What global tax changes are happening in 2024?

The unrelenting growth of ecommerce — and technology that can help facilitate it — puts buyers and sellers all over the world within reach of each other. Borders, oceans, and airspace that separate them are effectively eliminated at the browsing and buying stage.

An enormous amount of goods still have to get from point A to point B, and are constantly moving across borders via land, sea, and air. Cross-border compliance challenges therefore remain, as do physical borders where customs checks are conducted by humans (for now).

Technology continues to be adopted and utilized by businesses and authorities alike to help them ensure borders aren’t barriers. Global tax authorities are ramping up their efforts to go digital (or at least outlining strong intentions to do so) and embrace technology, perhaps as much as businesses and customers, to make international trade easier. By digitalizing tax compliance and administration, governments can also save on costs, reduce tax fraud, increase their efficiency, move closer to global standardization, and enhance their data analytics and insight capabilities. Requiring use of e-invoicing and live reporting allows governments and authorities to achieve all of those goals.

With the growing number of government mandates, and its increasing popularity among businesses, e-invoicing is central to the future of tax compliance. Governments welcome the opportunity e-invoicing and live reporting provides in gaining granular and more accurate views into transactional data in real time.

Many governments are also implementing digital hubs and systems that simplify and expedite cross-border trade without compromising national and international security — a critical factor given the current geopolitical climate. The European Union’s (EU) customs data hub allows businesses to disentangle the administrative side of importing goods. This enables the EU to accommodate faster customs clearance without having to cut back on safety and security checks and resources.

This shift (or acceleration) into the digitalization of tax compliance suggests global governments and tax authorities are no longer simply trying to keep up with businesses’ use of technology. Having a sound understanding of the essential role technology plays in international trade and compliance, governments are now setting the pace themselves instead of belatedly reacting to developments in technology and how global business is conducted.

Whether located in or outside the U.S., businesses that already do or plan to trade internationally need to understand how technology and international tax compliance are driving each other to evolve, and how the right software can help them adapt to and comply with new rules and requirements.

What the numbers tell us about the global tax economy

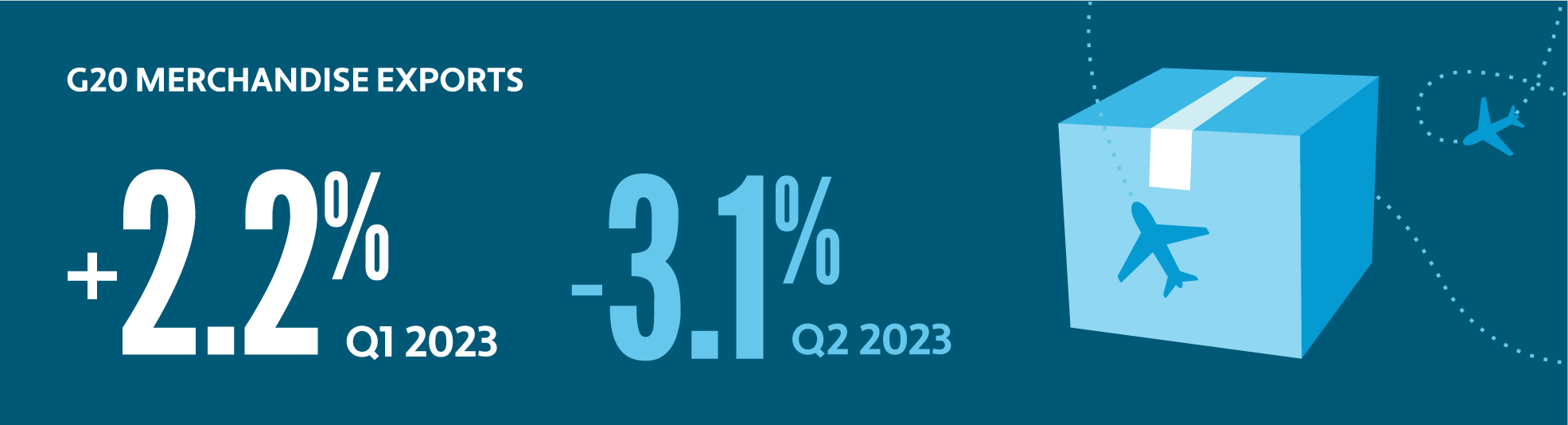

SOURCE: OECD

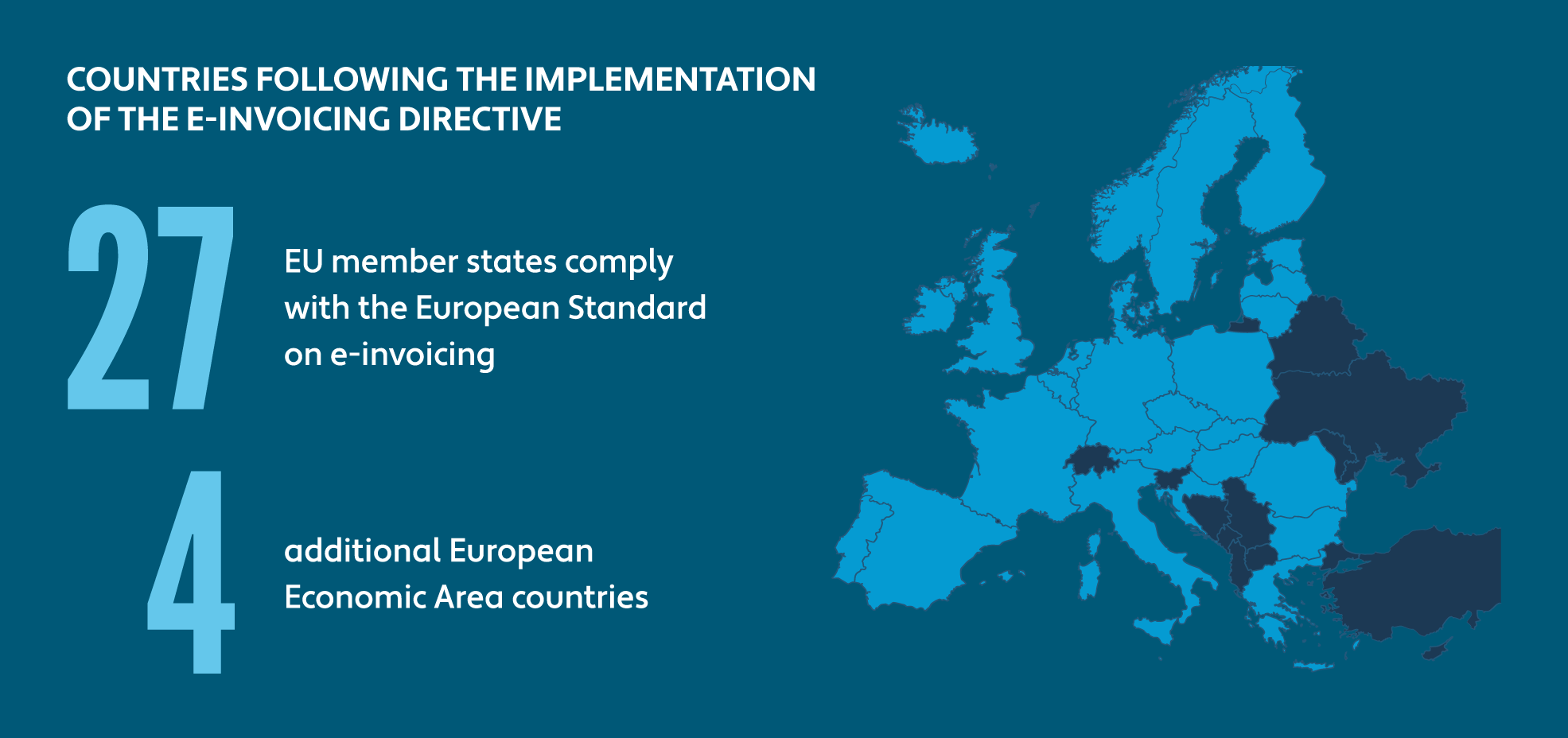

SOURCE: European Commission

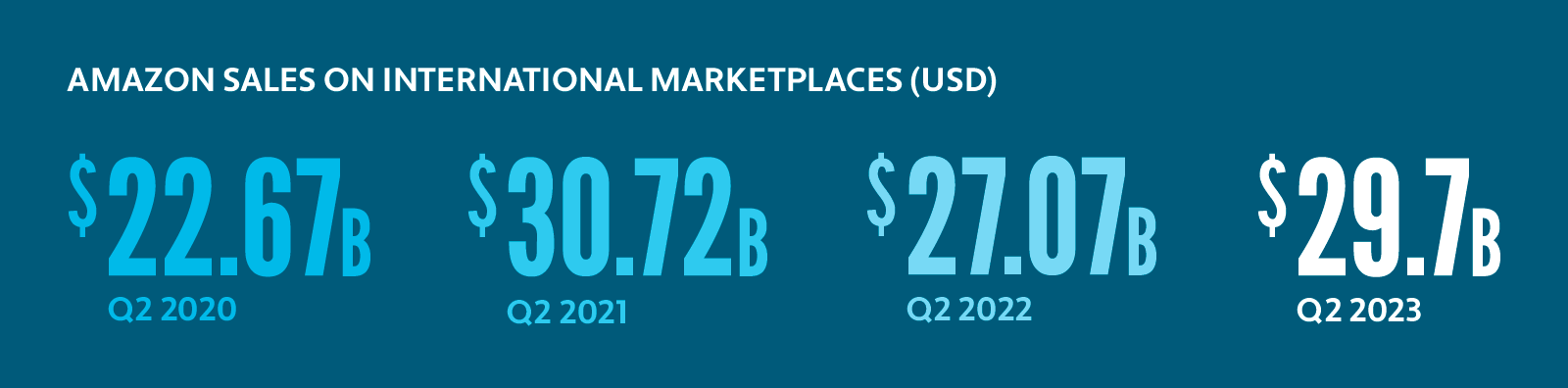

SOURCE: Marketplace Pulse

SOURCE: Insider Intelligence

SOURCE: Avalara

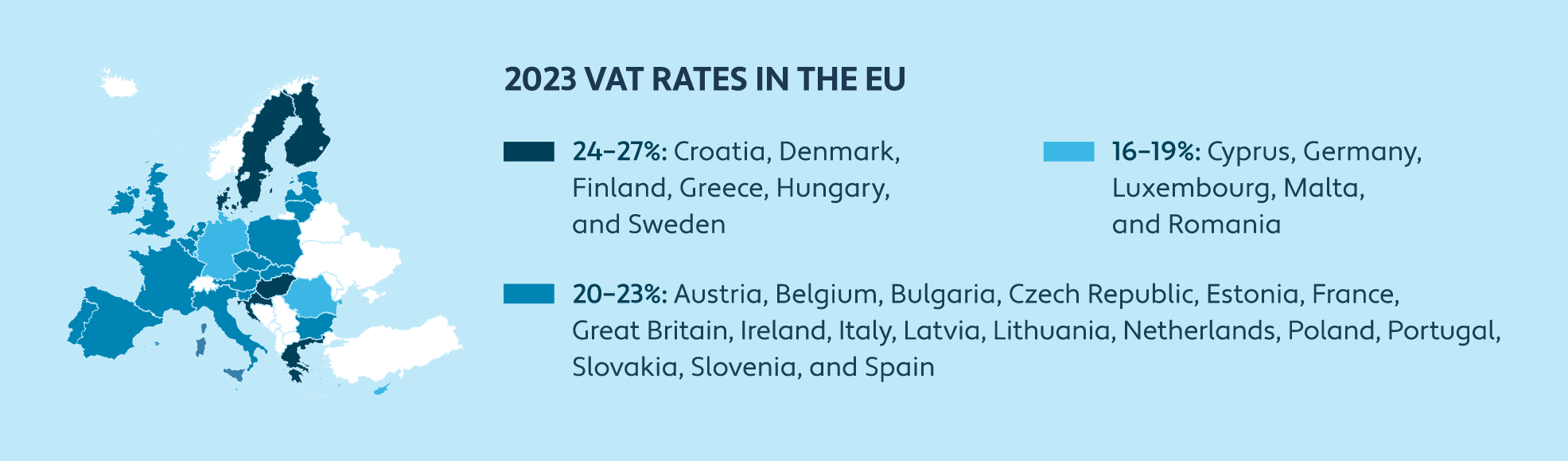

Recent changes to VAT in the Digital Age

As a response to the growing digital economy — and existing VAT systems’ struggles to keep up with the huge amount of online transactions — the European Commission published a proposal for VAT in the Digital Age (ViDA) in December 2022 — a plan to modernize VAT within the EU. The European Commission recognizes that digitalization can create opportunities to increase compliance, reduce the VAT gap, and simplify tax compliance and reporting for businesses. This major policy initiative focuses on three topics related to VAT, digitalization, and new innovative business models.

SOURCE: Tax Foundation

ViDA is designed to level the tax playing field for all businesses operating within the EU. Changes that go into effect will impact e-invoicing, ecommerce sellers, and the platform economy. ViDA also aims to close the VAT gap — the estimated difference between expected VAT revenue and actual VAT revenue collected. (More on closing this gap later.)

Under ViDA, it will be easier for EU member states to mandate e-invoicing owing to the removal of legal hurdles to mandate requirements. Existing EU VAT directives that place restrictions on EU member states whereby they must seek approval from the European Commission before mandating e-invoicing, and permission from customers before replacing paper or PDF invoices with e-invoicing, will be reformed.

ViDA will also extend VAT obligations for marketplaces and ecommerce platforms by making them liable for charging and remitting VAT when they facilitate business-to-business (B2B) and business-to-consumer (B2C) sales of goods within the EU. This will apply to domestic and cross-border sales, regardless of where the seller is based, and will simplify VAT obligations for buyers at the same time.

Also, short-term rental providers such as Airbnb and passenger transport service companies like Uber will be deemed suppliers, meaning they’ll also be responsible for collecting and paying VAT for their third-party sellers or customers. This aims to bring VAT obligations for these types of businesses in line with those of more traditional service providers.

E-invoicing is becoming a global standard

E-invoicing is the process of creating and providing an electronic invoice in the form of structured data — instead of a more traditional paper version or a PDF sent by email — to digitally exchange invoice data between a supplier and a buyer. An e-invoice allows the recipient to automatically process incoming invoices and post the invoice data into their accounting or ERP system with minimum human involvement.

E-invoicing is rapidly becoming more and more prevalent around the world. The benefits to governments and businesses are mutual. It’s the preferred method of collecting tax information by governments in an increasing number of countries. E-invoicing enables them to better tackle tax fraud, reduce the VAT gap, gain greater transparency on transactions — and therefore more insight into business and trade data — and encourages digital transformation, in line with many countries’ current goals. For businesses of all types and industries, it allows for streamlined finance departments and an opportunity to revamp and update financial and accounting systems, save on time and costs, and reduce their carbon footprint by cutting back on paper usage. According to a 2019 Billentis report, automated e-invoicing offers cost savings of 60–80% in most cases.

Although the electronic exchange of invoice data has been practiced by businesses for decades (predating the internet), government mandates first started to appear in Latin America in the early 2000s. It wasn’t until 2019 that mandates began rolling out in Europe. More than 60 countries currently have e-invoicing legislation in place, and the scope and details of requirements for e-invoicing and live reporting vary according to economic factors and transaction types.

E-invoicing mandates and live reporting requirements are constantly being introduced, amended, and updated in all global regions, making it a huge challenge for businesses and even compliance experts to stay completely up to date on the latest information and developments.

“E-invoicing is the clear direction of travel. It’s important to remember that countries that don’t have mandatory e-invoicing requirements now will have them in the future,” says Alex Baulf, Senior Director of E-invoicing at Avalara. “And it’s only the tip of the iceberg. Governments worldwide are experiencing huge benefits by mandating e-invoicing, and with new technologies and requirements being implemented every day, it’s highly unlikely digital compliance developments will stop there. For businesses that want to stay ahead of the curve, it’s crucial to invest in a scalable global solution that not only works today but can handle the requirements of the future.”

What countries have new e-invoicing mandates?

France had been moving toward a July 1, 2024, launch date for e-invoicing mandates; however, the French government recently postponed the launch due to concerns around the readiness and ability of smaller businesses to adapt to such significant compliance changes. It also wants to safeguard against risks associated with a centralized system, such as that used by the Italian Revenue Agency, the Sistema di Interscambio.

The French government is considering the risk and likelihood of all e-invoicing effectively coming to a halt in the event of a cyberattack, which could cause major disruption to business and the economy. E-invoicing in France will be implemented in stages, with the first wave of businesses being mandated to issue e-invoices starting September 2026.

Other recent updates include:

- In Belgium, e-invoicing for B2B transactions is not currently mandatory, but proposals have recently been approved to introduce mandatory e-invoicing for domestic B2B transactions commencing January 1, 2026.

- B2B e-invoicing is not currently mandatory in Croatia, but the country has proposed a date of January 1, 2026, for a mandate covering both B2B and business-to-government (B2G) transactions.

- Mandatory B2B e-invoicing in Germany is planned and currently projected for 2026.

- Israel has plans to introduce mandatory e-invoicing for invoices subject to VAT where the taxable base exceeds ILS 25,000, starting April 2024.

- E-invoicing is mandatory in Japan for certain transactions such as those between companies and government agencies, as well as for transactions between businesses in certain industries. Japan has also recently adopted the use of Peppol (see below for more information) and launched the U.K.-Japan Digital Partnership to strengthen digital cooperation between the two countries.

- Poland’s e-invoicing mandate is now confirmed to come into force in July 2024.

- Romania has an e-invoicing mandate for B2G and certain B2B transactions (for goods listed as “high fiscal risk”) in place today. It will also introduce a general B2B e-reporting mandate beginning January 2024 and a wider e-invoicing mandate beginning July 2024.

- E-invoicing is mandatory in Spain for B2G transactions and is expected to become mandatory for B2B transactions as of July 2024. With recent public consultation and elections, this date will probably be postponed by 6–12 months.

The Peppol network (formally known as Pan-European Public Procurement Online) was originally developed to streamline business with customers within the public sector of the EU. It also became popular for document exchange among private companies. As Peppol is adopted by more and more countries around the world, it has become the most common delivery network and standard for trading partners (including governments) to send and exchange compliant e-invoices. Currently, more than 30 countries have implemented or are in the process of implementing the Peppol framework. Though most are located in Europe — including the U.K., Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Norway, Poland, Portugal, and the Netherlands — Peppol has also been adopted in Australia, Japan, New Zealand, and Singapore.

Will e-invoicing come to the U.S.?

The U.S. currently has no e-invoicing mandates or live reporting requirements. However, a pilot for voluntary adoption was carried out in 2022 by the Business Payments Coalition — led by the Federal Reserve Bank of Minneapolis. The E-invoice Exchange Market Pilot aimed to design, build, and test a virtual network that will enable U.S. businesses to exchange e-invoices and establish a secure, open e-invoice delivery framework between service providers.

The Digital Business Networks Alliance was established in 2023 to oversee the creation and operation of a new B2B digital highway to allow businesses across the U.S., Canada, and Mexico to exchange e-invoices. U.S. businesses that wish to continue operating in or enter into international markets where e-invoicing mandates are in place (or planned) will have to comply with local regulations. U.S. businesses should strongly consider familiarizing themselves with e-invoicing software that can help them do so.

IOSS opens up to more businesses

The Import One-Stop Shop (IOSS) scheme was introduced by the EU in July 2021. The scheme makes it easier for businesses to sell into the EU by allowing them to register in a single member state to declare and pay EU import VAT on sales made to EU consumers for a goods shipment with a consignment value below €150. Businesses that use the scheme receive a unique IOSS identification number to put on all packages sent to the EU. Having assessed that the €150 threshold creates a burden to businesses, the EU proposed on May 17, 2023, to remove it, opening IOSS to more businesses that would benefit from lower compliance costs.

As part of ViDA proposals, IOSS will become mandatory for marketplaces facilitating low-value imports into the EU.

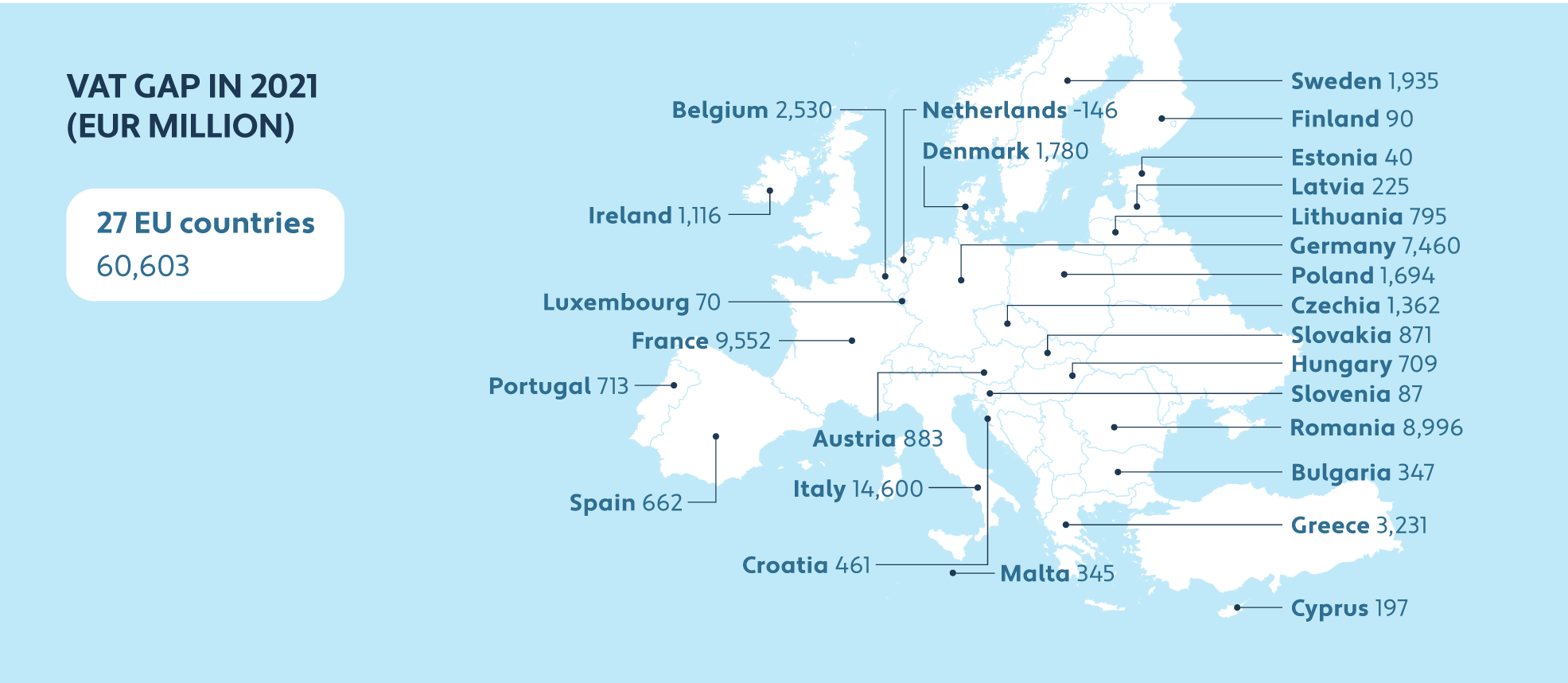

Closing the VAT gap

The VAT gap is the estimated difference between expected VAT revenue and actual VAT revenue collected. It’s a calculation of lost tax revenue that could have been collected if all businesses were fully compliant with VAT regulations. The European Commission recently reported that EU countries lost around €61 billion in VAT in 2021, down from €99 billion in 2020.

SOURCE: Taxation and Customs Union

Businesses are expected to collect VAT on behalf of the government and remit it to tax authorities, but not all businesses fully comply. There are various reasons for this, from criminality such as tax fraud and tax evasion, to genuine mistakes, bankruptcies, financial insolvencies, and miscalculations and administrative errors.

The ongoing rollout and adoption of real-time reporting provides authorities with more transparency into transactional data, making it easier to clamp down on VAT fraud and evasion. By having access to vast amounts of tax data in real time, and by deploying sophisticated algorithms including artificial intelligence, tax authorities can spot unusual patterns or anomalies almost immediately, quickening their response to suspect and fraudulent activity. The understanding that transactional data is available to authorities in real time can also act as a deterrent to more evasively minded businesses, and those that “forget” to remit what’s owed.

Reducing the VAT gap means governments can increase their tax revenue without raising tax rates. This can help to fund public services, healthcare, education, infrastructure, and social welfare programs.

What are the new EU customs reforms?

The European Commission believes EU customs reforms announced in 2023 represent “a smarter approach to customs checks” and “a more modern approach to ecommerce.” As part of the reforms, in March 2028, marketplaces and ecommerce platforms will become “deemed importers.” This means platforms will be responsible for ensuring VAT and customs duties — which become due when the platform receives the payment for the goods — are paid at the point of sale and removes the burden from consumers.

While VAT is applicable on all imported goods into the EU, parcels valued up to €150 are currently exempt from customs duties. This exemption will be removed March 1, 2028.

A new EU customs data hub will allow businesses that bring goods into the EU to log all information on their products and supply chains into a centralized system. Businesses will only need to submit data once for multiple consignments, instead of a declaration for each specific parcel, allowing for simplified and more rapid customs clearance. The hub will also provide relevant authorities with a 360-degree overview of supply chains and the movement of goods within the EU, as an update to risk management measures and customs checks.

The governments of EU member states will have more far-reaching access to data, and in real time. Information can also be shared among members, allowing for quicker and more unified responses to any perceived security risks. Artificial intelligence can even be used to monitor the data and predict risk before goods reach the EU, allowing EU customs authorities to channel their resources accordingly.

The reforms also include simplified tariff classifications and customs calculations to determine the customs owed for items most commonly brought into the EU via B2C sales. Though the simplified tariff treatment will be applied on a voluntary basis by importers, they’ll benefit from preferential tariff rates by doing so.

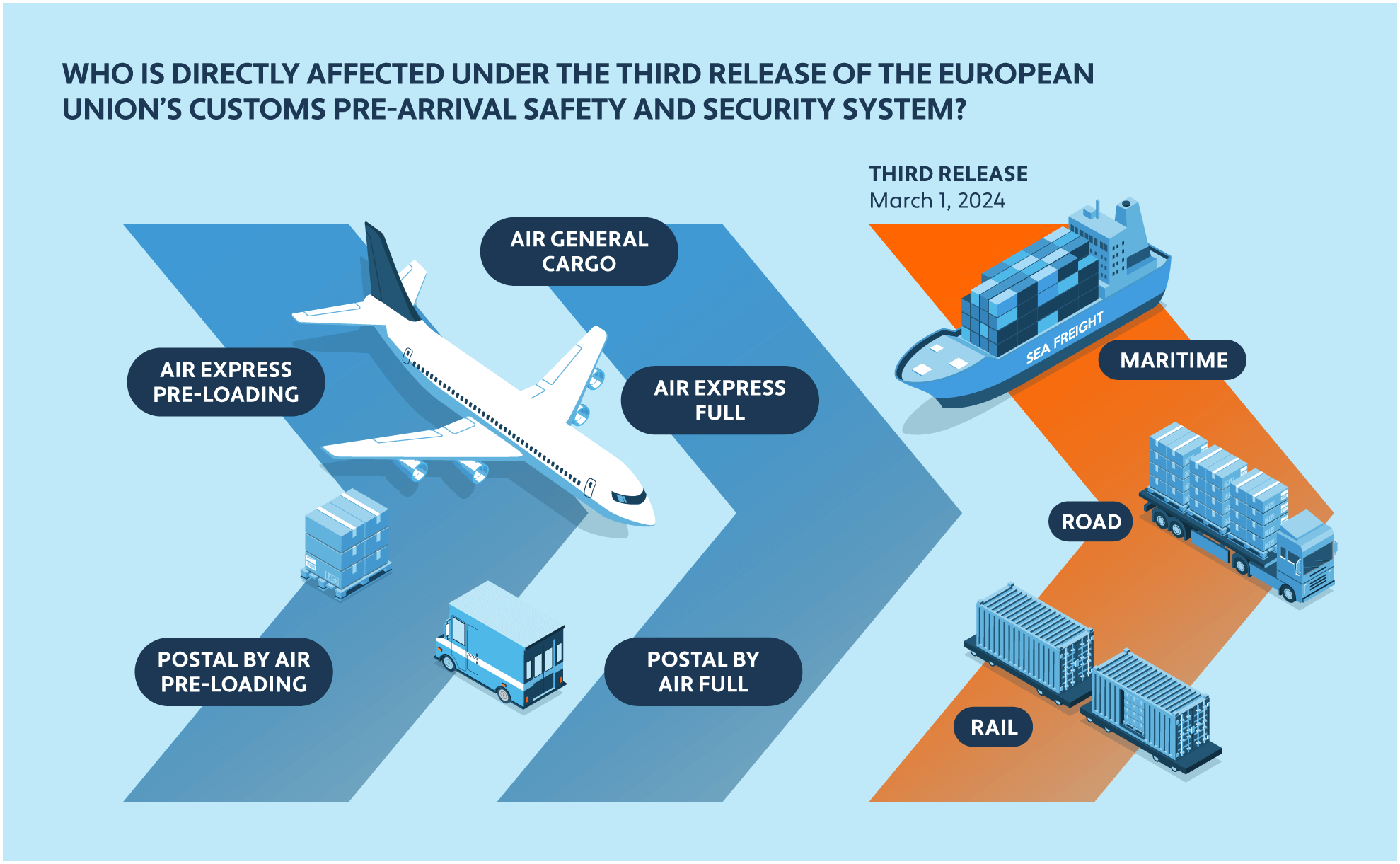

Import Control System 2 Release 3

The third and final phase of Import Control System 2 (ICS2) will begin on March 1, 2024. ICS2 is another EU safety and security initiative that screens shipments prior to their arrival in Europe. The initiative is designed to help protect against security and safety threats by helping customs authorities identify high-risk consignments and intervene where necessary.

SOURCE: European Commission

ICS2 phases 1 and 2 commenced March 2021 and March 2023 respectively, affecting all carriers, couriers, and postal services transporting goods through the EU by air. From these dates, it became a requirement to submit safety and security information to the EU prior to a shipment’s arrival. Without this data, goods will be stopped at customs.

Phase 3 will impose these rules on operators moving goods by maritime and inland waterways, road, and rail. All operators must submit Entry Summary Declaration (ENS) data to ICS2 prior to the arrival of goods in the EU to meet data filing obligations.

Free trade agreements are a boost to digital trade

The Australia-United Kingdom Free Trade Agreement entered into force on May 31, 2023, with aims of creating new export opportunities for businesses in both nations, reducing costs for businesses, easing cost-of-living pressures for consumers, and increasing transparency for customs procedures.

The agreement removes tariffs on most exports between Australia and the U.K., which the U.K. government estimates will increase U.K. GDP by £2.3 billion per year by 2035. Though this increase is relatively small, the government also expects the agreement “to unlock £10.4 billion of additional trade, boosting our economy and increasing wages across the U.K.” It also cites as expected benefits: access to the Australian market for British services and investors, more opportunities for U.K. businesses to trade digitally with Australia, and lower prices for U.K. consumers and businesses.

Though multiple economic sectors are expected to see an increase in output, the agreement specifically commits to an increase in opportunities for digital trade and supports a more secure online environment for businesses in the digital economy. Governments of both nations want to enable cross-border data flows — without jeopardizing the data privacy of consumers — and facilitate the acceptance of electronic versions of trade administration documents to reduce barriers to trade. Further, the two nations are expecting ongoing cooperation on digital trade issues such as data innovation, the development and adoption of digital standards, and how emerging technologies can benefit businesses and consumers in Australia and the U.K.

The U.K. free trade agreement with New Zealand (originally signed in February 2022 and entering into force May 31, 2023) also aims to reduce barriers to trade between the U.K. and New Zealand. Like the Australia-U.K. agreement, it removes tariffs on U.K.-New Zealand trade (U.K. tariffs on some sensitive agricultural products are reduced over a transitional period). New Zealand exporters could save approximately NZD 37 million per year on the elimination of tariffs.

Sustainability issues in 2024

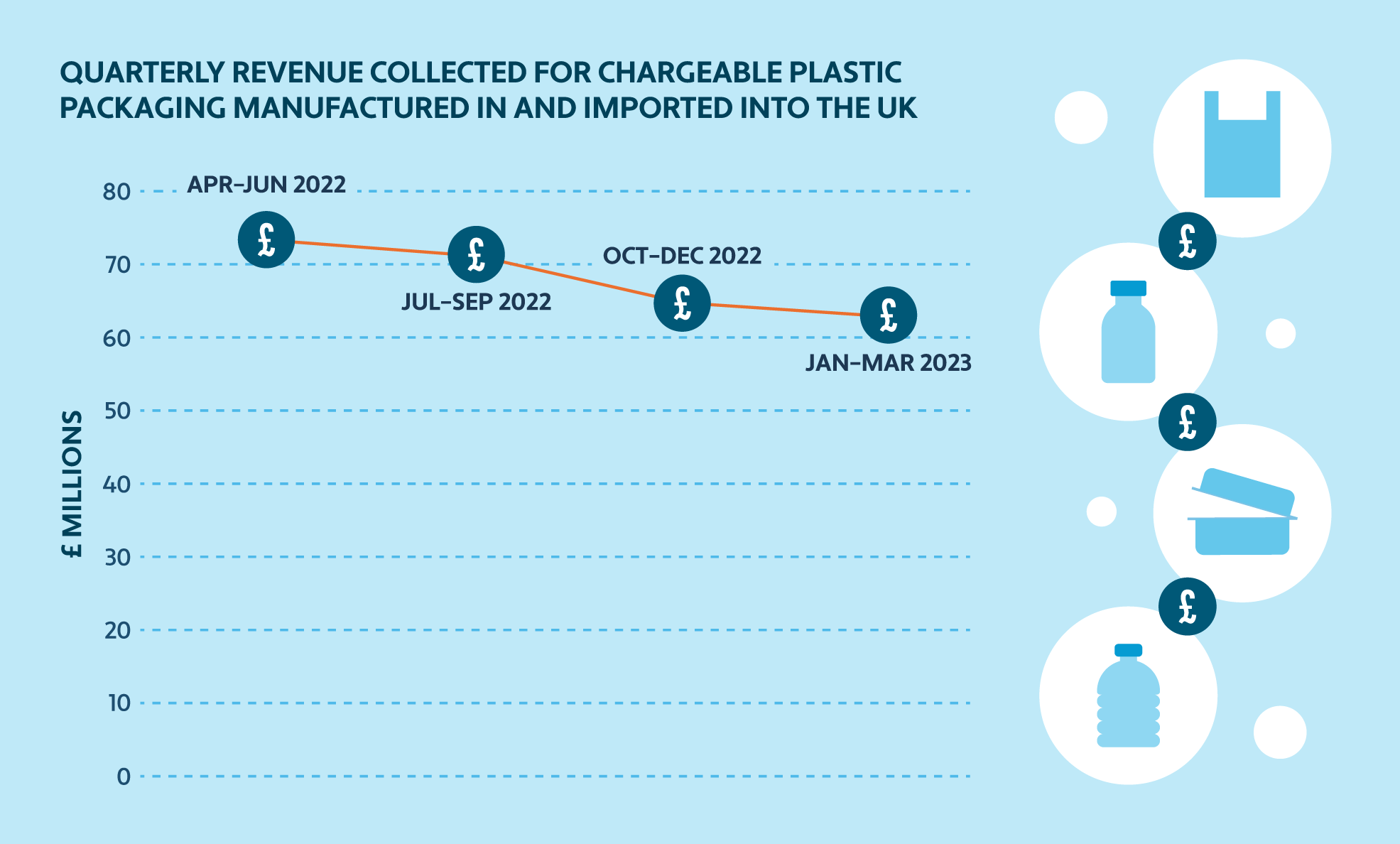

Climate issues are becoming a higher priority for nations around the world. The Plastic Packaging Tax (PPT) on plastic packaging with less than 30% recycled plastic came into effect in the U.K. on April 1, 2022, with a charged rate of £200 per tonne, generating £276 million of revenue in the first year. The rate rose on April 1, 2023, to £210.82 per tonne. PPT is designed to encourage the use of more recycled plastic and reduce single-use plastics, and applies to plastic packaging produced in, or imported into, the U.K. The U.K. government estimates the tax affects approximately 20,000 packaging producers and importers.

SOURCE: GOV.UK

Businesses must submit quarterly returns to HM Revenue & Customs (HMRC) detailing weights of plastic packaging. Smaller businesses that import or manufacture less than 10 tonnes of plastic packaging per year are exempt from PPT. Once a business meets the 10 tonnes threshold, it must register with HMRC for PPT. The tax is self-assessed and businesses are responsible for ensuring they’re compliant with the regulations.

Although HMRC hasn’t announced any further PPT rate increases for 2024 or later, similar taxes targeting a wider range of materials would come as little surprise in the U.K. and beyond.

Australia — one of the world’s biggest fossil fuel exporters — passed climate laws on July 1, 2023, requiring total emissions from big industrial sites to be cut by 5% per year, either through absolute cuts or by buying carbon offsets. The Australian government has announced a review on whether to introduce a carbon border adjustment mechanism (CBAM) in the country — essentially, a “carbon tariff” to certain imports from overseas. The feasibility of introducing such measures is set to be determined in October 2024.

Australia has seemingly taken lessons from the EU CBAM, which imposes a levy on industries with significant emissions and aims to ensure the carbon content of imported goods is equivalent to those produced within the EU. The EU uses software and algorithms to analyze data on the raw materials and production and transportation process to calculate imported products’ carbon footprint. CBAM data can also be integrated into customs systems for the purpose of customs checks upon import. The EU can therefore use technology to monitor the effectiveness of its CBAM. Though CBAMs are considered within some industries to be a trade barrier, Australia looks set to move ahead with a similar system that does not negatively impact trading relationships.

How Avalara can help

Tax automation helps global businesses of all types maintain compliance with international tax requirements while saving time, lowering costs, and growing revenue. Learn more about Avalara solutions for e-invoicing and live reporting, VAT reporting, tariff code classification, and more.