State-by-state guide to non-collecting seller use tax

Not having to collect sales tax in a state doesn’t necessarily mean you’re entirely off the hook for sales and use tax. More than a dozen states require remote retailers and/or marketplace facilitators or providers (e.g., Amazon, eBay, etc.) that don’t collect sales and use tax in the state to report consumer purchase information to state tax authorities and the consumers themselves if they meet certain criteria.

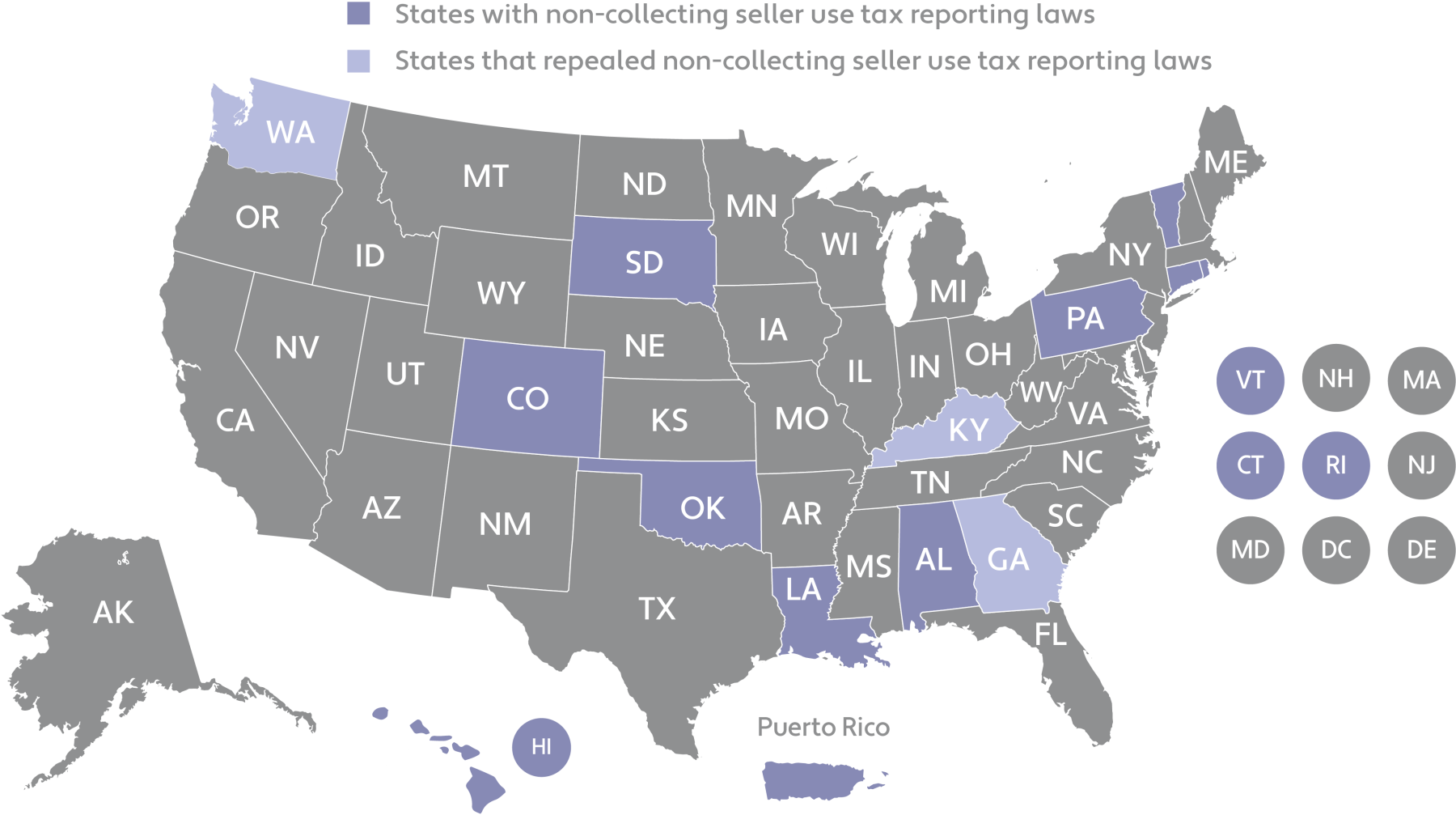

Non-collecting seller use tax reporting requirements by state

Last updated March 24, 2021

Non-collecting seller use tax reporting laws vary by state but generally require non-collecting sellers to:

- Notify customers of their obligations to report and pay use tax since sales/use tax was not collected on their purchase

- Provide an annual purchase summary to customers

- Send an annual customer information report to the state tax authority

Failure to comply with a state’s non-collecting seller use tax reporting law can lead to costly fees and penalties, which vary by state. However, complying with non-collecting seller use tax reporting requirements may pose a different kind of risk: It could anger customers who don’t want their information provided to the state tax authorities.

To help you better understand which states have non-collecting seller use tax reporting requirements and what's expected in each state, we’ve outlined the individual state requirements below. For more information or assistance in determining your sales tax registration, collection, and remittance requirements, contact Avalara Professional Services.

Although we hope you’ll find the information helpful, this guide does not offer a substitute for professional legal or tax advice. If you have questions about your tax liability or concerns about compliance, please consult your qualified legal, tax, or accounting professional. This information was compiled in May 2019. Because states constantly update and amend their sales and use tax laws, see each state’s tax authority website for the most up-to-date and comprehensive information.

Reduce tax risk

Increase the accuracy of your tax compliance with our cloud-based tax engine and tax research services.

Alabama

Enforcement date:

January 1, 2019

Requirements:

Marketplace facilitators with no physical presence in the state and more than $250,000 in annual Alabama sales must elect to register to collect Alabama’s Simplified Sellers Use Tax or comply with use tax notice and reporting requirements.

Additional information:

Sales and Use Tax Rules

Alabama Department of Revenue Simplified Sellers Use Tax (SSUT); Act 2018-539

Colorado

Enforcement date:

July 1, 2017

Requirements:

Non-collecting remote retailers must comply with notification and reporting requirements for Colorado customers and the Colorado Department of Revenue. Specific requirements apply to non-collecting vendors with more than $100,000 in gross sales into Colorado.

Additional information:

Use Tax – Information for Non-Collecting Retailers

Use Tax Reporting Instructions Format & FAQ for Non-collecting Retailers

HB 10-1193

Connecticut

Enforcement date:

December 1, 2018

Requirements:

Starting December 1, 2018, non-collecting referrers that receive more than $125,000 during the prior 12-month period for listing or advertising a seller’s products must comply with notification requirements. By July 1, 2019, such referrers must also send a quarterly notice to each seller that was referred a potential Connecticut purchaser during the previous calendar year. And starting January 31, 2020, such referrers must electronically submit an annual report to the Connecticut Department of Revenue Services that includes the name and address of each seller that received a notice from the referrer.

Additional information:

SB 417

Legislative Changes Affecting ... Sales and Use Taxes

Georgia

Enforcement date:

January 1, 2019; repealed effective April 28, 2019

Requirements:

Remote sellers that did not have an obligation to collect Georgia sales and use tax before January 1, 2019, and have more than $250,000 in retail sales or conduct at least 200 transactions of tangible personal property for delivery (electronically or physically) in Georgia in the current or previous calendar year must comply with certain notification requirements as of January 1, 2019. Additional reporting requirements apply for customers with more than $500 in aggregate annual sales from the seller.

Additional Information:

Policy Bulletin SUT-2019-02

HB 61

Hawaii

Enforcement date:

January 1, 2020

Requirements:

Any person other than a marketplace facilitator who provides a forum in which sellers list or advertise tangible personal property for sale and take or process orders must notify potential consumers of potential use tax responsibilities both on the forum and in writing at the time of sale. Non-collecting forum providers must also send an annual report containing the name and address of purchasers and sellers, along with the aggregate dollar amount of the purchases, to the Hawaii Department of Taxation.

Additional information:

SB396 SD1

Kentucky

Enforcement date:

July 1, 2013; repealed effective July 1, 2019

Requirements:

Out-of-state retailers with no obligation to collect Kentucky sales tax and more than $100,000 in gross sales in the state must obtain a Kentucky sales tax permit or notify customers that Kentucky use tax must be paid directly to the Department of Revenue.

Additional information:

Consumer Use Tax

HB 354

Louisiana

Enforcement date:

July 1, 2017

Summary:

An out-of-state vendor that isn't required to collect Louisiana sales or use tax — but purposefully avails itself of the Louisiana market and makes at least $50,000 in annual retail sales of tangible personal property or taxable services in the state per calendar year — must notify consumers of their consumer use tax obligation. They must also provide purchasers and the Department of Revenue with an annual statement that includes the total amount paid by the purchaser to the retailer in the preceding calendar year and informs consumers of their use tax obligations. Non-collecting remote retailers with more than $100,000 in annual sales in the state must file the annual statement electronically.

Additional information:

Information Bulletin No. 18-006

HB 1121

Nevada

Enforcement date:

October 1, 2019

Requirements:

As of November 1, 2019, non-collecting remote referrers that refer Nevada consumers may be allowed to opt out of collecting sales tax if they comply with use tax notice and reporting requirements. This applies to referrers with more than $100,000 in cumulative gross receipts from retail sales to Nevada customers resulting from referrals from the referrer's platform, or at least 200 separate retail sales transactions from such referrals. The referrer must post a conspicuous notice on each platform explaining sales and use tax obligations, provide a monthly notice to each marketplace seller to whom a potential customer was referred, and provide periodic reports to the Department of Revenue. The non-collecting use tax notice and reporting is only available to referrers.

Additional information:

AB 445 Marketplaces responsible for tax on third-party sales

Oklahoma

Enforcement date:

November 1, 2016; July 1, 2018

Requirements:

As of November 1, 2016, non-collecting remote vendors that make sales to Oklahoma consumers must inform customers of their obligation to report and pay Oklahoma use tax and provide to each Oklahoma buyer of taxable goods a statement of the total sales made to the customer during the preceding calendar year. As of July 1, 2018, remote sellers, marketplace facilitators, or referrers with aggregate sales of at least $10,000 in Oklahoma must file an election with the Tax Commission to collect and remit sales and use tax or comply with additional notice and reporting requirements.

Additional information:

HB 2531

HB 1019XX

Remote Sellers

Wayfair Decision and HB 1019XX

Pennsylvania

Note: Act 13 of 2019 removed the election and reporting requirements for sellers located outside of Pennsylvania.

Enforcement date:

March 1, 2018 (April 1, 2019, for digital products)

Summary:

A remote seller, marketplace facilitator, or referrer with annual Pennsylvania taxable sales of greater than $10,000 but less than $100,000 in total sales must make an election to collect and remit sales tax or comply with notice and reporting requirements.

Non-collecting seller use tax reporting:

Remote Sellers

2017 Act 43

Puerto Rico

Enforcement date:

July 1, 2017

Requirements:

Non-collecting remote sellers are required to inform consumers in writing of their obligation to report and pay use tax on taxable purchases and send annual reports to customers and the Secretary of the Treasury.

Additional information:

Administrative Determination no. 17-04

Puerto Rico to require use tax notification and reporting, July 2017

Rhode Island

Enforcement date:

August 17, 2017

Summary:

Non-collecting retailers with $100,000 in gross revenue or 200 or more transactions of taxable goods or services in the state in the preceding calendar year must voluntarily collect or comply with various notice requirements. These include: posting a notice that they don’t collect Rhode Island sales tax on their website and at checkout; sending a notice to the customer within 48 hours of the purchase; sending an annual notice by January 31 to Rhode Island customers with at least $100 in annual purchases; and providing an annual attestation that the notice requirements were fulfilled by February 15 of each year. Referrers that receive more than $10,000 in compensation from referrals must notify retailers that their sales may be subject to Rhode Island sales and use tax. Retail sale facilitators (marketplace facilitators) meeting the threshold must provide a list of names/addresses of retailers for whom they collected and did not collect Rhode Island sales tax.

Additional information:

Non-collecting retailers, referrers, and retail sales facilitators

Notice to All Non-Collecting Retailers

Summary of Legislative Changes

FAQs for non-collecting retailers (remote sellers) following Wayfair decision

South Dakota

Enforcement date:

July 1, 2011

Requirements:

All non-collecting retailers with annual gross sales in South Dakota of $100,000 or more are required to give notice to customers on their billing statement and receipt that South Dakota use tax is due to the South Dakota Department of Revenue on non-exempt purchases of tangible personal property, services, and products transferred electronically. Businesses that have an obligation to collect South Dakota sales tax through the state's economic nexus or marketplace provider laws must comply with registration and filing requirements. Businesses that don't fit those criteria but fit the criteria of SDCL ch. 10-63 must comply with the notice requirements.

Additional information:

South Dakota Sales Tax Public Notice for Non-Collecting Retailers

Vermont

Enforcement date:

July 1, 2017

Requirements:

All non-collecting vendors with no obligation to collect Vermont sales tax must provide a transactional notice with every taxable Vermont purchase. In addition, non-collecting sellers must send a list of total purchases made by the consumer during the previous calendar year to Vermont consumers who made at least $500 worth of purchases during that time. Also, non-collecting vendors that made $100,000 or more in Vermont sales in the previous year must provide the Department of Taxes an annual customer information report for every purchaser required to receive an annual purchase summary.

Update: Effective January 1, 2020, non-collecting vendors making $100,000 or more in Vermont sales in the previous year are no longer required to provide an annual customer information report to the Department of Taxes. Vermont's economic nexus law requires out-of-state vendors with $100,000 in sales or 200 transactions in the preceding 12 months to register with the department and collect and remit sales tax.

Additional information:

Washington

Enforcement date:

January 1, 2018; repealed effective July 1, 2019

Summary:

Marketplace facilitators, remote sellers, and referrers selling their own goods must register then collect and submit Washington sales and use tax or comply with the use tax notice and reporting requirements if they make between $10,000 and $100,000 in annual gross retail sales to Washington consumers. If they make more than $100,000 in sales in the state, they’re required to collect and remit Washington sales and use tax.

Additional information:

2019 sales tax legislation, Wayfair

Wayfair’s impact on the Marketplace Fairness Act

New law updates Washington state tax requirements for out-of-state businesses

For additional details on the ins and outs of non-collecting seller use tax requirements, review our guide

Non-collecting seller use tax reporting is just one of the requirements that can be imposed on remote sellers. To learn more about remote seller sales tax nexus laws, view our sales tax nexus laws by state resource.

If you'd rather collect sales tax than deal with non-collecting seller use tax notice and reporting requirements in states that offer that option, the typical next step is to register your business with the jurisdiction. Avalara Licensing can help with that.