Illinois requires remote sellers and marketplaces to collect local sales tax starting January 2021

Update. This post was originally written in December 2020.

To create a more level playing field between in-state and out-of-state retailers, Illinois changed its sales tax laws. Effective January 1, 2021, most remote retailers with an obligation to collect sales tax in Illinois must collect local taxes in addition to state tax, as in-state businesses generally do. Collection requirements for marketplace facilitators also changed.

Behind the curtain of Illinois sales and use tax

Illinois has an extremely complex sales and use tax system. In fact, “sales tax” in Illinois “actually refers to several tax acts”:

- Retailers’ occupation tax, or ROT (applies to tangible personal property)

- Service occupation tax (applies to services)

- Service use tax (applies to services)

- Use tax (applies to tangible personal property)

The difference between retailers’ occupation tax and use tax is more than semantic.

The use tax rate is 6.25% for general merchandise and 1% for qualifying food, drugs, and medical appliances. According to Scott Peterson, vice president of Government Relations at Avalara, “The state use tax includes a percentage that is allocated to local governments.” Because of this, retailers that collect use tax don’t have to calculate local taxes.

Retailers required to collect retailers’ occupation tax must collect the state rate plus the local tax rate in effect at the location of the sale. If destination sourcing governs the transaction, that’s the rate in effect at the point of delivery. If origin sourcing rules apply, it’s the rate in effect at the point of sale or where the order is fulfilled. See Sales tax sourcing: How to find the right rule for every transaction to learn more about sales tax sourcing.

New sales tax collection requirements for remote retailers

Illinois has enforced economic nexus since October 1, 2018. Out-of-state sellers with no physical presence in Illinois (i.e., remote retailers) must register then collect and remit tax on sales into the state if, in the preceding 12 months, they meet one of the following economic nexus thresholds:

- $100,000 or more in cumulative gross receipts from sales of tangible personal property to purchasers in Illinois; or

- 200 or more separate transactions for the sale of tangible personal property to purchasers in Illinois.

Prior to January 1, 2021, remote retailers with economic nexus were generally required to collect the state use tax on sales delivered into the state (not state and local retailers’ occupation tax).

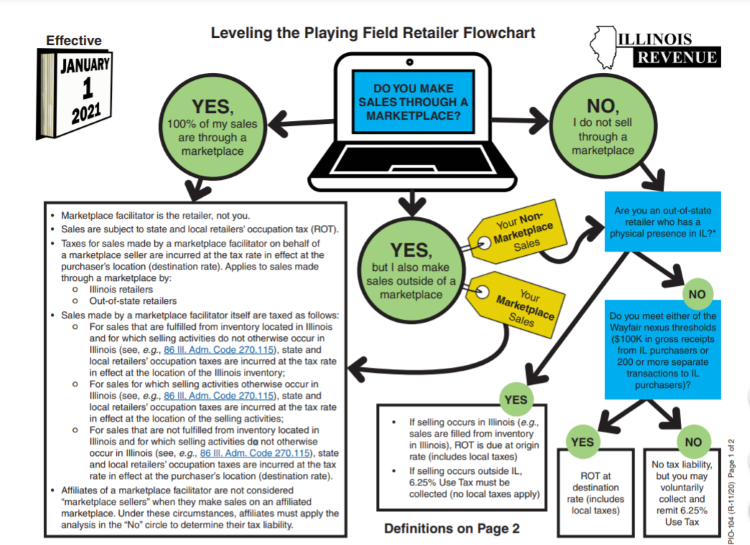

Starting January 1, 2021, remote retailers with economic nexus must collect state and local retailers’ occupation tax on sales delivered to consumers in Illinois, at the rate in effect at the point of delivery.

Out-of-state retailers with inventory in Illinois

Note that different rules may apply to out-of-state retailers with inventory in the state of Illinois.

If the inventory is used strictly to fulfill marketplace orders, it doesn’t affect the collection requirements for the seller’s direct sales. However, if the inventory is used to fill direct sales in addition to marketplace sales, it can.

The Illinois Department of Revenue (IDOR) explains: “When your sale is fulfilled from inventory located in Illinois, you will incur state and local retailer’s occupation taxes at the rate in effect at the location of the inventory (origin rate).” When the sale is fulfilled from inventory located out of state, “you incur use tax.”

Out of-state retailers making both direct and marketplace sales

Remote retailers that make both direct and marketplace sales into Illinois and have economic nexus with the state are responsible for the tax due on their direct sales prior to January 1, 2020. But as of January 1, 2020, marketplace facilitators with a physical presence in Illinois or economic nexus with the state are responsible for collecting and remitting the tax due on sales made through the marketplace.

And as with remote direct sellers, the collection requirements for marketplace facilitators changed on January 1, 2021.

New sales tax collection requirements for marketplace facilitators

For marketplace facilitators with distribution or fulfillment centers in Illinois, sales tax compliance is now more complex. As of January 1, 2021, all sales made through the marketplace are subject to state and local retailers’ occupation tax instead of use tax — but some sales are subject to origin sourcing rules and some to destination sourcing rules.

Destination sourcing governs all marketplace (i.e., third-party) sales, whether the marketplace seller is based in Illinois or another state. Thus, the marketplace facilitator must collect the state and local ROT at the rate in effect at the point of delivery.

Destination sourcing also governs any direct sales by a marketplace facilitator that are shipped from out of state. For these transactions, the marketplace facilitator must collect and remit the state and local ROT rate in effect at the point of delivery.

However, origin sourcing rules govern direct sales by a marketplace facilitator that are fulfilled in or shipped from a location in Illinois. The marketplace must collect the state and local ROT rate in effect where the selling occurs.

There are three possible scenarios:

- If sales are fulfilled from inventory in Illinois but no other selling activities occur in Illinois, ROT is based on the rate in effect at the location of the Illinois inventory.

- If sales are fulfilled from inventory in Illinois and selling activities also occur in Illinois, ROT is based on the rate in effect at the location of the selling activities (e.g., where the order was taken).

- If sales are not fulfilled from inventory in Illinois and selling activities don’t occur in Illinois, ROT is based on the rate in effect at the point of delivery.

Affiliates of a marketplace facilitator aren’t considered marketplace sellers, so they follow sales tax sourcing rules for retailers (see previous section).

To help retailers and marketplace facilitators figure out their collection obligations, the IDOR has created a nifty flow chart.

Retailers and marketplace facilitators will likely find this new system confusing. They’re unlikely to be alone.

Consumers may be confused

Consumers shopping through an online marketplace may also wonder why different tax rates apply to different sales.

Imagine a customer purchases five items through a marketplace and has them delivered to their home in Paw Paw. Three items are sold by a third-party vendor, and two are direct sales sold by the marketplace itself; all five are shipped from the marketplace facilitator’s fulfillment center in Joliet, Illinois. The three items sold by the marketplace seller are taxed at the rate in effect in Paw Paw, while the two items sold by the marketplace facilitator are taxed at the rate in effect in Joliet.

The IDOR provides numerous examples to help taxpayers understand their new obligations at Registration Examples for Marketplace Facilitators and Remote Retailers. Additional information can be found on this resource page.

It’s complicated, but it’s complicated for a reason. As Illinois works to revise its tax system, it must ensure existing revenue streams aren’t overly impacted. Scott Peterson explains, “The state use tax includes a percentage that is allocated to local governments. One of the state’s complexities is minimizing who stops paying the use tax, as local governments that get that money today expect to get it tomorrow.”

Easing the burden of compliance

The Illinois Department of Revenue encourages remote retailers to ease the burden of compliance by using a certified service provider (CSP) to collect and remit sales and use tax on their behalf. Alternatively, retailers can use a certified automated system (CAS) to help them calculate the proper retailers’ occupation tax rate.

Learn how Avalara AvaTax can reduce the pain of tax compliance in Illinois and other states at avalara.com.

A word about other taxes

The IDOR has published guidance on other taxes it administers, including the Chicago Home Rule Municipal Soft Drink ROT.

Marketplace facilitators are liable for taxes due on their direct sales, and they must collect and remit Chicago Home Rule Municipal Soft Drink Retailers Occupation Tax (ROT) on behalf of marketplace sellers located in Chicago. However, marketplace facilitators generally aren't liable for these other taxes on sales they facilitate for a third-party.

IDOR encourages marketplace sellers to “make arrangements with their marketplace facilitators to collect and provide these taxes to the marketplace sellers along with the gross receipts from the sale.” In such cases, the marketplace sellers would remit the taxes to the IDOR as required.

The Avalara Tax Changes midyear update is here

Trusted by professionals, this valuable resource simplifies complex

topics with clarity and insight.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.