer of the shipment or marketplace may package these goods in a single consignment. If the combined value of the goods exceeds €150, then the VAT treatment, collections, and reporting cannot fall under IOSS. Marketplaces may therefore have to adjust the VAT determination after the checkout, which could present some issues.

The customer may seek a VAT refund from the facilitating marketplace or seller, whichever party was responsible for charging output VAT. This also helps to avoid double taxation in the case of goods with output VAT triggering customs import VAT when clearing into the EU.

Marketplace record-keeping obligations

In addition to taking on potential deemed supplier VAT responsibilities, marketplaces will also have new record-keeping responsibilities. They’ll be required to keep seller transactions in sufficient detail that tax authorities in the customer’s country can check whether VAT has been correctly accounted for. Transactional data must be held electronically for at least 10 years after the year of the transaction.

Even where the marketplace has not facilitated the sale, it is still obliged to maintain basic transactional data for each seller, including their VAT numbers.

Marketplace liable for mistakenly declared VAT?

A marketplace will not be held liable for underpaid VAT on deemed supplier transactions when the seller provided the marketplace with erroneous information for the VAT calculation. However, the marketplace will have to demonstrate that it did not and could not reasonably have known the information it received from the seller was incorrect.

Brexit implications?

The U.K. is no longer part of the EU, having left the EU VAT regime on December 31, 2020. The July 2021 deemed supplier marketplace reforms will not apply to transactions in the U.K.

The U.K. introduced its own version of the deemed supplier marketplace rules on January 1, 2021. They are similar to the EU rules — imports not exceeding £135 or any sale by a non-U.K. business on a marketplace are now the VAT responsibility of the marketplace.

CONCLUSION

It’s time to sell into Europe more confidently

As you can see, selling into Europe and managing VAT compliance is not for the faint of heart. But with Avalara, you can relax knowing we’ve simplified the hardest parts with end-to-end VAT compliance solutions. Avalara is here to help you understand where your business has VAT obligations, register your business to report VAT with the appropriate tax authorities, understand the taxability of the products you sell, calculate the correct VAT and customs duties, and properly report VAT.

Your VAT obligations can continue to evolve as your business changes

Visit this guide as often as you need to. And while we hope you find this information valuable, it’s not a substitute for advice from a tax professional.

Are you selling into other countries in the world?

Avalara supports VAT determination throughout the globe, GST calculation and compliance in India, and VAT compliance in Brazil. Visit the Avalara international tax solutions webpage for more information.

STEP

01

Introduction

STEP

02

A single EU VAT return for ecommerce

STEP

03

Closing the low value consignment stock loophole

STEP

04

EU and non-EU marketplaces become the deemed supplier

STEP

05

Conclusion

STEP

01

Introduction

STEP

02

A single EU VAT return for ecommerce

STEP

03

Closing the low value consignment stock loophole

STEP

04

EU and non-EU marketplaces become the deemed supplier

STEP

05

Conclusion

01

Introduction

02

A single EU VAT return for ecommerce

03

Closing the low value consignment stock loophole

04

EU and non-EU marketplaces become the deemed supplier

05

Conclusion