Ethanol Taxation Challenges

The Blend for Compliance Success

In 2005 Congress approved the Energy Policy Act, which removed the oxygenate requirement for gasoline and approved the Renewable Fuels Standard (RFS). This piece of legislation mandated that fuel producers blend renewable fuels, like ethanol, into traditional fuels.

The change was spurred by the controversy over the use of MTBE (methyl-tertiary-butyl ether), which makes gasoline burn more efficiently by blending it with oxygen. When it was discovered that MTBE was leaking into groundwater and causing pollution, the federal government officially banned MTBE through the RFS. In order to meet the renewable fuel blending requirements set by the RFS, motor fuel suppliers began blending gasoline with ethanol, and the market began to grow.

Post-2005, the number of ethanol producers and the amount of ethanol produced increased dramatically to meet these supplier’s needs. The nation saw a 3,700% increase in ethanol production between 1982 and 2012 (from 350 million gallons to 13.3 billion gallons). Today there are more than 200 ethanol bio-refineries in 29 states. These facilities have the ability to produce more than 15 billion gallons of ethanol.1 As of January 2015, ethanol is blended into 97% of the U.S.gasoline supply, in 2002 this number was 15%.2 The stats speak for themselves — ethanol is here to stay.

Ethanol Exports

A 2014 report from the Renewable Fuels Association cited a 35% increase in U.S. ethanol exports between 2013 and 2014. The 836 million gallons exported was the second most in U.S. history. This number represents 5.9% of total ethanol produced in the U.S. This fuel was exported to 51 countries around the world.4

Too Good to be True? Partially.

While ethanol provides an environmentally friendly way to reduce the amount of gasoline used in the United States, it is largely made from corn (98% of 2014 production used corn3). The use of corn introduces a long-term production capacity issue. Corn crop production relies on a variable outside of human control – weather. Droughts, floods or other weather phenomena such as tornados can affect the supply chain with sometimes little notice. In addition, there is a ceiling on how much corn can realistically be grown to satisfy the increasing demand for ethanol.

Another roadblock to the wider adoption of ethanol for use as a motor fuel is engine compatibility. Many automobile engines are not able to process high levels of ethanol. The maximum blend percentage that is acceptable for all vehicles is E10 (10% ethanol blended with 90% gasoline). E10 is found at most fuel retail pumps in the U.S. 80% of cars manufactured after 2001 are able to run on blends of up to 15%. However it may be many years before E15 is widely available at retailers due to required infrastructure changes and associated liabilities.

Flex-fuel vehicles (FFV) are able to run on E85, the highest-octane ethanol blend. FFVs make up 7% of the vehicles on the road today (16 million), but this number is expected to rise in coming years, as both consumer demand for alternative fuels vehicles and the RFS blend requirements increase.

So, What Does This Mean for Taxes?

Excise taxes on motor fuels are notoriously complex which makes compliance difficult. Adding biofuels like ethanol, and all of its various blends, into the equation creates some unique challenges and makes every day fuel tax complexities even more of a headache.

Federal Tax Credits

To encourage the production of renewable fuels like ethanol, the federal government offers a variety of tax credits. It is critical that ethanol producers are aware of these credits, and their reporting requirements in order to take advantage of the reduction of taxes owed on the fuel they produce.

Find a partial list of credits as of February 2015 below:

Second Generation Biofuel Producer Tax Credit

Allows for a credit up to $1.01/gallon of second generation biofuel that is sold and used by the purchaser to produce a second generation biofuel mixture, as a fuel in trade or business, sold as a motor fuel at a retailer, or used by the producer to do any of the above.

Alternative Fuel Mixture Excise Tax Credit

Alternative fuel blenders registered with the IRS may be eligible for $0.50/gallon credit on the sale or use of their alternative fuel blend for use in that blender’s business operations.

Alternative Fuel Infrastructure Tax Credit

Fueling equipment for E85, as well as other alternative fuels, installed between January 1, 2006 and December 31, 2013 is eligible for a 30% tax credit of the cost, not to exceed $30,000.

For more information on all federal tax credits visit http://www.ethanolrfa.org/pages/tax-policy

The federal government also has an Ethanol Blend Retailer Tax Credit in place through 2020. A credit of $0.08/gallon is granted when pure ethanol is blended into gasoline, but to qualify for this credit, the retailer must sell a certain percentage of renewable fuel, either company-wide or on a site-by-site basis. For 2015, that number is 17% for retailers selling more than 200,000 gallons of motor fuel and 14% for those selling less. A stipulation to this credit is that those retailers who are within 2% of this target receive a $0.06/gallon credit.

The credit is managed at the state-level, so state governments have the power to adjust this credit based on market conditions (such as a shortage of biofuel feedstock). State-to-state

variations of this credit can be difficult to track, but if retailers fail to claim it they can find themselves at a competitive disadvantage.

For more information visit: http://www.afdc.energy.gov/laws/5237

Staying apprised not only of the changing federal tax credits, breaks and loans, but also compiling the required documentation that must be filed in order to receive these incentives takes a lot of time and coordination.

Taxing Ethanol at the State Level

Each state has it’s own laws outlining the tax structure for motor fuels, including ethanol. States also offer their own tax credits to promote the production and use of alternative fuels like

ethanol. For companies operating in multiple states, this leads to a wide variety of tax policies that tax managers are required to stay apprised to remain compliant.

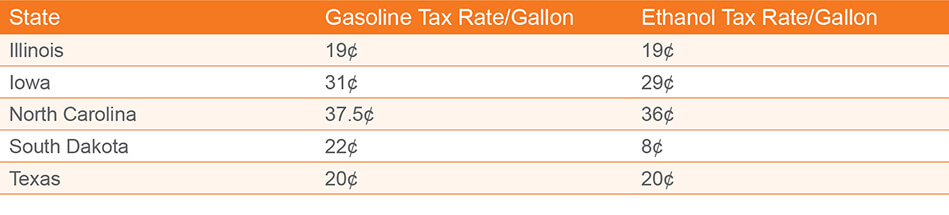

State Rates

Some states, like North Carolina, Illinois and Texas tax ethanol at the same rate as petroleum gasoline. To those states, Tax Managers across the United States say, “thank you.” Most states however, have different tax rates for ethanol. This can get tricky for ethanol blends, as discussed earlier. This means that the 10% of ethanol in E10 is taxed at a different rate than the 90% of petroleum in that same gallon.

For example, in South Dakota, ethanol is taxed at 8¢/gallon, while gasoline is taxed at 22¢/gallon. That means that for a gallon of E10 in South Dakota, the tax equals 0.1(0.08) + 0.9(0.22) = .008 + 0.198 = $0.206/gallon. This 0.014¢ reduction in tax per gallon can have a large effect on profitablility when taxes are collected or paid on millions of gallons.

The chart below shows tax rates for gasoline and ethanol in a variety of states (please note that rates change regularly):

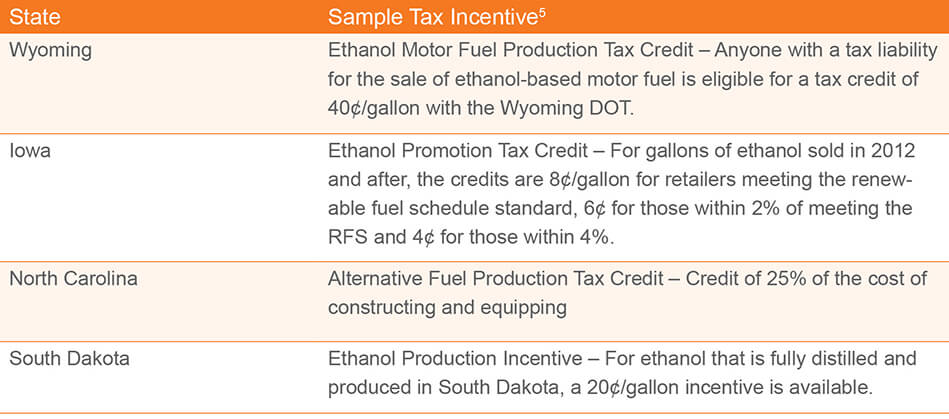

State Incentives

Similar to the tax credits from the federal government, individual states often offer tax credits and breaks for the production and use of ethanol. While each state is different, here are a few

examples of programs offered by states, as of July 2014:

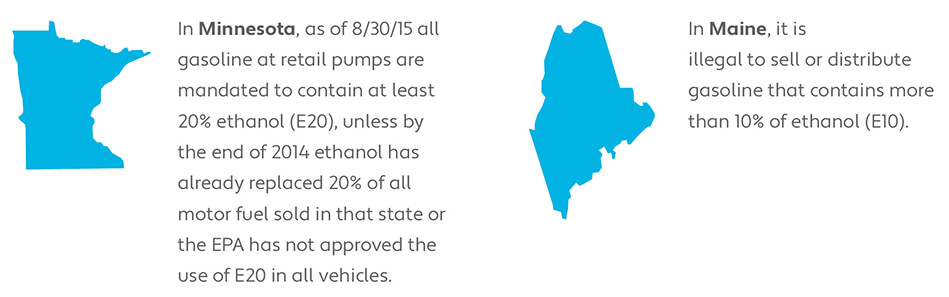

Ethanol Mandates

A state’s position on providing incentives for the use of biofuels like ethanol can vary drastically from state to state. Political motivations often influence the passage of regulations on biofuels. Thirteen states have some form of fuel mandate, or laws requiring that all gasoline be mixed with a biofuel.

An example of how state regulations differ can be seen in the treatment of ethanol-blended fuels in Minnesota and Maine.

This is a clear demonstration of how drastically different each state approaches the introduction of ethanol into the fuel market.

RENEWABLE IDENTIFICATION NUMBER (RIN)

Prior to blending, every gallon of ethanol is assigned a Renewable Identification Number (RIN) by the producer or importer. This 38-digit code allows the EPA to track whether ethanol producers are fulfilling the blending requirements outlined in the Renewable Fuel Standard (RFS). As the fuel moves along the supply chain, the RIN certificate accompanies it. Companies must keep track of these certificates for reporting and to prove they are meeting the RFS requirements to collect applicable tax credits.

Supply Chain Challenges

Ethanol is highly corrosive and cannot be transported via

pipeline, therefore transport methods such as fleets, trains and barges are introduced into the supply chain. This variance from the traditional fuel supply chain introduces additional tax challenges as fuel companies scramble to figure out at which point in the chain they are required to pay or collect excise taxes, and where they can report the transaction without a tax exchange. To add further complexity, whether or not the suppliers and buyers are licensed in the state where the transaction is taking place, or in the fuel’s final destination state, impacts the necessity to pay (or not pay) excise taxes.

As ethanol moves along the supply chain, through various jurisdictions and states, both tax rates and taxation points change. For example, in Wisconsin, ethanol production plants have to license with the state as a Terminal Operator, and they file the same Wisconsin Terminal Operator Report that a traditional petroleum terminal operator has to file. This includes filing with a Terminal Control Number that is in the same format as the IRS Terminal Control Number. When that Wisconsin ethanol producer sells to a customer who is exporting the product out of the state of Wisconsin, some, but not all, destination states require that the original ethanol plant be licensed within their state if they produce 100% ethanol. This requirement is mandated even though the ethanol plant sold the product FOB-Origin and the ethanol plant has no operations in the destination state.

If that same load of ethanol is shipped via rail to South Dakota where the original buyer then blends it, that blender/buyer has to report the transaction in both South Dakota and Wisconsin. Adding to the confusion, the seller of this new blend has to charge the end customer different tax rates for the blended gasoline product based on the percentage of ethanol within the final product. These transactions are all captured on the party’s tax returns for reporting purposes, but they do not always require taxes to be paid.

But, what if a customer buys ethanol from the original buyer (who first purchased it from the Wisconsin ethanol plant) and blends it with gasoline himself? What tax rate is charged by the state? Where are they in the supply chain? South Dakota requires the gasoline supplier to charge the adjusted rate for a 10% Ethanol blend even though the gasoline supplier is selling pure gasoline to the blender of record. Why? So the state can match the records more accurately on the state filing side.

Phew! Time to call in tax back-up.

How to Overcome the Challenge

The fluid nature of the excise tax laws and regulations on ethanol requires companies who buy and sell the fuel to constantly be on their toes. What tax managers at these companies may not realize is that this time-consuming work can be outsourced to a company whose sole focus is to ensure tax compliance.

So, when Alabama decides to change their ethanol tax credit from $0.08/gallon to $0.09/gallon, software is automatically updated and companies do not miss out on that extra penny per gallon credit. Or, when Texas decides to change the tax law so gasoline and ethanol are taxed at different rates, companies do not have to update labor-intensive spreadsheets.

Avalara is the leading provider of fuel excise tax calculation and compliance automation. Their team of fuel tax specialists is dedicated to staying on top of changing rates, rules and fees. When you subscribe to their cloud-based software solution, you get peace of mind that your taxes going to be calculated using the correct rate, at the correct point in the supply chain for the state in which the transaction is taking place.

When it comes to excise taxes, even a seemingly small error of a tenth of a percent can dramatically affect not only the profitability of a company, but also the ability to avoid an audit liability at the federal or state levels. Fortunately there is a solution for that.

1 Renewable Fuels Association, Pocket Guide to Ethanol 2015,

http://ethanolrfa.3cdn.net/23d732bf7dea55d299_3wm6b6wwl.pdf

2 Renewable Fuels Association, 40 Facts about Ethanol Source:

http://www.ethanolrfa.org/pages/40-facts-video-sources/ Viewed May 7, 2015.

3 Renewable Fuels Association, Pocket Guide to Ethanol 2015,

http://ethanolrfa.3cdn.net/23d732bf7dea55d299_3wm6b6wwl.pdf

4 Renewable Fuels Association, 2014 U.S. Ethanol Exports and Imports Statistical Summary,

http://www.ethanolrfa.org/page/-/rfa-association-site/studies/2014%20U.S.%20Export-Import%20Report.pdf?nocdn=1 Viewed May 6, 2015

5Federation of Tax Administrators, State Taxation of Motor Fuels – Summary of State Laws, July 2014;

© Avalara Rev 071415

Contact us at: 877-780-4848