Massachusetts enacts economic nexus, marketplace facilitator law

Update 7.31.2019: The economic nexus and marketplace facilitator provisions in H.4000 have been signed into law. They take effect October 1, 2019.

Massachusetts lawmakers have sent the 2020 budget to Governor Charlie Baker at last — three weeks after the start of the 2019–2020 fiscal year. It includes remote sales tax provisions the governor championed when introducing his budget proposal: sales tax collection requirements for remote sellers and marketplace facilitators.

Cookie nexus vs. economic nexus

Massachusetts already requires certain remote internet vendors to collect sales tax under a 2017 regulation adopted when states were limited to taxing sales by businesses with a physical presence in the state. To work around the physical presence rule, Regulation 830 CMR 64H.1.7 holds that internet vendors establish a physical presence in Massachusetts when they place software on in-state devices. This is sometimes called cookie nexus* after web cookies.

Less than a year after cookie nexus took effect in Massachusetts, the Supreme Court of the United States overruled the physical presence rule with its decision in South Dakota v. Wayfair, Inc. (June 21, 2018). States now have the authority to require out-of-state sellers with a certain amount of sales and/or transactions in the state (economic nexus) to collect and remit sales tax.

The Massachusetts Department of Revenue has said the Wayfair decision doesn’t affect enforcement of its cookie nexus regulation, and the new budget doesn’t repeal the cookie nexus regulation. In fact, it includes in the definition of “engaged in business in the commonwealth” exploiting the retail sales market through a retailer’s use of “an Internet website, software or cookies distributed or otherwise placed on customers’ computers or other communications devices, or a downloaded application.”

However, the budget also includes a new South Dakota-style economic nexus provision. Under H.4000, a remote seller is required to register with the department and collect and remit Massachusetts sales tax if its sales into the commonwealth in the current or prior taxable year exceed $100,000. This threshold is considerably lower than the existing cookie nexus threshold (more than $500,000 in sales and at least 100 transactions).

Learn about economic nexus laws in other states in Avalara’s state-by-state guide to economic nexus laws.

Avalara Free Tax Guides

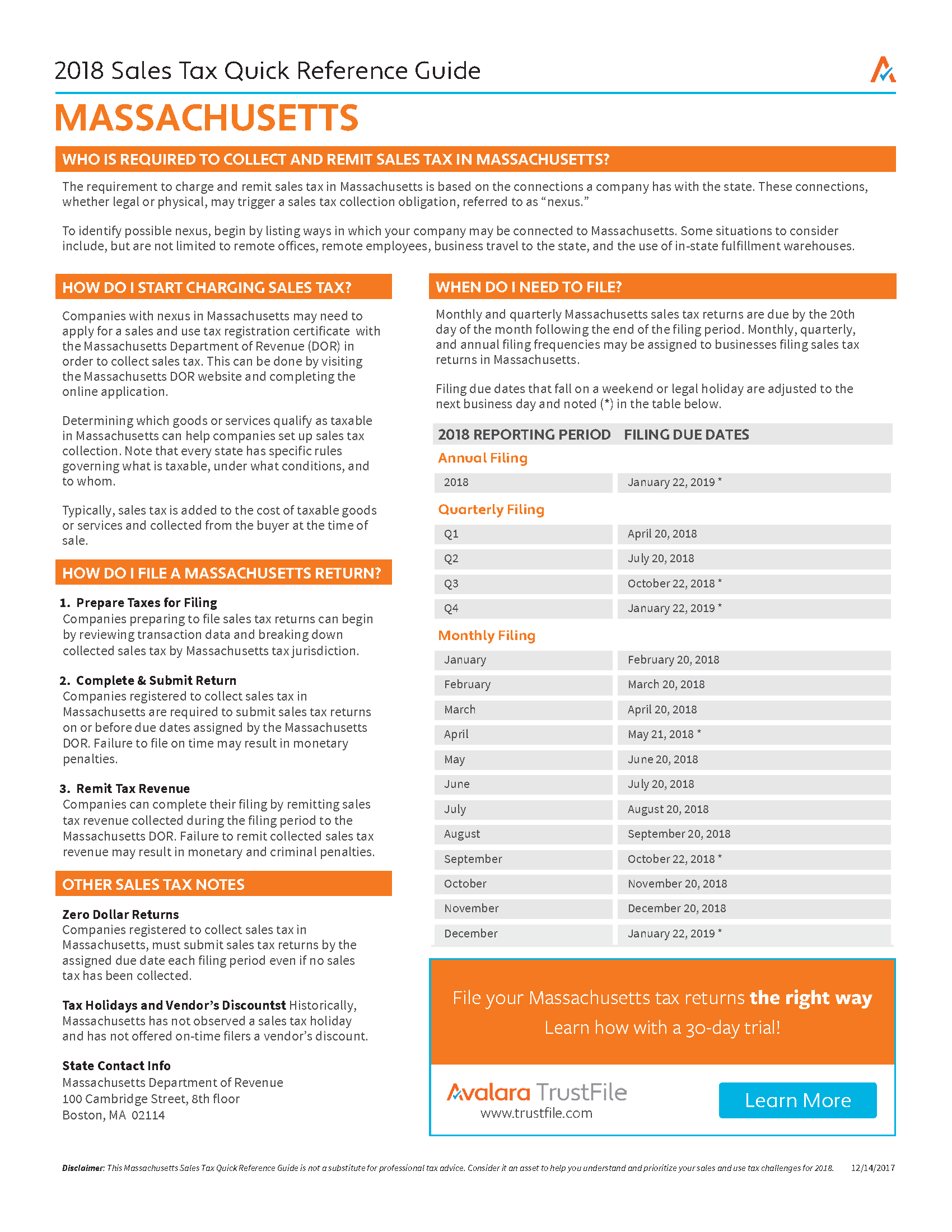

Massachusetts Sales Tax Reference Sheet

A handy reference for businesses filing Massachusetts sales tax returns.

New sales tax collection requirement for marketplace facilitators

In addition to establishing economic nexus for remote sellers, H.4000 would require certain marketplace facilitators to collect and remit the tax due on all sales made through the marketplace. More than 35 states, and counting, have similar policies.

H.4000 defines “marketplace” as “a physical or electronic forum, including a shop, a store, a booth, a television or radio broadcast, an Internet web site, a catalogue or a dedicated sales software application, where the tangible personal property or services of a marketplace seller is offered for sale, regardless of whether, in the case of tangible personal property, such property is physically located in the commonwealth.”

The sales tax collection requirement would apply to in-state and remote marketplace facilitators whose sales within the commonwealth in the prior or current taxable year meet the economic nexus threshold (more than $100,000). The threshold count includes all sales made or facilitated through the marketplace, direct sales, and those made on behalf of third-party sellers.

Neither in-state nor out-of-state marketplaces are responsible for collecting tax on third-party sales if their sales into Massachusetts don’t meet the $100,000 threshold.

When calculating the threshold, remote sellers shouldn’t count sales made through a marketplace if the marketplace facilitator reports, collects, and remits sales tax on behalf of the seller. The Department of Revenue will issue additional guidance for in-state and out-of-state sellers, marketplace sellers, and marketplace facilitators.

Alternatives

The budget contains a provision allowing marketplace facilitators to request a waiver from the requirement to collect tax for a marketplace seller. The facilitator must presume in good faith that the seller will collect and remit the tax due. Furthermore, the facilitator must obtain and maintain a record of the applicable tax registration numbers for any such sellers. If the Massachusetts Department of Revenue approves the waiver, the marketplace seller will be liable for the tax owed.

A marketplace seller of telecommunications services would also be permitted to request a waiver that would allow it to collect and remit applicable sales taxes itself. Given the breadth and complexity of the services they provide, telecommunications companies such as AT&T tend to want to maintain control over sales tax collection and remittance. Ohio’s newly enacted marketplace facilitator law contains a similar allowance.

The sales tax collection requirement for marketplaces would take effect in Massachusetts on October 1, 2019. Gov. Baker has 10 days to approve, veto, or partially veto the fiscal year 2020 budget.

Learn more about the various ways states can require remote sellers to collect and remit sales tax in the seller’s guide to nexus laws and sales tax collection requirements.

*Ohio has a similar rule, though it’s repealed effective August 1, 2019.

The Avalara Tax Changes midyear update is here

Trusted by professionals, this valuable resource simplifies complex

topics with clarity and insight.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.