The mixed-up classification and taxation of RTDs

Ready-to-drink beverages are having a heyday in the United States. The ready-to-drink (RTD) category grew more than any other spirits category in 2022, and the RTD category value is expected to reach $11.6 billion through 2026. Such strong sales are causing some states to reconsider how to best classify — and tax — RTDs. When it comes to defining and taxing ready-to-drink beverages, there’s little if any consistency from state to state.

What is an RTD?

What is an RTD?

As the name suggests, an RTD is a beverage manufactured and packaged for immediate, easy, individual consumption. While that may call cans of beer to mind, RTD typically refers to drinks assembled from two or more ingredients, like cocktails, that are sold in a manufacturer-sealed container. RTDs usually contain alcohol, though there are nonalcoholic varieties.

A margarita prepared by your favorite Mexican restaurant for off-premises consumption is not a ready-to-drink beverage. The premixed, canned Jack Daniel’s & Coca-Cola RTD that hit the U.S market in March 2023 is.

The Alcohol and Tobacco Tax and Trade Bureau (TTB) doesn’t define ready-to-drink beverages, and every state defines RTDs differently, if at all.

For instance, Arkansas defines a ready-to-drink product as “a product containing spirituous liquor with a final finished product of no greater than 15% alcohol by weight.” A “mixed spirit drink” in Michigan is made with distilled spirits and other ingredients, has an alcohol by volume (ABV) of no more than 13.5%, and is packaged in metal cans; if packaged in any other type of container, a mixed spirit drink may not exceed 10% ABV. In Nebraska, a ready-to-drink cocktail is a beverage or other confection containing spirits in an original package that contains 12.5% or less ABV.

RTDs are commonly categorized by manufacturing method or the base alcohol ingredient:

- Malt (partially germinated cereal grains like barley) or malt substitute (including sugar);

- Spirits (gin, rum, tequila, vodka, whiskey, grain neutral spirits); or

- Wine (fermented grapes or other fruits).

Ingredients matter because they’re tied to tax: States typically tax beer and other malt-based beverages differently than distilled spirits, and liquor differently than wine. Many states have taken a similar approach to taxing RTDs.

How are RTDs taxed?

To understand how RTDs are taxed, it helps to start with a primer on how state excise taxes apply to beer, wine, and spirits.

State taxes on beer, wine, and spirits are linked to alcohol content

Tax rates tend to be linked to alcohol content. With a higher alcohol content than beer or wine, distilled spirits are taxed more heavily than beer or wine. Malt beverages have relatively low alcohol by volume and are subject to the lowest tax rates. A happy medium (stronger than beer but weaker than spirits), wine is typically taxed somewhere between the two.

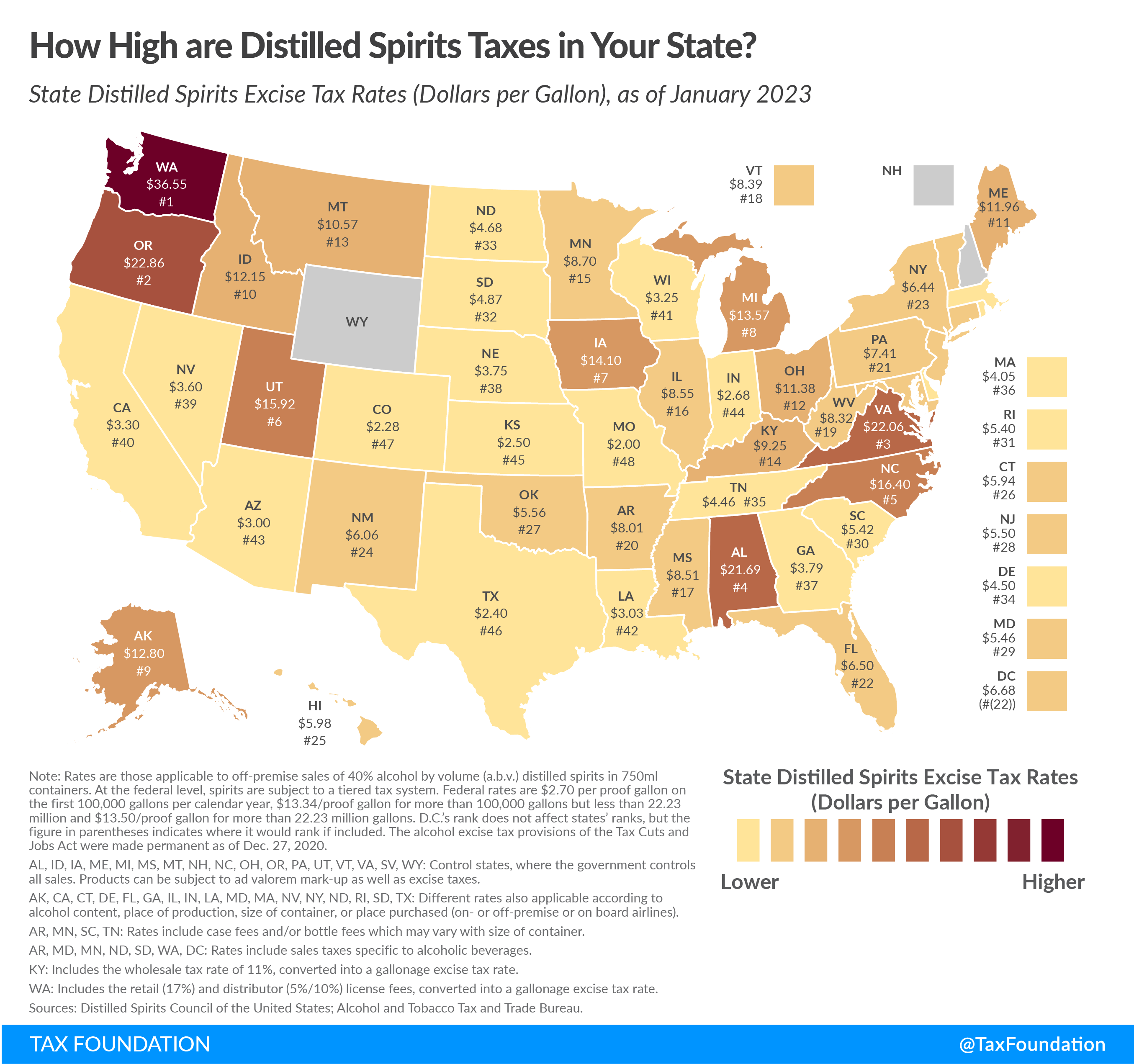

The following chart gives a taste of how different tax rates for alcoholic beverages can be from state to state (in dollars per gallon) — but just a taste. Beverage alcohol excise taxes are layered and complex, and the responsibility to pay them may fall on the manufacturer, retailer, or wholesaler, depending on the type of transaction.

RTD taxes tend to mimic taxes on spirits, wine, and beer

It’s common for states to tax RTDs based on their main alcohol ingredient, so in many states, spirit-based RTDs are subject to a higher tax than their malt-based and wine-based counterparts.

In West Virginia, for instance, a spirit-based RTD with 6% alcohol by volume (ABV) is taxed 35 times more than a malt- or sugar-based RTD with the same alcohol content. “The rate for malt- and sugar-based beverages with a 6% ABV is $0.02 per 12-ounce can,” according to the Distilled Spirits Council of the United States, “versus $0.71 per 12-ounce can of a spirits-based beverage.”

That’s not the case in every state. A February 2023 Ready-to-Drink Alcohol Tax Report by the Maryland Alcohol and Tobacco Commission notes that 25 states have a “Low Spirit” tax rate in addition to a “Full Spirit” tax rate. The lower tax rate applies to spirits with 24% or less ABV in New York but 6% or less ABV in Alabama. See the map below for more state-specific details.

Most of these states didn’t create the low-spirit rate with RTDs in mind. The low rate may apply to RTDs — but may not.

At least 12 states attempted to establish lower tax rates for “low-proof” spirit-based RTD beverages in 2021 and 2022: Alabama, Arizona, Hawaii, Kentucky, Maryland, Michigan, Minnesota, Nebraska, North Carolina, Vermont, Washington, and West Virginia. Only three states enacted the new laws:

Michigan SB144 (2021) reduced the excise tax rate for low-proof, spirit-based RTDs effective August 23, 2021.

Nebraska LB274 (2021) established a new tax rate for RTDs as of July 1, 2021. At $0.95 per gallon, the tax is significantly lower than the full spirits tax rate of $3.75 per gallon (though not as low as the $0.31 originally sought).

Vermont H730 (2022) lowered the rate and stipulated that RTDs not be sold through the state’s alcohol-controlled model. The new policy and tax rate took effect July 1, 2023.

Several states introduced legislation in 2023 to lower taxes on certain spirit-based RTDs and/or expand retail options for spirit-based RTDs, with little success. California SB-277 sought to allow more retailers to sell low-ABV spirit-based RTDs, but the bill stalled. A similar bill was left pending in committee in Texas, while a Pennsylvania bill was laid on the table.

IWSR Drinks Market Analysis expects industry advocates to continue to push for states to level the playing field by allowing spirit-based RTDs to be sold alongside their malt-based and wine-based counterparts. A more equitable tax policy could also help grow the spirit-based market. Even with existing policies, consumer taste for spirit-based RTDs is growing.

Consumption of ready-to-drink beverages grew more than 104% in the past two years, according to NielsenIQ, while the market for other alcoholic beverages contracted. If that rate of growth continues, it could encourage states to develop more consistent definitions for ready-to-drink beverages, and perhaps update their tax policies as well. If any do, we’ll let you know at the Avalara Tax Desk.

The Avalara Tax Changes midyear update is here

Trusted by professionals, this valuable resource simplifies complex

topics with clarity and insight.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.

{kind=link}