Know your nexus

Determining where and when you need to collect and remit sales tax

Getting sales tax compliance right is important. The first step is understanding where your business has nexus, or where you need to collect and remit sales and use tax. Nexus is ever-changing and it can be confusing for even savvy professionals. Fortunately, AI and automation make it easier to identify where you have nexus and to meet your obligations.

Once your business has nexus with a state or local jurisdiction such as a county or city, you must adhere to that taxing authority’s rules including collecting and remitting sales tax and managing use tax obligations. Use tax responsibilities come into play when taxable products or services are purchased without sales tax. The buyer must pay use tax to the jurisdiction where the item is used or stored. Read our 5 steps to managing sales tax guide to better understand your sales and use tax obligations and how to stay compliant.

Unfortunately, you can’t just figure out where you have nexus today and forget about it — you have to closely monitor changes to nexus. Many activities can trigger new tax collection obligations for your business, especially now that every state with a sales tax has passed laws targeting remote sales and use tax revenue and online marketplace sales.

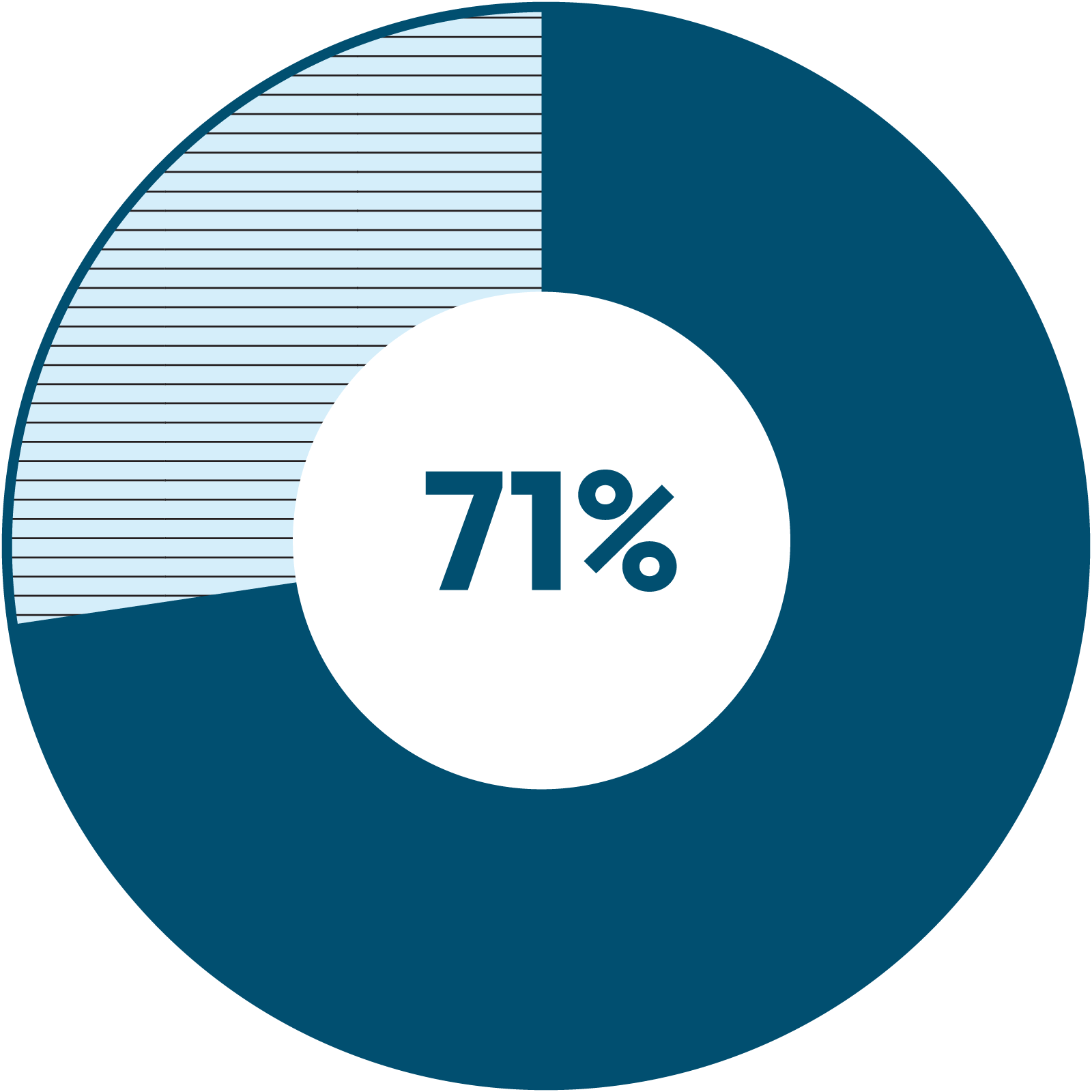

It’s been a while since the 2018 U.S. Supreme Court decision, South Dakota v. Wayfair, Inc., changed tax obligations for remote sellers. Many companies still have a lot to understand about nexus and how it’s established from state to state. According to a 2023 survey by Censuswide, about 55% of respondents can explain all their online sales tax obligations to someone outside their organization. More than 71% of respondents agree or strongly agree that online sales tax requirements including economic nexus and marketplace facilitator laws are complex and confusing.

Sales and use tax nexus affects all businesses that wish to sell into the U.S. It’s imperative that these businesses understand nexus to avoid penalties and fees associated with noncompliance. Furthermore, businesses that sell internationally can trigger the need to collect and remit customs duties and import/export taxes in other countries. Our 5 steps to managing VAT guide is a good starting point for understanding your obligations if you sell into places like Australia, the EU, India, or the U.K.

Your company may also have excise tax nexus or income tax nexus. The factors that trigger these obligations are different. For example, a company can have an obligation to collect and remit sales tax in a state where it has no income tax liability. And while sales tax is typically paid directly by consumers, excise tax is generally paid by businesses on sales and sales-related activities on certain products like alcohol, gas, or tobacco. Like sales tax, compliance rules for excise tax nexus can vary by state.

Failure to register in states where they have nexus is one of the top reasons businesses incur penalties from sales and use tax audits. We know understanding nexus can be tough, which is why we’ve developed this quick reference to help. Throughout this guide we outline what nexus is, what may trigger nexus, and how to keep up with your nexus obligations so you can stay in good standing with tax authorities.

More than 71% of respondents agree or strongly agree that online sales tax requirements including economic nexus and marketplace facilitator laws are complex and confusing.

Source: 2023 survey by Censuswide

What is nexus?

Nexus is the connection between a business and a taxing authority such as a state or local jurisdiction that establishes a tax obligation for the business. For example, if you have sales tax nexus in California and Texas, you must register to collect tax in those states, charge customers for sales tax using the correct rate, and pay the tax you owe as required.

CONNECTICUT

TRIGGER AND THRESHOLD:

$100,000 in sales and 200 transactions

INCLUDED TRANSACTIONS:

Gross receipts from taxable sales of tangible personal property including digital products and software as a service (SaaS), and sales through an online marketplace. Taxable and exempt services and exempt sales are included.

EXCLUDED TRANSACTIONS:

Sales for resale are not included in the sales threshold.

FLORIDA

TRIGGER AND THRESHOLD:

$100,000 in sales only

INCLUDED TRANSACTIONS:

Taxable sales of tangible personal property delivered physically into the state.

EXCLUDED TRANSACTIONS:

Taxable services, exempt sales, and exempt services are not included in the threshold.

TEXAS

TRIGGER AND THRESHOLD:

$500,000 in sales only

INCLUDED TRANSACTIONS:

Gross revenue from sales of tangible personal property and services into the state. Exempt sales and exempt services are included.

What triggers nexus?

So, what exactly triggers nexus? Unfortunately, there’s no one thing. Nexus has long been linked to physical presence, but even physical presence can be hard to measure. Due to the explosion of ecommerce sales and the Wayfair decision, physical presence is no longer the de facto standard for establishing nexus.

We’ve broken down some common activities that may establish a sales tax obligation for your business.

Did you know?

New Hampshire, Oregon, Montana, Alaska, and Delaware (also known as NOMAD states) are the only states that don’t have a general sales tax. However, some have local and county sales taxes.

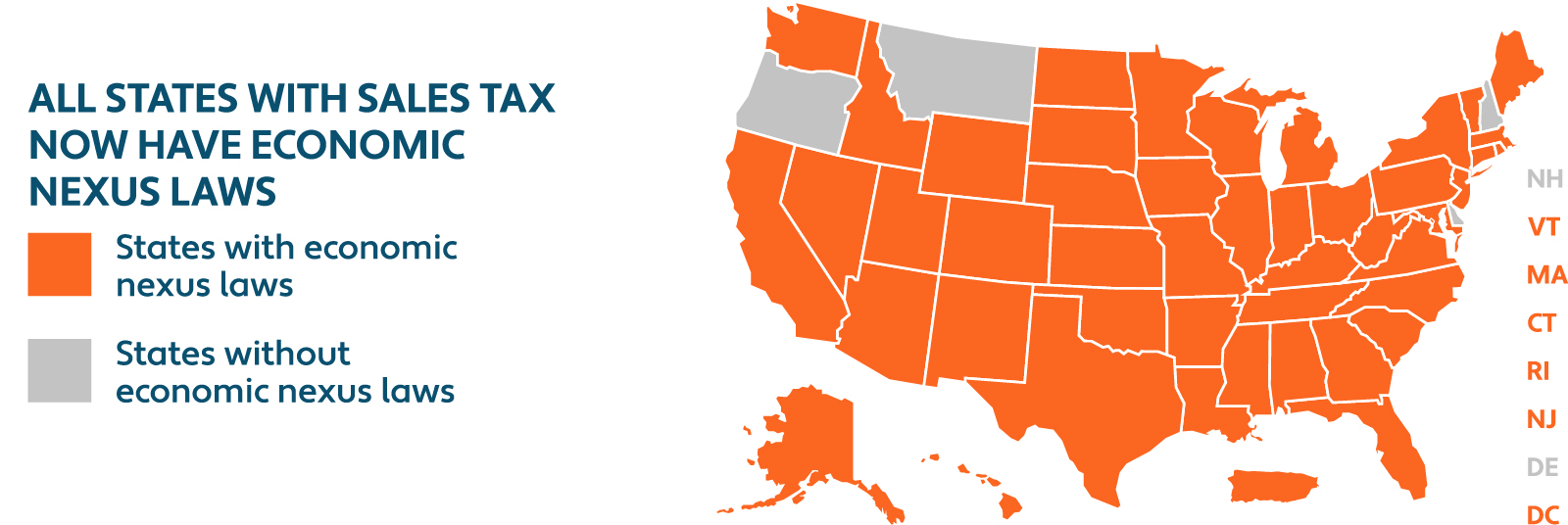

Economic nexus

Economic nexus bases a tax collection obligation on economic activity alone. As a result of the Wayfair decision, economic nexus laws have been adopted by every state with a sales tax, Washington, D.C., and some jurisdictions in Alaska.

Nexus thresholds vary by state and are subject to change. Many states use $100,000 in taxable sales or 200 separate sales transactions as the economic nexus threshold. But some states have higher thresholds, and several states base economic nexus on sales revenue only. Alabama’s threshold is $250,000 in taxable sales during the previous calendar year. In Washington, D.C., it’s $100,000 in taxable sales or 200 sales transactions in the current or previous calendar year. In New York, it’s $500,000 in taxable sales and 100 sales transactions during the previous four sales tax quarters. Some states include exempt sales and services in their thresholds.

Because of economic nexus laws, it’s important for businesses to actively monitor sales volumes in states where they’re not registered. It’s easy to exceed thresholds in one or more states, especially if you sell online or through multiple channels. Avalara Agentic Tax and Compliance™ continuously analyzes your sales across channels and shows where you’re approaching thresholds so you can spot nexus risk early and act before it becomes a problem. Review our state-by-state guide to economic nexus laws for more details on specific thresholds and rules.

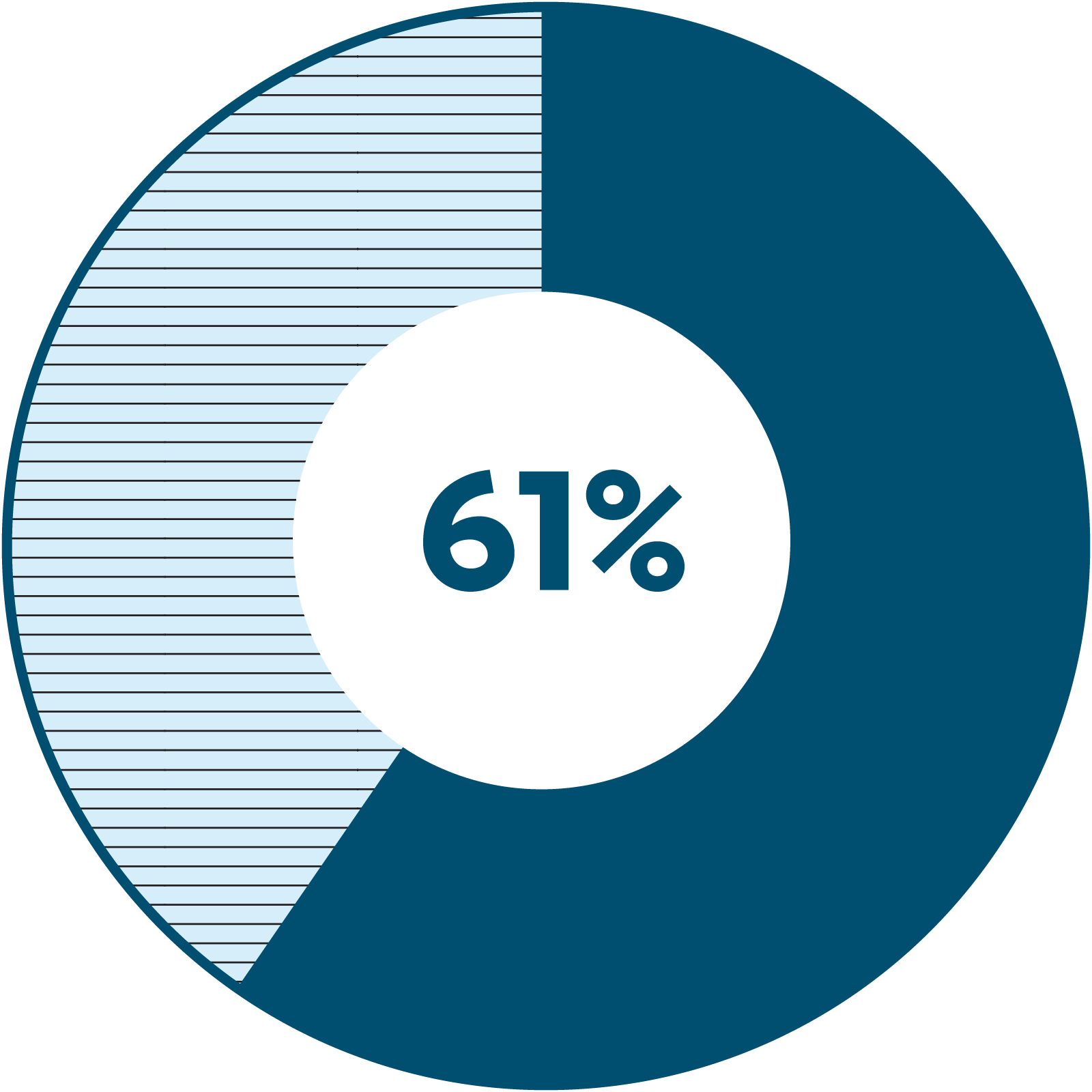

Fewer than 61% of businesses of any size who were surveyed claim to have implemented all required changes to be compliant with South Dakota v. Wayfair, Inc.

Source: 2023 survey by Censuswide

Marketplace facilitator laws

The rise of marketplace facilitator laws means that platforms where you sell goods or services, like Amazon, Etsy, and eBay, are now likely to collect and remit sales tax on your behalf. These laws shift the obligation to collect and remit sales tax from the seller to the platform that facilitates the sale. In most cases, the marketplace provider is required to collect and remit taxes if it meets economic nexus thresholds. Depending on the state, remote sellers should either include or exclude marketplace sales in their economic nexus threshold count. You may still need to register in certain states and file returns — even if no tax is due — while also managing any direct-to-consumer sales separately. For example, Connecticut requires remote sellers to register and file returns even when they only sell through a marketplace that collects and remits sales tax on their behalf.

The right tax compliance solution can automatically flag states where your direct sales and marketplace activity may push you over a threshold and help you understand where you must register. Agentic Tax and Compliance™ reconciles marketplace-reported sales with your own records and applies state-by-state rules for including or excluding marketplace sales in your economic nexus thresholds. Find more details in our guide, State-by-state registration requirements for marketplace sellers.

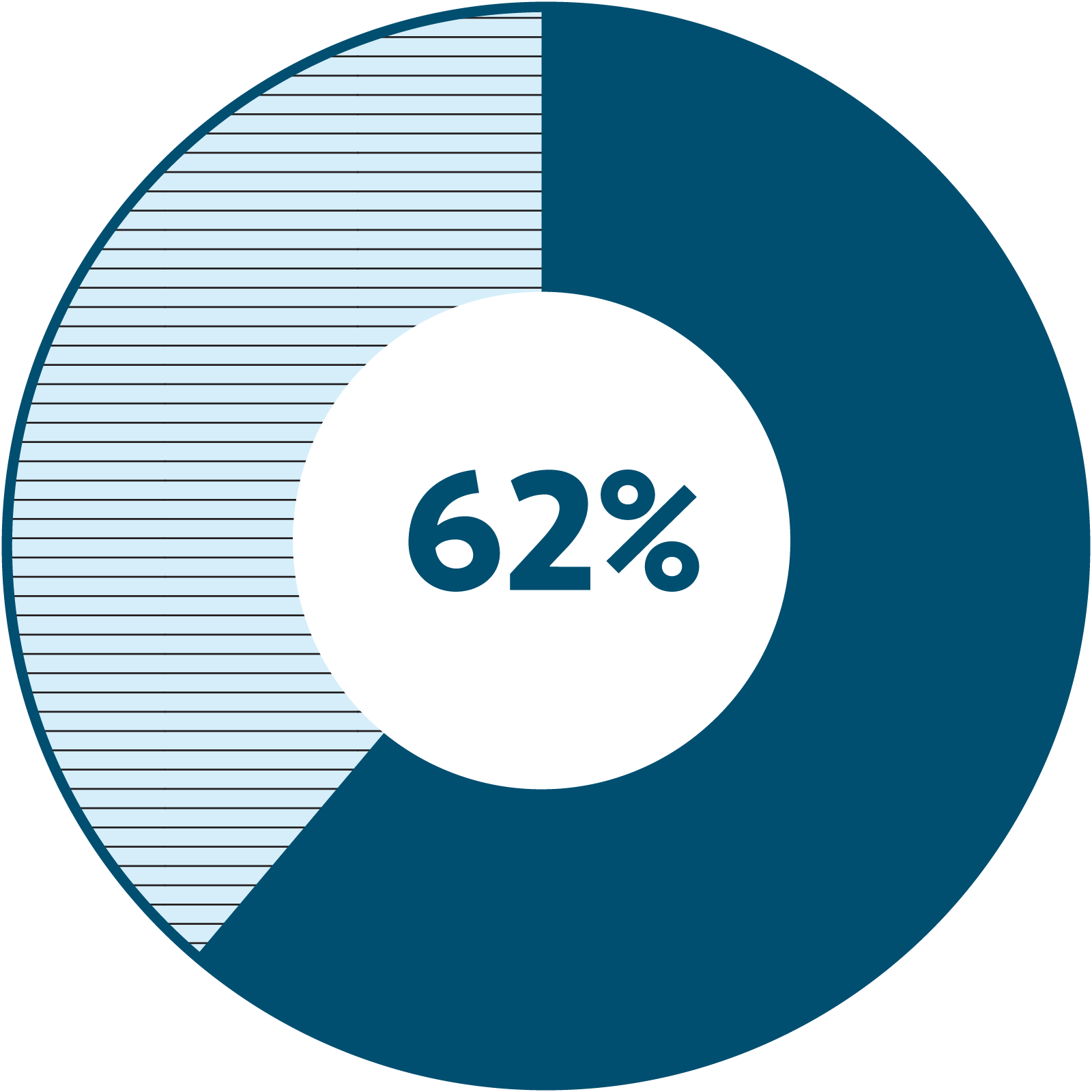

Fewer than 62% of businesses of any size who were surveyed claim to have implemented all required changes to be compliant with marketplace facilitator laws.

Source: 2023 survey by Censuswide

Physical presence

As you may expect, physical presence includes brick-and-mortar locations like branches, offices, stores, and warehouses. It can also include renting or owning property — even property located at a site owned by a third party. Having remote employees or contractors in a state, even temporarily, can trigger physical nexus, as can delivering goods in your own vehicle, or storing property in a location owned by someone else, such as a fulfillment center. Common triggers include:

Remote employees/sales representatives

Nexus is typically established once your business hires an employee. The same occurs when a team member moves to another state. If you’re not paying attention, you may unknowingly trip nexus in one or more states.

Nexus can also be created if you employ salespeople in different states and if your employees or contractors conduct any work at a customer’s out-of-state location, or even deliver products into another state. For example, in Colorado nexus can be established when a remote seller has employees in the state, “even if the activities of the employees are completely unrelated to the sales transaction at issue.”

Event attendance

Attending trade shows or other events in another state can also create sales tax nexus with that state. State rules vary, and some states take a more aggressive stance than others. To trigger nexus in Arizona, for example, an employee or independent contractor generally has to be in the state to solicit sales or establish a market for more than two days per year.

Remember, nexus laws can change. Before July 1, 2016, attending just one trade show in Washington state could trigger nexus. Since then, attendance or participation at one trade show each year doesn’t automatically establish nexus — although it could if an attendee is there to sell goods or take retail orders, or if the trade show is marketed to the general public.

Storing inventory

If your business stores inventory in a warehouse in another state, you may trigger nexus. In roughly 20 states, you can establish a physical presence even when the facility is owned by another party. This commonly occurs when businesses use a fulfillment center to process orders, such as Amazon FBA. And, unlike economic nexus, the obligation to collect sales tax starts from your first sale. To further complicate matters, a few states are trying to collect back sales taxes from marketplace sellers based on storing inventory in a marketplace facilitator’s warehouse.

Agentic AI and automation track physical presence nexus risk by continuously monitoring business activity, transaction data, entity footprints, and jurisdictional tax rules to identify where your company may trigger tax obligations. Avalara’s agentic AI platform combines physical presence information with economic nexus activity to provide a single, consolidated view of where you have nexus and why.

Nexus may be triggered even if you and your employees or shippers don’t step foot in another state. Agentic AI and automation apply jurisdiction-specific nexus rules to transaction and sales activity across connected systems to evaluate potential nexus exposure. Combined with continuously updated regulatory content and centralized reporting, Avalara helps finance and tax teams gain greater visibility into “hidden” nexus triggers where expanding sales-channel activity may create additional compliance obligations. For example:

Advertising

It’s now easier than ever for a business based in one state to advertise to potential customers in other states. Beware: Sometimes advertising across state borders can trigger a tax collection obligation. For example, advertising in newspapers or other periodicals printed in Virginia can trigger nexus, as can advertising on billboards or posters located there. Similarly, the regular or systematic solicitation of sales through marketing channels like television, radio, magazines, mail, and more can establish sales tax nexus in Texas.

In 2021, Maryland became the first state to adopt a digital advertising tax. Maryland’s law has been mired in legal battles, but that hasn’t stopped other states from proposing similar laws. These laws tax banner advertising, interstitial advertising, search engine advertising, and similar services. On the surface, it may sound simple to levy a tax whenever a person in a state views a digital ad. But since we take our smartphones everywhere, including across state lines, it may be difficult to pinpoint exactly where someone viewed the ad.

Did you know?

Tax obligations can be established through a connection to an in-state business or individual, including online advertising.

Affiliate nexus

Nexus can be established if an out-of-state retailer is affiliated with an entity that has sales tax nexus in another state. Affiliate nexus laws have been expanded in some states to include activities by unrelated parties that help out-of-state businesses generate or maintain a market in the state.

In New York, an out-of-state seller may have affiliate nexus if it uses in-state representatives to solicit business or otherwise help it develop or maintain a market in the state.

Click-through nexus

Under click-through nexus laws, your out-of-state business can establish a physical connection to a state through an agreement to reward a person for directly or indirectly referring potential buyers through links on a website.

The referrals must meet the state’s threshold to trigger nexus.

In most states, referrals must generate more than $10,000 in taxable sales during the preceding 12 months or four quarters.

Delivery and distribution

If you ship goods to customers by a common carrier such as the U.S. Postal Service, UPS, or FedEx, you’re unlikely to trigger sales tax obligations based on physical presence, but the sale may still count toward your economic nexus threshold in the state. Delivering products to customers in your own vehicle, however, can trigger physical nexus. An out-of-state business that sells to customers in New York and regularly uses its own vehicles for delivery has to register to collect and remit sales tax. Regular delivery means “at least 12 times a year.”

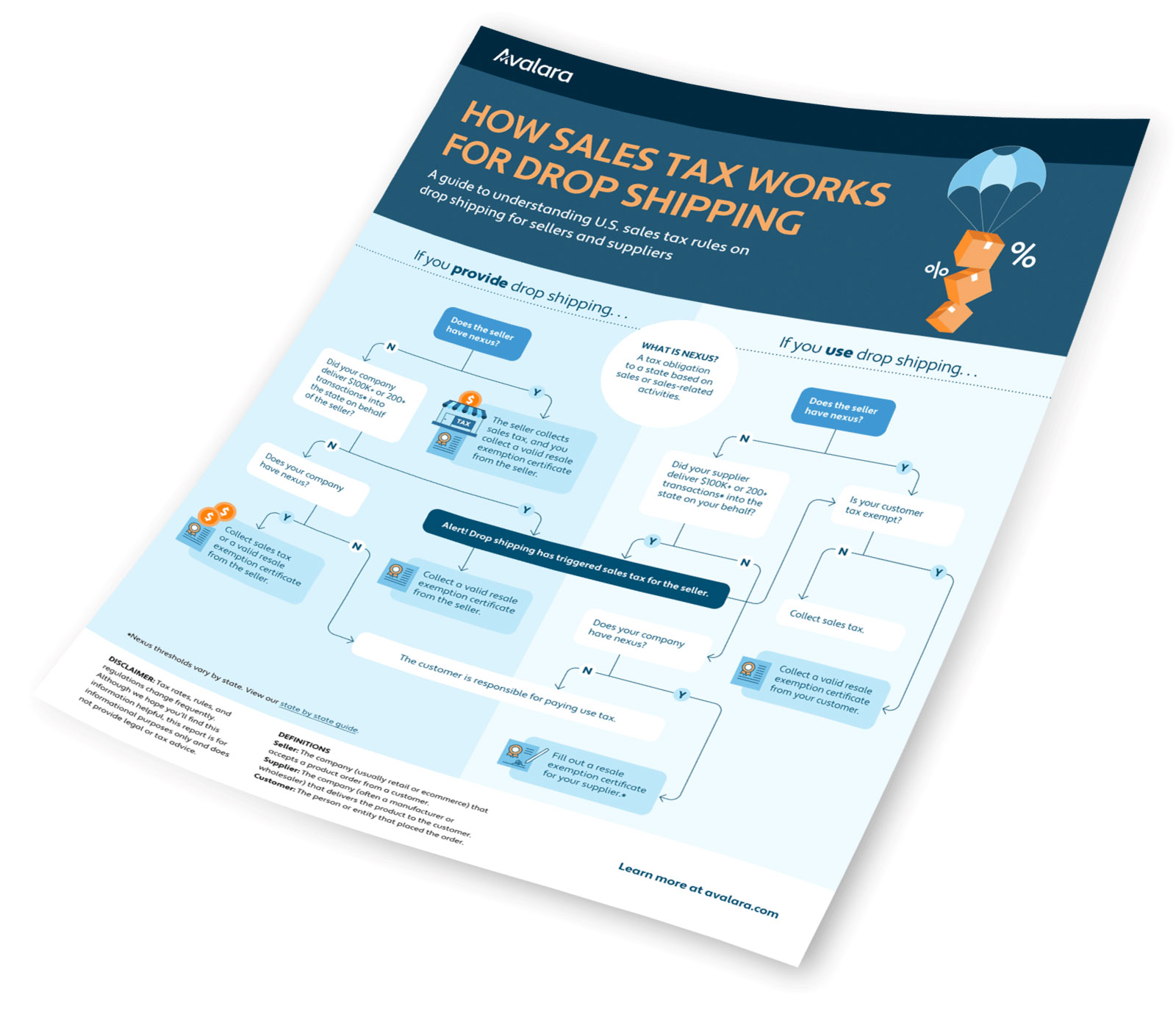

Nexus becomes complicated if you use a drop shipper. With drop shipping, a retailer doesn’t keep items in stock but orders them from a third party and has them shipped directly to the customer. As a result of economic nexus, businesses are increasingly impacted by drop shipping rules. But it’s not always apparent who’s responsible for collecting and remitting sales tax — the retailer, the supplier, or the drop shipper. And depending on the circumstances, retailers and drop shippers can be required to collect resale exemption certificates. Refer to our drop shipping reference guide for help.

Trailing nexus

Once you’ve established nexus in a state, it can linger longer than you might imagine. Nexus may continue even after you cease doing business or having a presence in a state, for a period that can last through the end of the calendar year or even longer. This is important to remember, especially if you trigger sales tax nexus through a temporary presence, like event attendance.

In Washington state, for example, a seller who stops nexus-creating activity continues to have nexus through the following calendar year.

Agentic AI and automation help businesses maintain visibility into nexus obligations as operations change over time. By analyzing historical transaction activity, registration status, filing history, and jurisdiction-specific tax rules across connected systems, Avalara helps surface ongoing compliance obligations that may otherwise be overlooked.

Nexus for international sellers

Understanding tax compliance for every country where you sell your products can be challenging, especially if you’re unfamiliar with local laws and languages. Thankfully, there are a few key steps that you can check off to help you remain in good standing with tax authorities.

- Determine the local tax of where you’re selling into.

- Check if you’ve crossed a border during your transaction. If you have, you must clear customs using a Harmonized System (HS) code to help identify any customs duties you may owe.

- Get your item code and HS code to identify what you owe and where it’s owed.

- Remit tax to the appropriate authority and store your documents for future reference.

You must make sure your business abides with each country’s local tax rules and regulations. International businesses need to realize that there are both differences and similarities between selling in the U.S. and selling into other countries. While value-added tax (VAT) in most countries around the world is charged at every stage of production, including manufacturing, distribution, and retail, sales tax in the U.S. is paid by the customer at the final sale of a product.

As you expand globally, your business must register with the appropriate tax authorities. For companies selling in the European Union, Import One-Stop Shop (IOSS) simplifies requirements by allowing businesses to register in just one EU state to sell into all 27.

To sell in the U.S., you must separately register with each state where you have nexus. It can be difficult to do alone because every state has its own application process and form. You can save time by turning to an outside vendor to handle the paperwork and register your business in all the states where you’re obligated to collect and remit sales tax.

There are also customs duties to consider if you’re selling across an international border. Countries have different de minimis thresholds, or values below which goods can be imported without being subject to customs duties or taxes. If your sales exceed the de minimis threshold, you’re liable for remitting the appropriate amount. Assigning the correct HS codes to your products will help you clear customs faster and avoid penalties.

In Europe, each country is a taxing jurisdiction. In comparison, there are more than 12,000 U.S. sales and use tax jurisdictions. They include states, counties, cities, and other municipalities with varying rates and rules. If you establish nexus, your business will need to calculate and collect sales and use tax, file returns, and pay tax to the appropriate jurisdiction. International sellers also have to consider U.S. sales tax exemptions and sales tax holidays. Normally taxable goods are temporarily exempt from sales and use tax during sales tax holidays.

Once registered, your business must submit returns and remit taxes.

Due to the rise of e-invoicing mandates and real-time reporting, many companies are required to issue and/or receive electronic invoices.

Automation can simplify international tax compliance and make it easier to meet your obligations. AI-driven solutions from Avalara identify correct HS codes, apply the right VAT and GST rates and rules, and validate, convert, and transmit billing data in requested e-invoice formats.

More U.K. businesses than U.S. businesses agree or strongly agree that economic nexus and marketplace facilitator laws are complex and confusing.

Source: 2023 survey by Censuswide

Excise tax nexus

Excise tax is charged on certain products such as tobacco, alcohol, and gasoline. Often, the tax is automatically added to the product’s price. Like sales tax, certain business activities can trigger excise tax nexus. However, compliance regulations and state rules vary.

For example, beverage alcohol tax laws are different depending on where you ship wine. Virginia requires businesses that ship wine directly to consumers to collect excise tax and sales tax. Massachusetts imposes excise tax but not sales tax on direct wine shipments. While remote wineries don’t need to register then collect and remit Florida sales tax unless they have economic nexus, they need to register for and collect and remit excise tax from the first sale.

Some communications services are also subject to excise tax nexus. The federal telephone excise tax is a 3% tax on local telecommunications services. Telephone companies collect the tax then pass it along to the Internal Revenue Service.

Hawaii was one of the first states to enforce economic nexus. The Aloha State has a general excise tax (GET) instead of sales tax. Businesses in Hawaii are required to pay GET on the gross receipts or gross income derived from their business activities in the state. Many companies pass along the tax to their customers.

Agentic AI and automation are making it easier for specialized industries to manage excise tax nexus obligations. Avalara offers purpose-built, complete solutions to handle tax compliance complexities for fuel and energy, tobacco and vape, communications, and beverage alcohol businesses.

How do you keep up?

If you made it this far, you know that nexus is tough.

It can be hard to understand the different types of nexus, and harder still to understand what they mean for your business. But knowing where you have nexus now, and where you could have nexus in the future, is crucial.

In short, getting nexus right takes a lot of time and dedicated effort. Unfortunately, if you don’t give state nexus laws the attention they demand, the consequences of noncompliance can cost you even more time and money.

Take our Avalara Sales Tax Risk Assessment to see if you overlooked any obligations to collect and remit sales tax.

DISCLAIMER

Sales tax rates, rules, and regulations change frequently. Although we hope you’ll find this information helpful, this report is for informational purposes only and does not provide legal or tax advice.

Connect with Avalara

You’re just a few steps from making tax compliance easier to manage, more accurate, and integrated into your business systems.

What to expect:

Connect with a sales tax specialist

Tell us which ERP, ecommerce platform, or accounting software you use and how you manage tax

We’ll connect you with the right person to demo our solution, provide a quote, and get you started