The trials and tribulations of sales tax in the United States

A guide to U.S. Sales Tax

Breaking into the U.S. without breaking the bank

Online retail is booming. In 2013, North America turned over €333.5 billion (U.S. $415 billon) via ecommerce, while Europe achieved sales worth €363.1 billion (U.S. $452 billion).1 Businesses are fighting for a share of the lucrative global market and looking at cross-border expansion.

In the rush to expand, however, merchants can overlook areas of international business that are unfamiliar. Ensuring you support international payments and have a logistics network capable of fulfilling orders is important, but with new opportunities come new complexities, particularly when meeting the challenge of sales tax compliance in the United States.

Businesses in Europe are used to dealing with transactional taxes in the form of VAT, but U.S. sales tax is a different prospect entirely. With over 12,000 taxing jurisdictions throughout the U.S., each empowered to alter rates and rules with little oversight, the complexity for companies trading in the U.S becomes mindboggling. With 100,000+ rules and boundary changes annually it’s easy to see why many companies require outside expertise to manage what initially seems like a straight forward process.

Where do you need to file and remit sales tax? On which items do you charge sales tax? What rate of sales tax do you need to charge for different addresses on the same street? What is the difference between state, county, city and special taxes? What records need to be kept in case of audit? How often do you file taxes and to which authority? And what on earth is nexus?

These are just some of the questions we hear every day from merchants either selling or planning to sell in the U.S. It’s a veritable minefield of legislation, regulation and complexity. However, sales tax should not

be feared.

What is Sales Tax?

As revenue from property taxes collapsed during the Great Depression in the 1930s, U.S. states implemented transactional taxes on commodities. As an indirect tax (a tax levied on goods and services), sales tax requires the seller to collect funds from the consumer at the point of purchase.

-

Today, there are over 12,000 state2 , county and city jurisdictions in the U.S. charging a sales tax.

-

Forty-five states and the District of Columbia now impose a sales tax on retail sales and some services. The bulk of their revenue is now generated from sales taxes, not income taxes. As an indication of the importance of sales tax to a state, in Texas, sales tax accounted for 54.3 percent of all its revenue in 2013.3

- The five states that do not have a state-wide general sales tax are Alaska, Delaware, Montana, New Hampshire and Oregon, although Alaska and Montana do allow localities to charge local sales taxes.

How does Sales Tax differ from Value Added Tax (VAT)?

Many businesses are familiar with VAT and may assume that they can apply current

processes to U.S. sales tax. However, VAT is applied every time value is added at each stage during the supply chain, whereas sales tax is collected only at the time of the final sale.

If a seller has nexus in a state, more on that to follow, they must collect sales tax on all taxable sales regardless of the channel.

Just how complex is Sales Tax?

Depending on the state in which your customer is based, different items may be taxed at different rates. In some states, for example, food is not taxed, while in others the same item may be classified differently. So far so good.

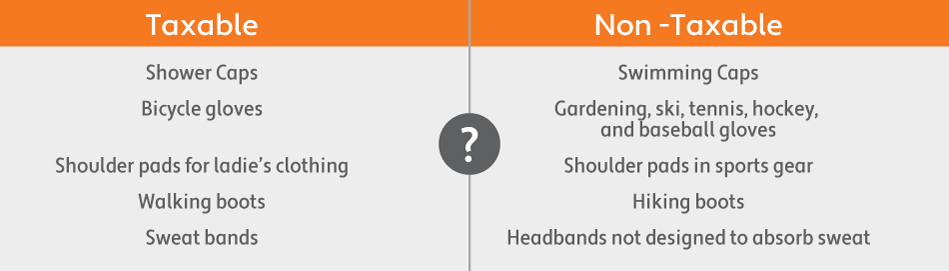

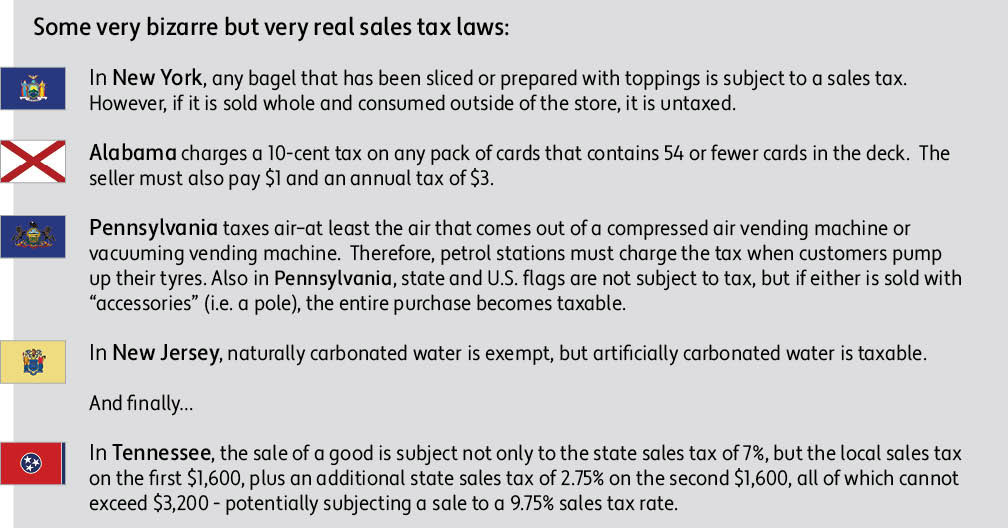

In New York, clothing and footwear costing less than $110 per item/pair is exempt from state sales tax, yet it is still subject to local sales tax in some jurisdictions. Local jurisdictions can change their tax policy towards clothing once a year, however, “most fabric, thread, yarn, buttons, snaps, hooks, zippers and similar items that become a physical component of clothing” or are used to repair it are exempt. Even specific types of clothing can be taxed differently [see figure below].

To be compliant, a retailer needs to know the correct classification of an item in each state to ensure it collects and remits the correct level of tax. Collecting too much in one state will make it uncompetitive, while not collecting enough increases its exposure to potential fines. Adding to the complexity, in some states the rates can vary by city, county, or even street. Two adjacent properties can have different tax rates.

While manually calculating tax rates is commonplace in Europe, more and more businesses in the U.S. automate the process to save time, money and reduce their risk of fines.

The Risk of Audit

In an effort to safeguard sales revenue, each state conducts audits of businesses, which may result in penalties and interest. Businesses must keep records of sales in each U.S. city, county and state in which they sell. California alone announced in August 2014 the hiring of 100 auditors, lawyers and specialists to help collect online sales tax.4

As more businesses sell in the U.S., auditors are also turning to international sellers to ensure they do not have a competitive advantage over domestic retailers. The financial importance of collecting sales tax on a state cannot be underestimated. The more auditors assessing international business, the more revenue a state can make in penalties and unpaid tax.

With the average audit costing as much as €79,0005 (U.S. $100,000) you can’t afford to be complacent about compliance.

Nexus: Do I have to collect U.S. Sales Tax?

International businesses selling in the U.S. are not required to collect sales tax in a state unless they have ‘nexus.’ Nexus is defined as a connection or business presence in a state or jurisdiction. If you have nexus in a state, you need to collect and remit sales tax according to their regulations. Activities leading to having nexus vary per state and can include activities such as opening offices, stores or franchises, storing items in warehouses or even attending meetings or tradeshows. Determining nexus can be confusing if you are unprepared or do not fully understand the obligations. This will ultimately increase your business’ exposure during potential sales tax audits.

Once you have determined where nexus exists for your business, you are required to calculate, collect, report and remit that state’s sales tax. For this reason, sales taxes are remitted based on where your business is actually located because it is the physical structure of the business that actually creates nexus. However, there are several other scenarios where nexus can be applied and these should also be considered.

What constitutes a ‘significant physical presence’?

Nexus rules are established by individual states and every state defines them uniquely. Determining exactly how a rule applies to a business is critical. With more than 12,000 sales tax jurisdictions across North America and with rates and boundaries constantly changing, staying on top of nexus responsibilities is a substantial drain on businesses, carrying no benefit to the bottom line. The regular presence of a single sales person is enough to create tax nexus, therefore requiring the collection of sales tax.

Recently, in an effort to avoid losing taxes to companies that locate themselves in areas with low or no tax rates, many states have enacted Amazon laws to require more national and international online retailers to collect sales tax for the first time. These laws expanded definitions of nexus to include online-specific relationships such as affiliate and web advertising.

Scenarios that could trigger Nexus and Sales Tax obligations:

Scenario #1

Your international business has a presence in multiple states. It could take the form of a store, or even a concession within a larger retail establishment. In this case, you will more than likely have sales tax obligations in each location.

Scenario #2

Nexus can be created by employing sales people who work in the states. For example, if your employees or contractors conduct any work for a customer in the U.S., you may have created nexus in that state.

Scenario #3

Regularly attending tradeshows or advertising in the U.S. can be considered nexus in certain states.

Additional factors that can create nexus obligations are:

- Property Ownership: Owning or leasing any real or personal property in the U.S.

- Product Delivery: Having company personnel deliver/install products in the U.S.

- Product Storage: Renting or owning storage, warehousing or drop-shipping facilities

Sales tax compliance is full of complicated rules and nexus is just one aspect. Several other layers must also be considered in order to be fully compliant.

To safely navigate these challenging tax rules, businesses should understand their exposure as part of a nexus study. Making the nexus determination on your own is difficult, confusing and can lead to problems further down the road.

Top 8 areas to consider in your business plan for selling in the U.S.

1. Keep up to date with each states tax requirements

Businesses need to keep up to speed on all the changes made by states and municipalities each year. These changes include rate increases/decreases as well as new sales taxes added to jurisdictions.

2. Establish processes for water tight record keeping

The best way to stay compliant is to keep up to date on filing sales tax returns and

payments (quarterly or monthly, depending on the state’s requirements) and keep

accurate and detailed sales records.

What records do business need to keep?

- Sales invoices

- Paid bills

- Contracts

- Purchase orders

- Register tapes

- Bank statements

- Cancelled cheques and similar original documents

- Depreciation schedules and other fixed asset records

- Documents supporting tax-exempt sales, such as resale and other exemption certificates

- Freight bills indicating shipments to addresses across states

If this sounds long or complicated, unfortunately it is!

Keeping records and preparing and filing sales tax returns can be a major headache, particularly for small businesses. Tax automation can help reduce this tedious, labour intensive task and can save money in the long run.

3. Understand your Nexus requirements

Every state has the right to define who has to collect sales tax, what those taxes are and any allowable exemptions. However, there are limits to how states can define nexus. Ecommerce merchants must have a connection to a state in which a customer resides for the merchant to be liable for sales tax. However, states define nexus in different ways, which can make the process confusing.

The way you deliver goods sold in online transactions can also have a huge impact on your tax obligation. Many European businesses selling in the U.S. online use drop shippers to deliver goods, creating complicated tax obligations. Using any third party, whether it is a drop shipper, supply chain, or online affiliate, can trigger nexus for your business.

4. Plan to use Geolocation over Zip Codes

While the U.S. Postal Service has established ZIP Codes for mail delivery, tax jurisdictions do not generally follow ZIP Codes.

Going down to street level is essential to get it right. Businesses relying solely on zip code often find big discrepancies during audits. In order to help businesses cope with these differences, providers of automated solutions continually research the physical boundaries of taxing jurisdictions nationwide. Without the use of geospatial technology, there is simply no way, in many cases, to accurately determine which jurisdiction applies to a transaction.

5.Set out your Returns Filing and Remittance Schedule

Each U.S. state has its own set of rules and regulations for filing and remitting tax, which may differ from other states. In addition to state rules, cities and counties may impose and manage sales tax returns on their own.

Responsibility lies with businesses to not only determine if they have to file with specific cities and counties, but also to register of their own accord.

Moreover, filing frequencies vary by jurisdiction so not all returns are due on the same day of the month. When dealing with multiple states and local jurisdictions, the number of due dates and filing schedules that must be managed can be daunting.

Filing methods can vary just as much, even within the same state or municipality. Some states now require sales tax returns to be filed electronically; others still require hard-copy submission, while a few states offer online filing along with an electronic data interchange (EDI) option.

These tasks are necessary, but can be time consuming and prevent employees from engaging in more value-added efforts to build the business.

6.Collect and store all exemption certificates

Not everyone is required to pay sales tax. Depending on the rules in the taxing jurisdiction, certain businesses and individuals may be exempt from sales tax. The vendor must collect and keep on file a valid exemption certificate for each business, organisation or individual with an exemption.

It is also up to vendors to ensure that exemption certificates are valid for each sales transaction. This requires businesses to keep a copy of each exemption certificate and ensure that they are renewed when they expire.

7.Identify if the ‘Streamlined Sales & Use Tax Agreement’ is right for you?

Currently many states have worked together on an agreement called the Streamlined Sales and Use Tax Agreement, designed to “simplify and modernise sales and use tax administration in order to substantially reduce the burden of tax compliance.” Signing up to SST requires only one form to register across all SST states, Once registered, businesses then have to file returns every month.

For companies selling, or looking to sell in the US, or affiliate relationships in a number of states, registering as an SST volunteer can save you a lot of time, effort and money. There is no cost for registration and if you qualify, filing is a free service across the SST states. SST volunteers have limited audit exposure (no negative audits possible). Full SST Member States include:

Arkansas, Georgia, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Nebraska, Nevada, New Jersey, North Carolina, North Dakota, Oklahoma, Ohio, Rhode Island, South Dakota, Utah, Vermont, Washington, West Virginia, Wisconsin, Wyoming

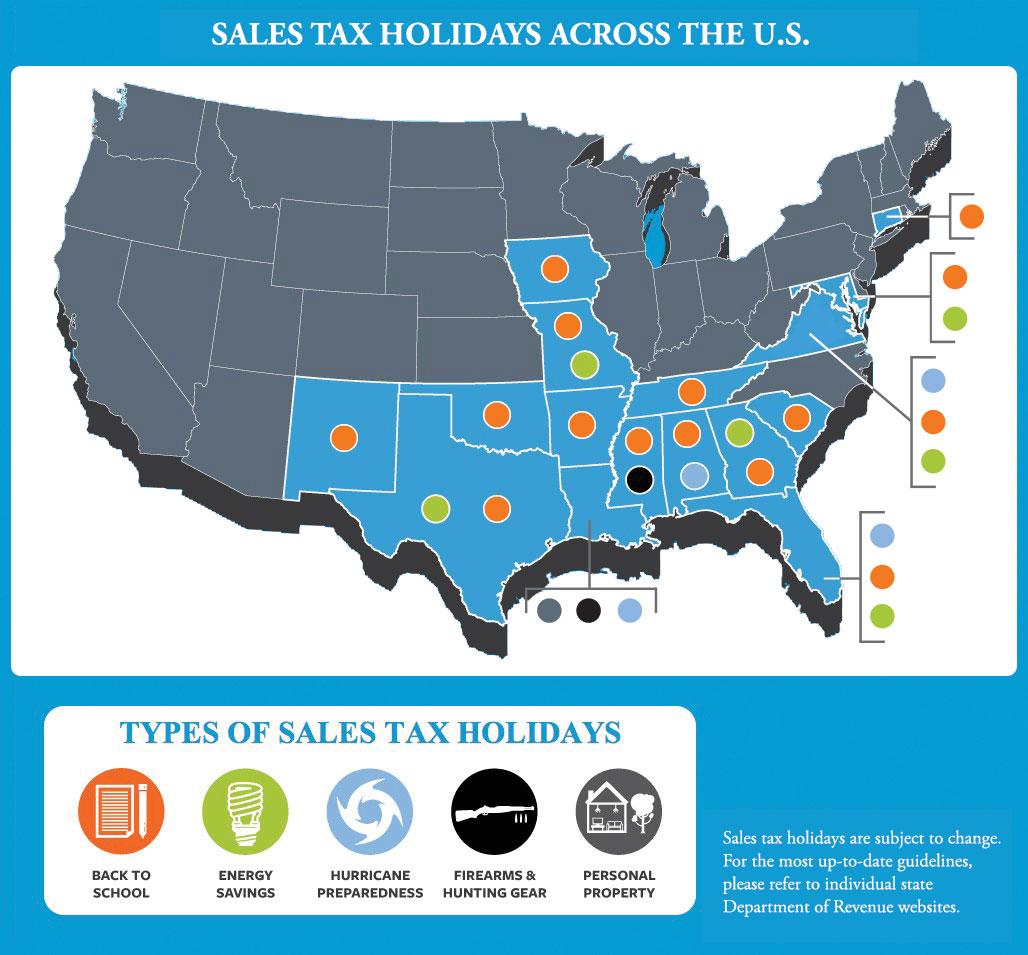

8.Plan for Sales Tax holidays

Further complicating the matter, dozens of states also declare sales tax holidays. Some states offer tax reprieves for products like school clothing for kids, while others give consumers a tax break on hurricane preparedness items, like plywood and nails. In states where hunting is a big business, tax holidays might be in place for firearms, ammunition and hunting supplies.

The holidays are varied and complicated, often taking place over specified dates and limiting the number of items that can be purchased tax-free.

In Virginia,6 for example, during the sales tax holiday for clothing and school supplies, many items are singled out as exempt. For clothing, this includes clerical vestments, choir and alter clothing, corsets, girdles, lingerie, purchased costumes, steel-toed shoes, suspenders, formal wear, etc. However, protective gloves, hard hats and helmets are taxable. School supplies that are exempt include calculators, binders, erasers, lunch boxes, highlighters, notebooks, paintbrushes, scissors, etc.

Steps to success

International trade is a great way to grow your business, so don’t be put off by the complexities of sales tax. Expansion need not be daunting and provided you take the right steps, selling your products in American markets could be the boost your business needs.

Or you could just automate everything...

Avalara can help to automate your sales tax compliance.

We offer a full suite of professional services including nexus studies that help to identify your obligations and registration services to ensure compliance when you expand in the U.S. Our cloud-based Avalara AvaTax technology integrates with hundreds of ERP and ecommerce platforms to bring tax automation into your expanding business, both in terms of calculating accurate taxes as well as filing and remittance.

To find out more about successfully managing sales tax and growing your business in the United States and around the world, get in touch today:

1http://www.euractiv.com/sections/innovation-enterprise/asia-pacific-outstrips-europe-worlds-largest-e-commerce-market-302859

2http://www.avalara.com/about/press/

3http://www.dallasfed.org/assets/documents/research/swe/2014/swe1403.pdf

4http://www.businessweek.com/ap/2012-08-31/california-to-seek-sales-tax-from-online-retailers

© Avalara Rev 111616

Contact us at: 877-780-4848