New report from Urban-Brookings Tax Policy Center reveals how COVID-19 is affecting the fiscal health of states

The question of how the pandemic is affecting state coffers has been on a lot of minds since California issued the nation’s first stay-at-home orders on March 19, 2020. And the answer keeps changing.

Predictions were dire at first because many states experienced a “freefall” drop in revenue after businesses were forced to shutter to slow the spread of COVID-19. Pushing back income tax due dates, delaying sales tax payments, and other tax relief measures then added to budgetary woes in 2020, and for a select few states, in 2021. However, the outlook became more optimistic once federal aid arrived, income tax was submitted, and the world as we know it didn’t entirely collapse.

Where does that leave states today? Avalara asked the Urban-Brookings Tax Policy Center to find out. The resulting survey of state government officials shows an overall revenue picture that’s “not great but also not as grim as initially feared.”

The survey was sent to representatives from every state’s executive and legislative branches, and 44 states responded. Key findings from the survey include:

States think taxing online sales is beneficial but need more data (all states with a sales tax have economic nexus laws that tax remote sales)

States with progressive tax structures fared better than states heavily reliant on hospitality and leisure

Some states are looking to legalize — and tax — recreational cannabis

State budgets face uncertainty with respect to future federal policies, state revenues, consumer behavior, and more

The fact that states need more data stands out, as does the uncertainty about the future. What do states know and not know? How does that influence their tax policy decisions? I sat down with my colleague Scott Peterson, vice president of government relations at Avalara, to discuss the findings of the report.

What states know

Taxpayer data offers few insights into consumer and economic trends.

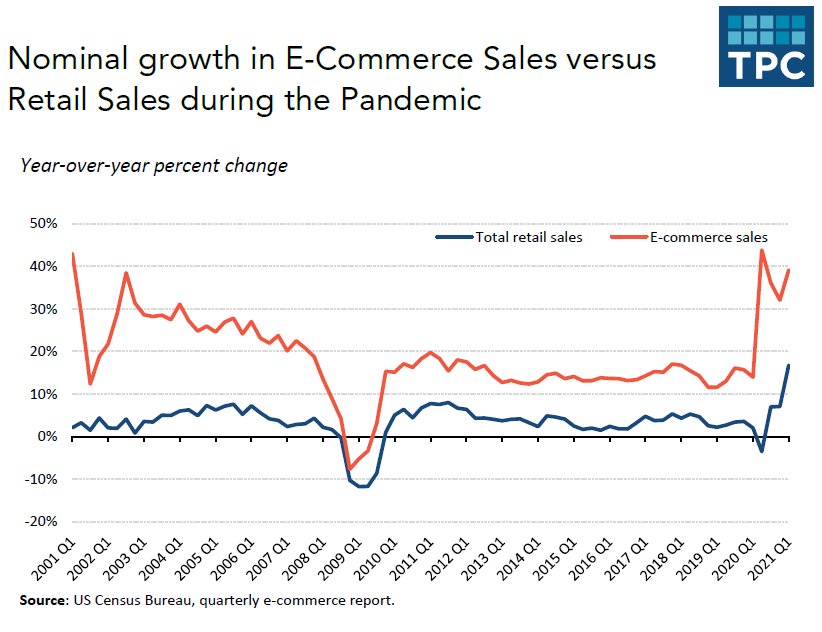

State officials know ecommerce sales skyrocketed during the darkest days of the pandemic, as in-store sales plummeted. Online sales grew nearly 44% year over year in the first three months of the first wave. During the same period, year-over-year total retail sales dropped by 3.6%.

They also understand how COVID-19 affected consumer buying habits, something Avalara has been tracking through the Avalara Commerce Monitor. When in-person activities like attending events, dining out, and in-store shopping were prohibited or restricted, consumers in many states stayed home, streamed entertainment, and bought more stuff online than usual.

But these economic trends have been widely reported. Beyond that, states usually know only what taxpayers tell them — and often that’s not a lot.

What states don’t know

States have little visibility into the genesis of sales tax revenue.

When he served as sales tax director at the South Dakota Department of Revenue (1995–2006), Scott Peterson knew “practically nothing” about the businesses collecting sales tax on behalf of the state. “The only information you get is the NAICS [North American Industry Classification System] code and what they put on their tax return, but that’s minimal in many states.”

In fact, Scott says state tax departments have painfully little data about their taxpayer base. As sales tax director, he had little to no capacity to respond to queries about who pays tax on what. “Avalara knows more about states’ taxpayers than states do because we have the product codes. Our information is head and shoulders above what any state has.”

Still, Scott was surprised by the litany of details states don’t know. This includes:

Which specific products or services are sold

State tax authorities often don’t know whether a clothing retailer specializes in children’s clothing or sportswear, or if a plumber’s repair services were to fix a leaky toilet or a blocked sink. They typically don’t need this level of detail to process returns.

Scott says states need better visibility into what items are sold in their state for a couple of reasons. “The first is so they can provide accurate revenue forecasts to legislators interested in changing taxability laws. Estimating the revenue impact of potential changes is mandatory in most states and without better data, it’s no better than an educated guess.

"The second is that it aids in their audit selection process. States spend considerable effort trying to make their audit selection process something other than random, so they can focus where noncompliance is possible and likely. Knowing how much tax is generated from a particular product would allow a state to look at everyone selling that product to see where there are unusual sales amounts.”

How sellers sell (in store or online)

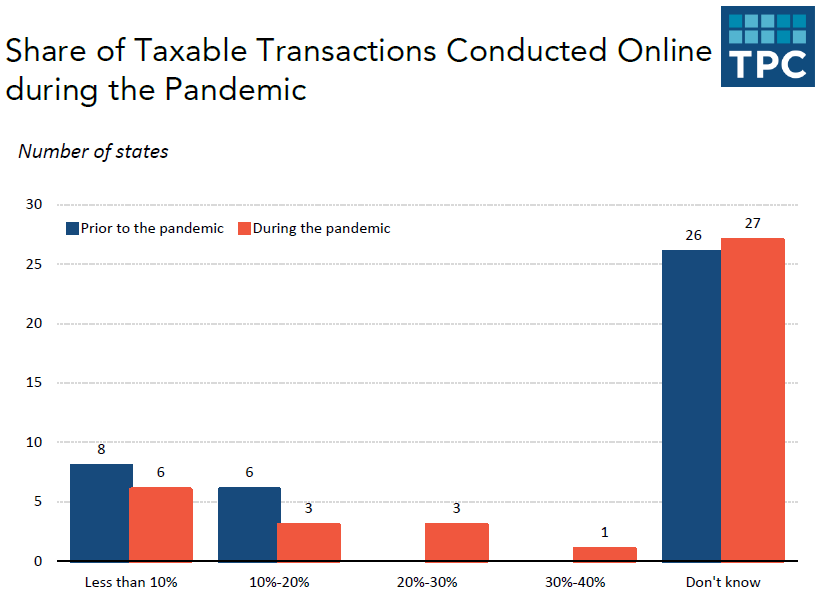

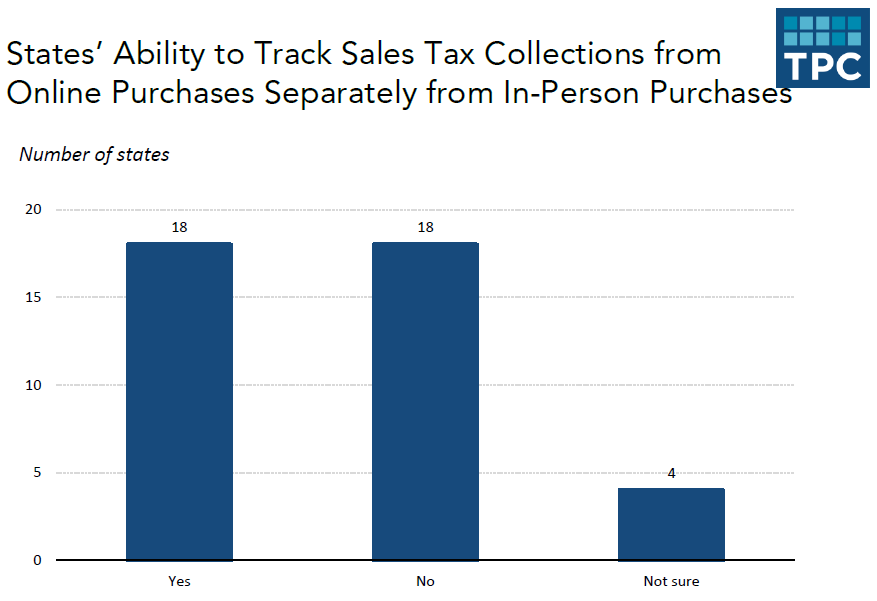

The survey showed states to have “incomplete details on online spending patterns.” Though about half the survey respondents track online sales tax revenue, many states don’t require businesses to report sales by channel and can’t easily determine what percentage of sales take place online.

This is especially true for in-state businesses, as companies with brick-and-mortar stores generally “commingle” in-store and online remittances. While it may not be necessary to get so granular to process returns if a business is taxing all sales, many respondents said it would be useful to know how many sales occur online versus in store. Maryland requires businesses to separate online sales tax remittance because the revenue is earmarked for education funding, but the state struggles to separate online transactions by in-state sellers.

Measuring online sales tax revenue from registered remote vendors may be a bit easier because there can be no in-store sales if there’s no physical store, but gaps in knowledge persist. Wisconsin tracks sales tax remittances from remote sellers and online marketplaces that registered after the Supreme Court of the United States authorized states to tax remote sales in 2018, but it doesn’t monitor collections from remote vendors registered prior to the decision.

Indeed, the survey revealed many states could not determine “the share of taxable sales transactions conducted online before and during the pandemic” due to “a lack of information.” This makes it difficult to forecast future sales tax collections and budget.

Of course, states could extract some information from the data they do have. For example, businesses with no physical address in the state likely sell online only, as do businesses registered through the Streamlined Sales Tax (SST) program. However, the less readily available the information, the less likely it will be sought and used. Scott notes that state tax authorities generally lack the resources to undertake additional projects.

Which out-of-state sellers should collect and remit sales tax

States also don’t know whether all remote sellers are registering, collecting, and remitting as they should. Scott says this jeopardizes tax compliance equity: "Tax compliance equity means everyone complies with the tax law. To acheive equity, states must know which businesses are not collecting."

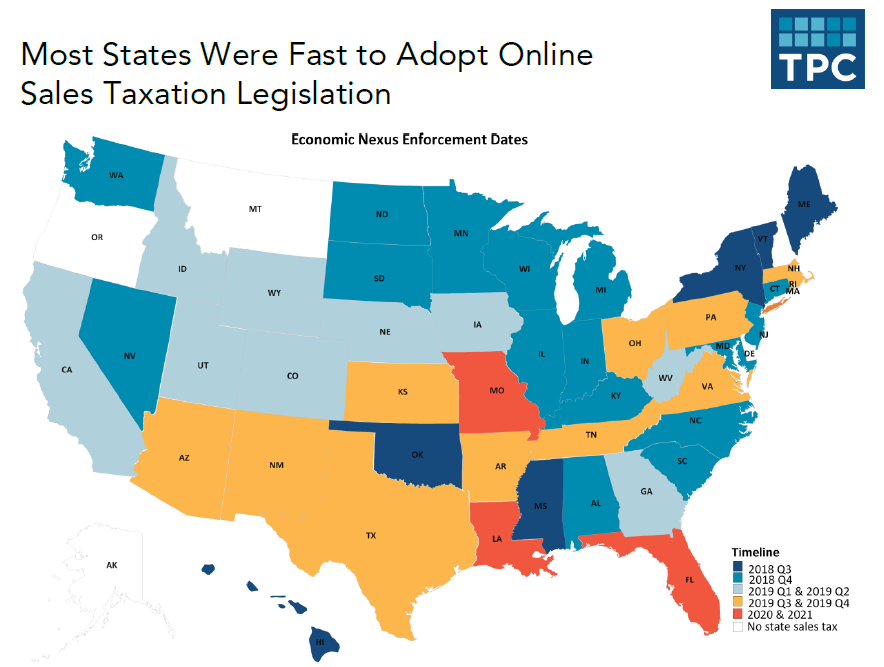

Prior to the landmark U.S. Supreme Court decision in South Dakota v. Wayfair, Inc. (June 21, 2018), states could only require businesses with a physical presence in the state to register then collect sales tax. The Wayfair ruling overturned the physical presence rule, allowing states to base nexus exclusively on a remote vendor’s sales and/or transaction volume in the state (aka, economic nexus).

All states with a general sales tax now have an economic nexus law on the books, as does the District of Columbia and some parts of Alaska. All also provide an exception for sellers with a low volume of sales or transactions in the state, though thresholds vary from state to state (e.g., $500,000 in sales, or $100,000 in sales or 200 transactions).

Unfortunately, there’s no easy way for states to gauge how many unregistered businesses should be registered. Of the more than 2 million retail businesses operating in the U.S. today, only about 14,500 sellers have registered in one or more states through the Streamlined Sales and Use Tax Agreement. Other businesses register directly with states, but there could still be thousands if not hundreds of thousands of unregistered businesses selling to American consumers.

Scott Peterson calls this America’s sales tax gap. He says there’s not a lot of criminal behavior in sales tax compliance; for the most part, sales tax evasion consists of small vendors with a lot of cash transactions using tax zappers to erase some sales. But now, economic nexus laws have created both new collection obligations and new opportunities for remote sellers to avoid them.

Technology could help fill America’s sales tax gap

It’s difficult for states to determine the scale of noncompliance, and whether a failure to register is due to ignorance or willful intent.

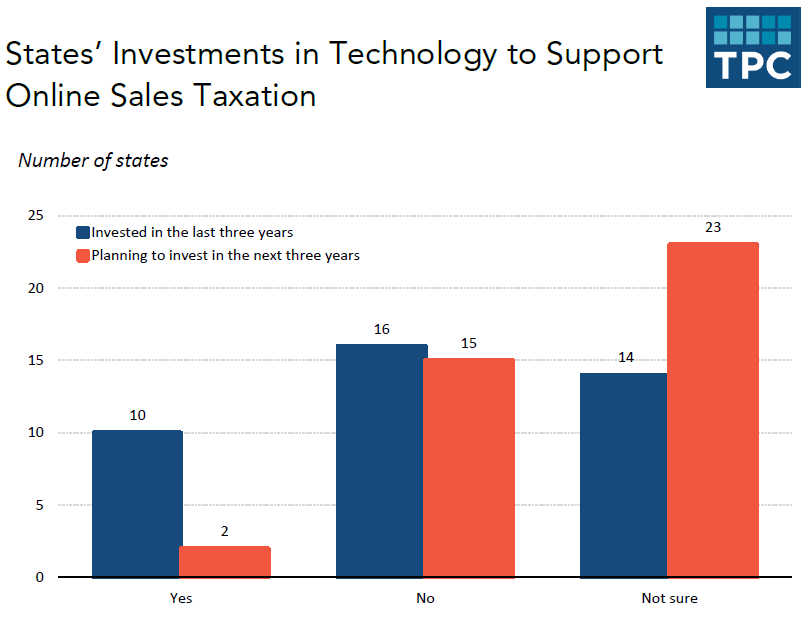

Improving technology could help states identify noncompliant remote sellers and thereby fill the tax gap. Doing so could also offer insights into future sales tax collections. Some states aren’t in a hurry to update their systems, but approximately 10 states have invested in new technology to improve remote sales tax compliance since the Wayfair decision. At least two of those states plan to make further investments in technology in the next three years, and others may do the same.

Globally, governments are leading the technology charge. Many governments outside of the U.S. now use technology to combat tax fraud and close the dreaded tax gap caused by tax evasion: Electronic invoicing requirements are becoming more and more common; real-time reporting requirements are on the rise.

The U.S. has lagged in this area, but change is afoot. For example, Massachusetts Governor Charlie Baker was recently able to institute accelerated sales tax remittance for companies of a certain size, and he’s pushing for real-time remittance.

In the meantime, states will continue to use the tools they have in hand. For example, California will keep searching for unregistered marketplace sellers that sell directly to consumers in the state. Inventory housed in a marketplace warehouse can establish nexus for marketplace sellers and an obligation to collect tax on their direct sales. Cross-referencing registered sellers with reports from marketplace facilitators is a simple way to uncover such noncompliant businesses.

There are private companies that compile lists of noncollecting businesses solely for the purpose of selling the lists to states. Scott says once a state knows a company exists, "it's very simple for them to start a formal conversation about tax compliance."

Some states use artificial intelligence and data mining tools to uncover noncompliant businesses; New York has found data mining to be particularly effective. Until states develop new technologies, they’ll continue to rely on these and other tried-and-true methods to increase sales tax compliance.

What comes next? Change driven by equity over need

States will play a long game for revenue and strive to create more equitable tax policies.

A year ago, it looked like the world would end. It didn’t. State and local governments are surprisingly flush after receiving a combined $350 billion from the American Rescue Plan Act (ARPA), with states getting $195.3 billion of the funds. Since “states have only seen revenue declines of $2 billion” according to the Tax Foundation, the state aid amounts to “116 times overall losses.”

With fuller pockets than anticipated, many state policymakers don’t need to base their decisions on immediate fiscal needs. Instead, they’ll play a long game, developing tax policies in response to technological disruptions and evolving consumer habits.

Scott thinks they’ll also reflect the zeitgeist and focus on making tax laws more equitable. Equity-based reform is driven by changes in consumer behavior and technological disruptions. Examples include taxing online sales, taxing vaping products and marijuana, and taxing digital goods and services.

Equity-based tax reform: Taxing online sales

Taxing remote sales is a perfect example of both long-term and equity-based reform. States started fighting for the right to tax businesses with no physical presence in the state decades before the birth of ecommerce, because not taxing remote sales put in-state businesses at a competitive disadvantage to out-of-state retailers making tax-free sales via catalog, mail, and phone. Ecommerce then disrupted retail and made the need to tax remote sales stronger.

The playing field for in-state and out-of-state retailers is now more level thanks to the Wayfair decision and subsequent economic nexus and marketplace facilitator laws. Yet the level playing field can be jeopardized by noncompliance: If remote sellers aren’t collecting sales tax as they should, out-of-state sellers continue to get preferential tax treatment.

So, states need to be able to identify out-of-state online sellers who should be registered but aren’t.

Equity-based tax reform: Taxing new types of sales

Equity-based reform can also drive states to broaden tax to new products and services. One way to make tax policies more fair is to make them less regressive. The Tax Foundation has long argued sales tax would be more equitable and neutral if states broadened the tax base and lowered the tax rate.

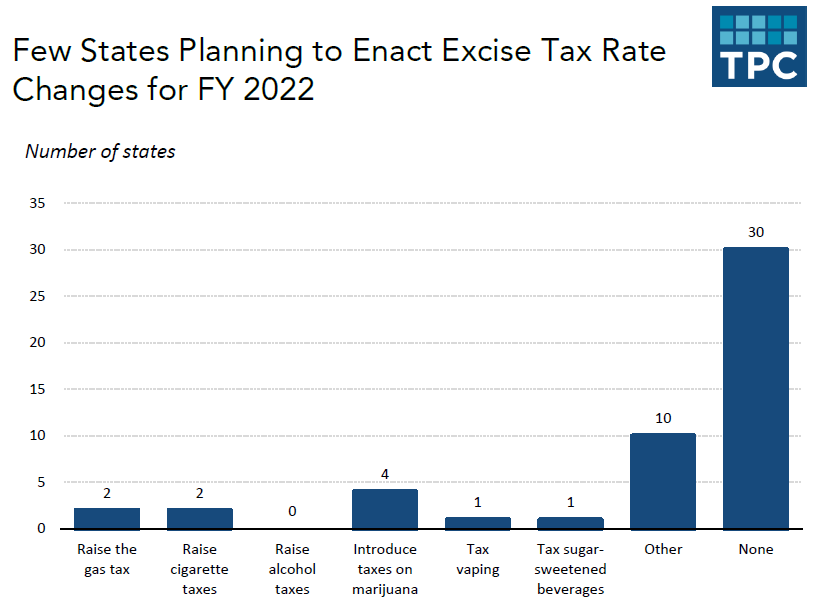

Thus, six of the states surveyed expressed an interest in legalizing — and taxing — recreational marijuana. Scott says taxing marijuana is so lucrative it may have sucked the air out of other so-called “sin” taxes, but at least one state is looking to amend its tax on sugary beverages, and some states are interested in taxing or increasing the rate on electronic cigarettes and other vaping products. At the federal level, the Prevent All Cigarette Trafficking (PACT) Act was recently expanded to include all electronic nicotine delivery systems.

Indeed, marijuana and vaping products are a perfect example of how states need to adapt their laws and tax policies to changing consumer habits. They need to ensure new types of sales are regulated and taxed so they’re not receiving preferential treatment, and so revenue streams will remain intact.

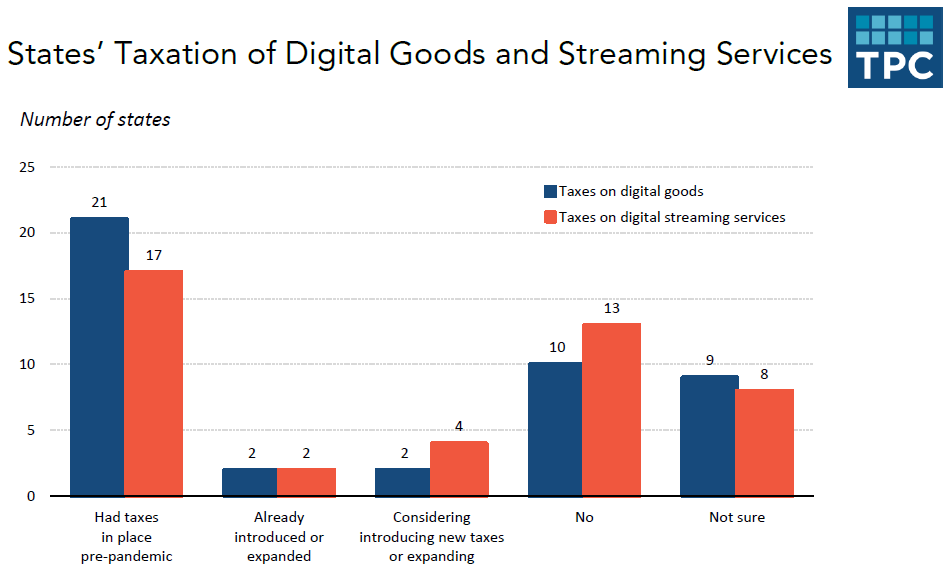

Thus, four states said they plan to tax new services, primarily digital streaming and subscription services. States that taxed these products and services benefited during the pandemic, but the report notes that “taxing the digital economy can be challenging and have unintended consequences.” One need look no further than Maryland's contentious digital advertising tax to understand why states want to further study this issue.

Another way to make tax more equitable is to ensure similar types of transactions are taxed similarly no matter who makes the sale — that industry disruptors pay the taxes the businesses they’re disrupting pay. Businesses often push for change on this front.

Scott offers the example of the nascent peer-to-peer car sharing industry. At the behest of (heavily taxed) rental car agencies, many states are working to levy taxes and fees on peer-to-peer car sharing services. Already, Florida and Nevada have decided to regulate and tax this industry, and Arkansas and Hawaii are among other states looking to do the same. Doing so will help ensure peer-to-peer car sharing companies and rental car agencies have a similar tax burden.

Online sales tax, broadening sales tax, regulating and taxing industry disruptors can help establish and maintain a level playing field.

Uncertain about what comes next, states need to regroup and reassess

The survey shows states are uncertain about the future. Scott isn’t surprised. He says states didn’t expect the Supreme Court of the United States to rule in favor of South Dakota and allow them to tax remote sales. They didn’t see the pandemic coming. They don’t know how the American Rescue Plan Act funds will impact their tax base, or exactly how they can use those funds.

And of course, no one knows what will happen with the pandemic in the coming months and years, and what impact that will have on businesses, consumers, and governments.

Delve deeper into the pandemic’s current impact on the state of the states in the report, Surveying State Leaders on the State of State Taxes.

The Avalara Tax Changes midyear update is here

Trusted by professionals, this valuable resource simplifies complex

topics with clarity and insight.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.