The executive’s guide to sales tax risk

A Wakefield Research Report

Sales tax laws are changing rapidly

This report sheds light on the outlying trends that impact a company’s risk level and demonstrates why company leaders should take a closer look at how sales tax is managed within their organizations. With an eye on the ever-changing legislative landscape, sales tax compliance has become more important—and more complicated—in recent years. This report draws upon a new survey by Wakefield Research, who investigated what leading and emerging companies in the U.S. know (and don’t know) about sales tax as well as how accounting and finance professionals in the trenches are doing to safeguard their organizations from potential audits and maintain compliance.

About the survey

The survey, conducted in October 2014, is the second in an ongoing series, which includes online responses from over 400 U.S. finance and accounting professionals across several industries, ranging from ecommerce, to retail to manufacturing. The survey covered a wide range of topics including the Marketplace Fairness Act or "Internet Tax" nexus, sales and use tax audits, the cost of compliance and more. Companies surveyed have annual revenues of $1 million or more. Major findings from this report are also compared with recent Wakefield Research survey data gathered from companies who automate their sales and use tax compliance with dedicated sales tax software.

What sales tax compliance means for risk management

Risk management is usually top of mind for C-level executives. This is especially true in the areas of finance and accounting, as companies face increasingly stringent standards. Until recently, sales tax compliance, was not a major focus with company leadership. But what’s emerged in recent years is a very difficult landscape, where new sales tax rules at the Federal and State level that determine sales tax liabilities (otherwise known as "nexus"), are making compliance very difficult. Adding to that complexity are growing state deficits, which are fueling more demand for sales and use tax audits as a means for recovery.

Ignorance is not bliss concerning sales and use tax compliance

It’s not surprising that nearly half of the survey respondents feel that mastering the Rubik’s cube would be easier than mastering sales and use tax rules. A quick glance at the survey findings indicates that many companies simply aren’t prepared for changing regulations and lack the processes and expertise necessary to be compliant in this legislative climate. On one level it would appear that most companies feel they have sales tax compliance under control. According to the survey, 96% of accounting professionals are confident their company has the correct strategies in place, yet nearly half of the survey respondents believe that an auditor would find costly errors if they were audited for sales and use tax.

Conclusion: Business-as-usual processes are not good enough

The data suggests that many businesses don’t account for sales tax rules correctly—especially companies that sell online and have tax obligations in multiple states. There were close to 14,000 changes to rates and jurisdictions to occur this year in the U.S. alone, (up by nearly 40%) from the previous year, yet 40% of the accounting pros surveyed rely on “existing knowledge” to determine their tax liabilities. In fact, nearly half of the respondents couldn’t remember the last time they updated their sales tax compliance processes.

Supporting data

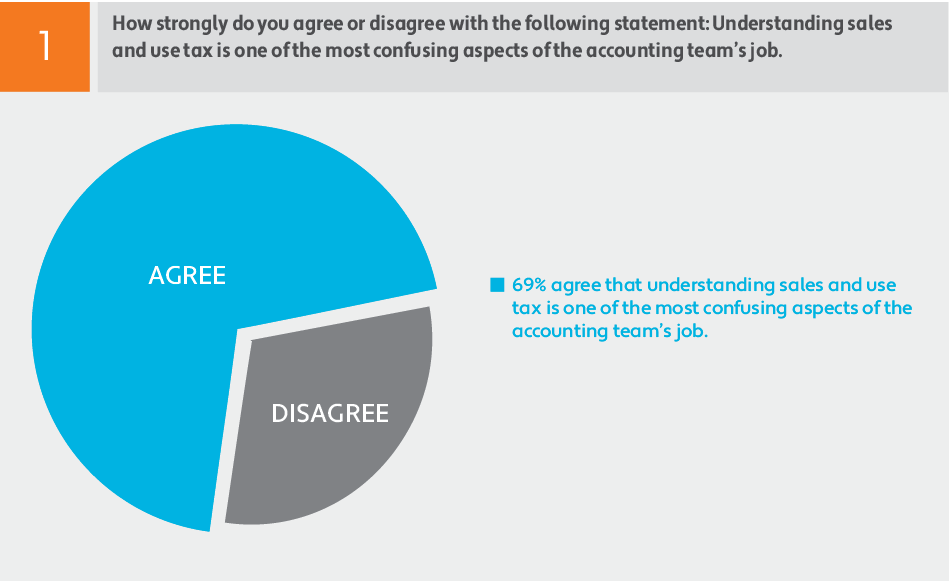

Question 1: How strongly do you agree or disagree with the following statement: Understanding sales and use tax is one of the most confusing aspects of the accounting team's job.

Summary: 69% agree that understanding sales and use tax is one of the most confusing aspects of the accounting team's job.

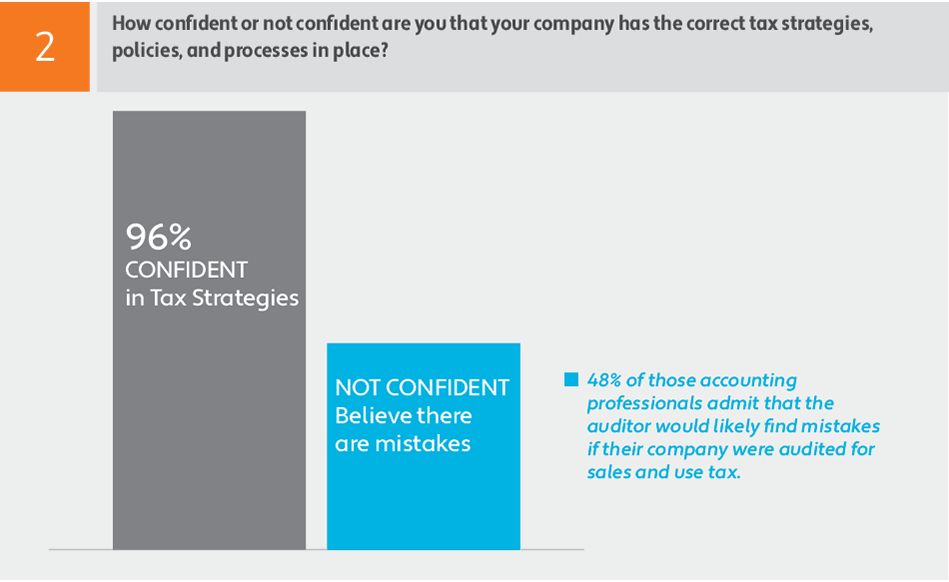

Question 2: How confident or not confident are you that your company has the correct tax strategies, poilicies, and processes in place?

Summary: 48% of those accounting professionals admit that the auditor would likely find mistakes if their company were audited for sales and use tax.

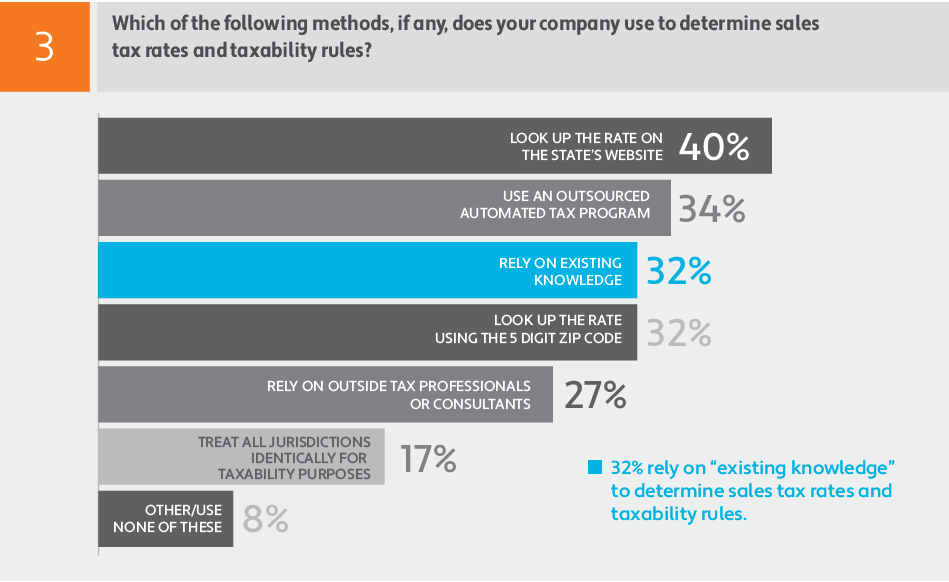

Question 3: Which of the following methods, if any, does your company use to determine sales tax rates and taxability rules?

Summary: 32% rely on "existing knowledge" to determine sales tax rates and taxability rules.

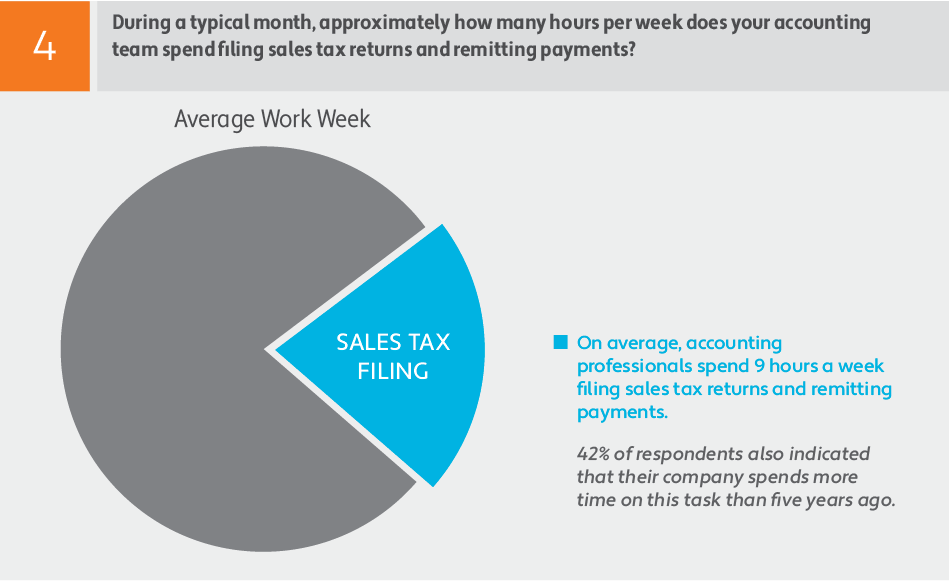

Question 4: During a typical month, approximately how many hours per week does your accounting team spend fi;ing sales tax returns and remitting payments?

Summary: On average, accounting professional spend 9 hours a week filing sales tax returns and remitting payments. 42% of respondents also indicated that their company spends more time on this task than five years ago.

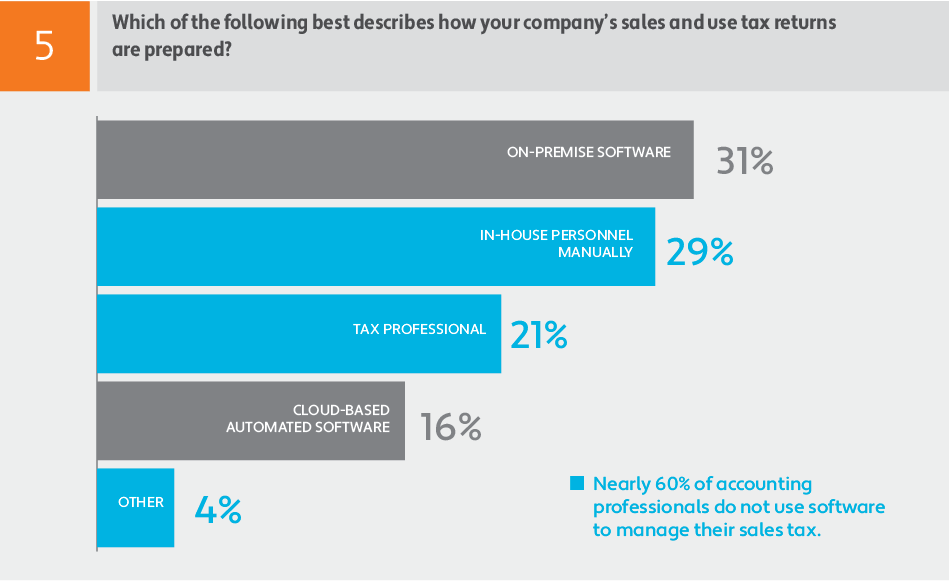

Question 5: Which of the following best describes how your company's sales and use tax returns are prepared?

Summary: Nearly 60% of accounting professionals do not use software to manage their sales tax.

Conclusion: The impact of a sales tax audit is underestimated by tax professionals

The survey found that there are many misconceptions around sales tax audits. One of the most striking is the belief among accounting professionals that if a company fails an audit, it’s only obligated to pay back the erroneous transactions found by the auditor. Truth is, penalties and fees can be applied to all transactions over an entire year as an overall percentage. That makes audits a high risk area for any business. According to the survey, the average audit costs a company more than $114,000 (up 19% from the previous year).

Moreover, more than half of survey respondents are unaware that tax liabilities uncovered during an audit can affect the valuation of a company.

Costs associated with negative audit findings can wipe out small-to-midsize companies’ profits. In spite of that, many don’t invest in automated sales tax compliance solutions. In fact, 60% of companies surveyed don’t use software solutions to manage sales tax.

Major audit mistakes found in the trenches:

- Missing documents, such as exemption certificates

- Applying the wrong sales tax rates to customer purchases

- Producing the wrong documents requested by an auditor

Supporting data

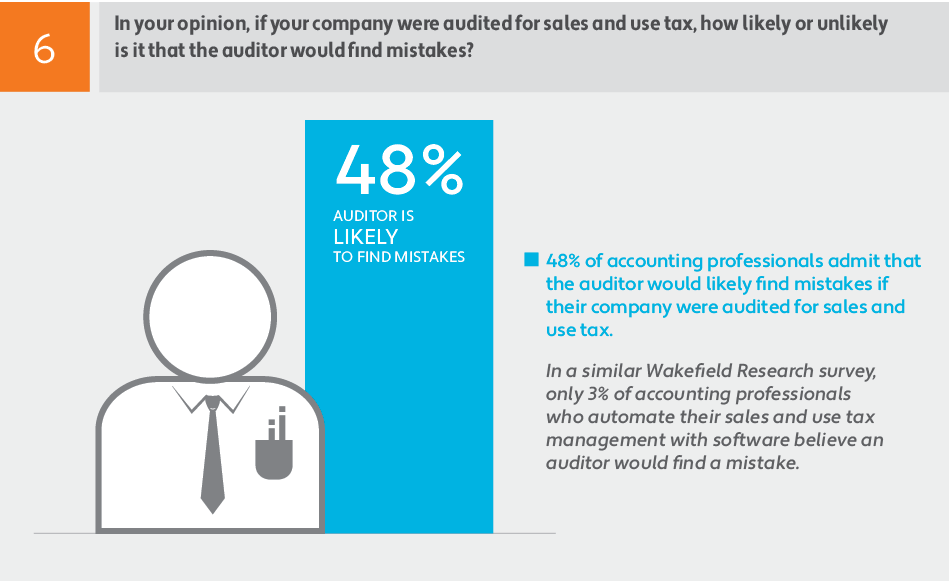

Question 6: In your opinion, if your company were audited for sales and use tax, how likely or unlikely is it that the auditor would find mistakes?

Summary: 48% of accounting professionals admit that the auditor would likely find mistakes if their company were audited for sales and use tax. In a similar Wakefield Research survey, only 3% of accounting professionals who automate their sales and use tax management with softward believe an auditor would find a mistake.

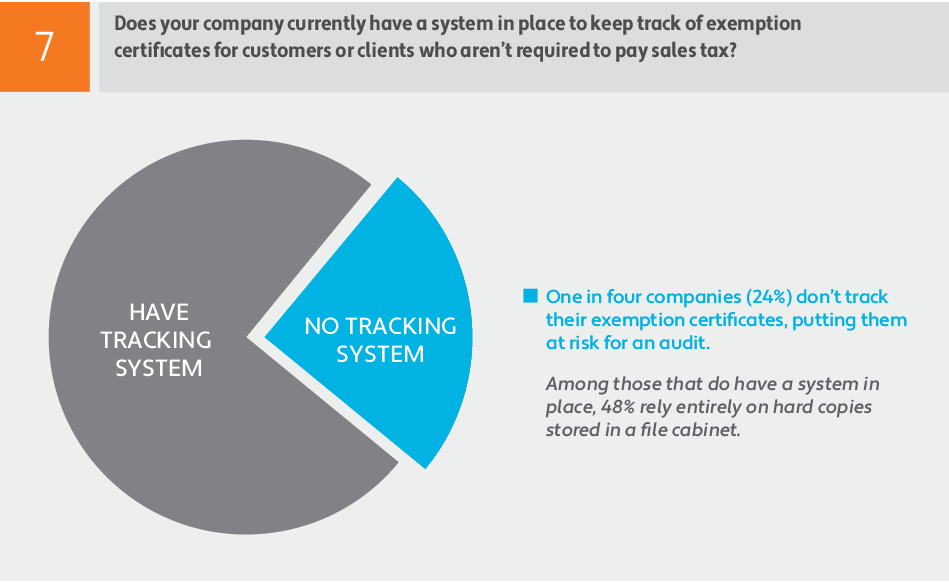

Question 7: Does your company currently have a system in place to keep track of exemption certificates for customers or clients who aren't required to pay sales tax?

Summary: One in four companies (24%) don't track their exemption certificates, putting them at risk for an audit. Among those that do have a system in place, 48% rely entirely on hard copies stored in file cabinets.

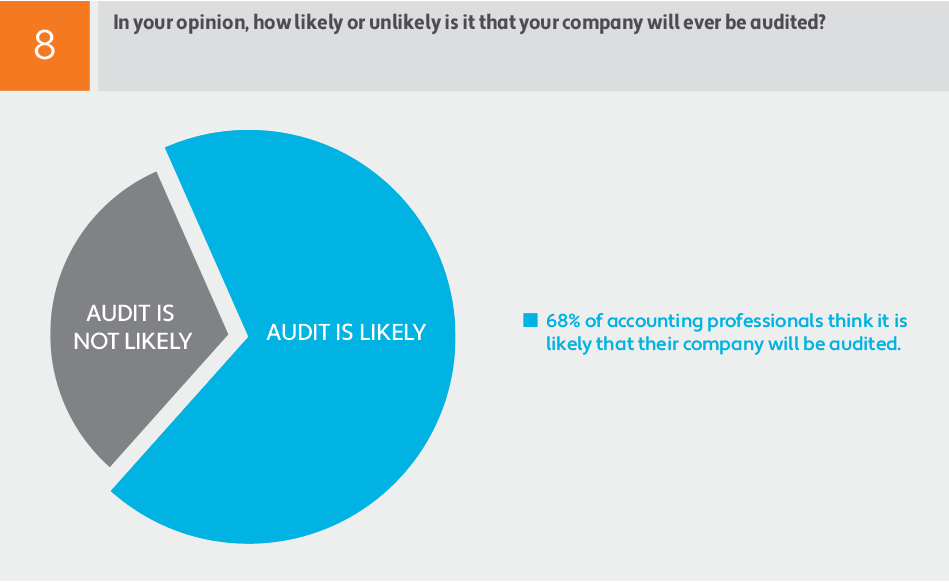

Question 8: In your opinion, how likely or unlikely is it that your company will ever be audited?

Summary: 68% of accounting professionals think it is likely that their company will be audited.

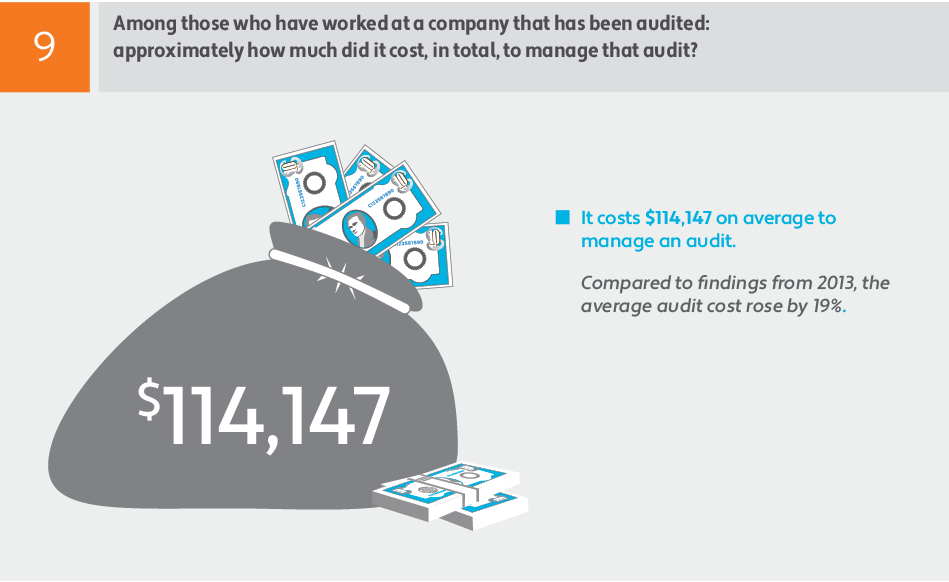

Question 9: Among those who have worked at a company that has been audited: approximately how much did it cost, in total, to manage the audit?

Summary: It cost $114,147 on average to manage an audit. Compared to findings from 2013, the average audit cost rose by 19%.

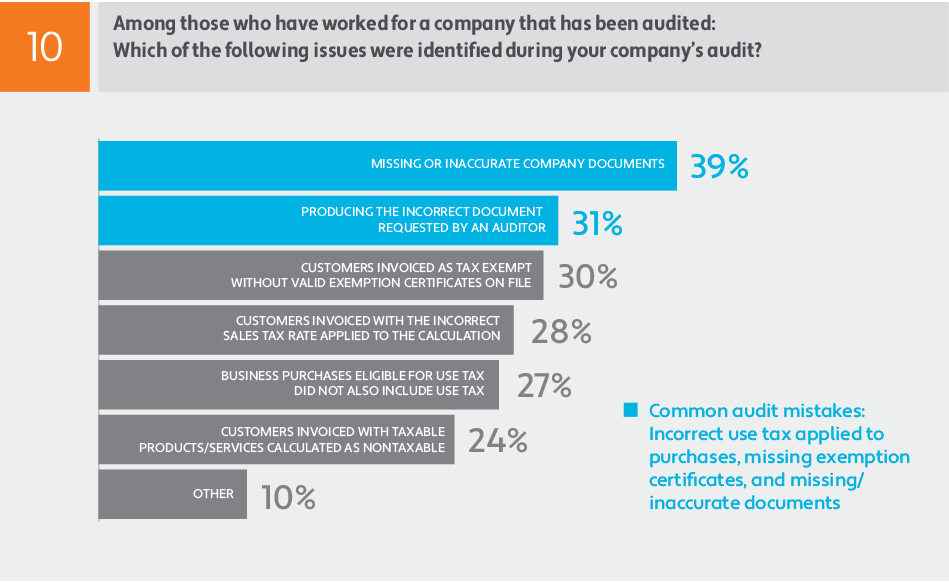

Question 10: Among those who have worked at a company that has been audited: Which of the following issues were identified during the company's audit?

Summary: Common audit mistakes: Incorrect use tax applied to purchases, missing exemption certificates, and missing/inaccurate documents.

Conclusion: Out-of-state nexus triggers are complex and expanding

Nexus (the physical and/or remote presence within a state that defines a tax obligation) is one of the most misunderstood, misinterpreted, and underestimated issues, making it a very common cause of tax problems.

At one time, companies could use a decision by the U.S. Supreme Court in Quill Corporation v. North Dakota (1992) as a guideline. In that case, it was simple: states could not require companies to collect state sales tax unless those companies had significant physical presence, like a warehouse or storefront. But that has all changed.

Now many states have redefined nexus with the emergence of e-commerce, and more and more services are now subject to sales tax. That creates even more tax planning problems and audit risk for companies.

It’s no surprise then that nearly 40% of survey respondents don’t know all of the states in which they’re obligated to remit sales tax—despite the fact that most of these companies sell online. And among those who feel confident in their knowledge of nexus, 89% still operate with misconceptions.

Supporting data

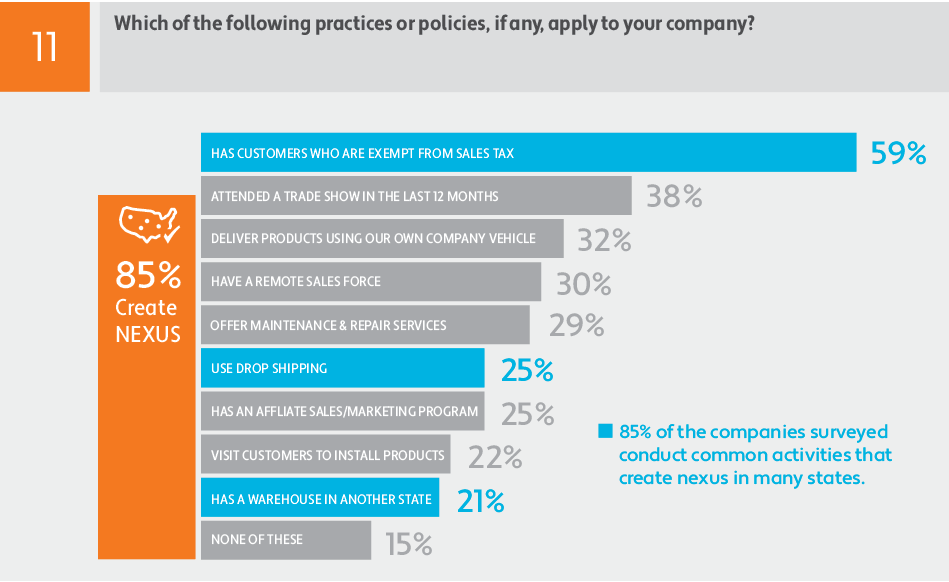

Question 11: Which of the following practices or policies, if any, apply to your company?

Summary: 85% of the companies surveyed conduce common activities that create nexus in many states.

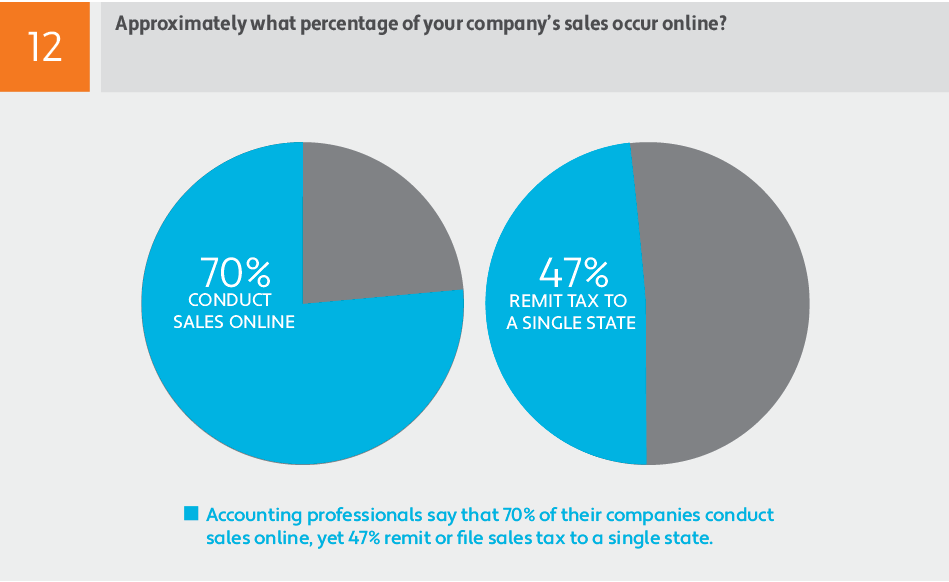

Question 12: Approximately what percentage of your company's sales occus online?

Summary: Accounting professionals say that 70% of their companies conduct sales online, yet 47% remit or file sales tax to a single state.

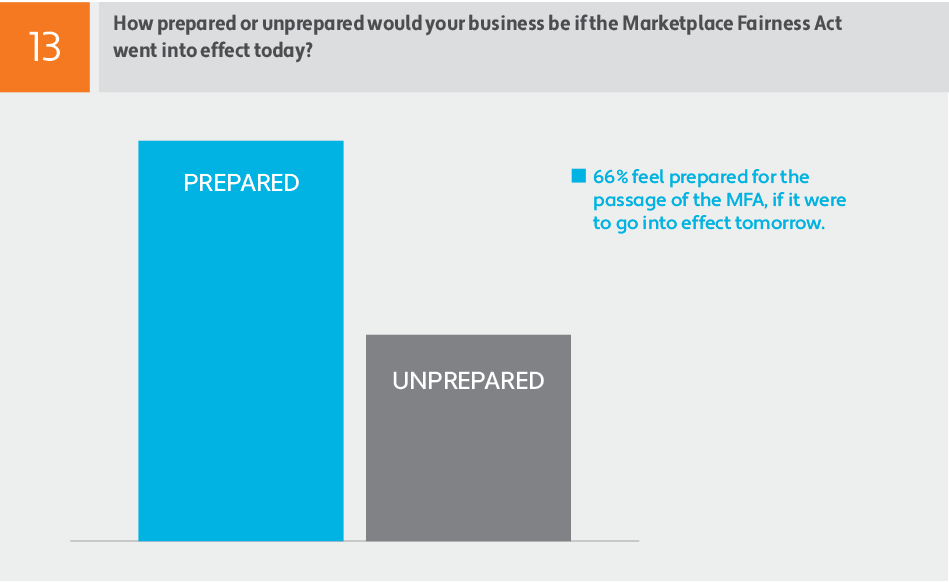

Question 13: How prepared or unprepared would your business be if the Marketplace Fairness Act went into effect today?

Summary: 66% feel prepared for the passage of the MFA, if it were to go into effect tomorrow.

The case for automating sales tax management

There are over 12,000 taxing jurisdictions in the U.S., many of which (e.g., Florida, Texas, California) are now requiring out of state ecommerce companies to collect sales tax for the first time. If federal legislation passes that effectively ends sales tax-free online shopping, the already difficult risk-prone sales tax problem will worsen. The solution? Automating the process with a cloud-based sales tax solution that resides within your business.

There is a reason automated solutions represent a cost efficient and comprehensive solution to the ever-present risk of state audits. They are, in essence, a revolutionary change in a marketplace that has come to recognize a consistent process and predictable workflow for all transactional tax reporting as fundamental to any audit strategy.

Automation is the clearest and best method to graphically display policies and procedures for a competent and, most important, compliant system of sales tax reporting. Organizations can have peace-of-mind knowing that their automated solution meets and exceeds standards that auditors expect from each business. Just as important, automated tax reporting can greatly diminish audit vulnerability-a best-case scenario for every business.

Reduce tax risk

Increase the accuracy of your tax compliance with our cloud-based tax engine and tax research services.