State-by-state guide to affiliate nexus laws

Guide sections

If you sell into states where you don’t collect sales tax, you need to be aware of affiliate nexus laws.

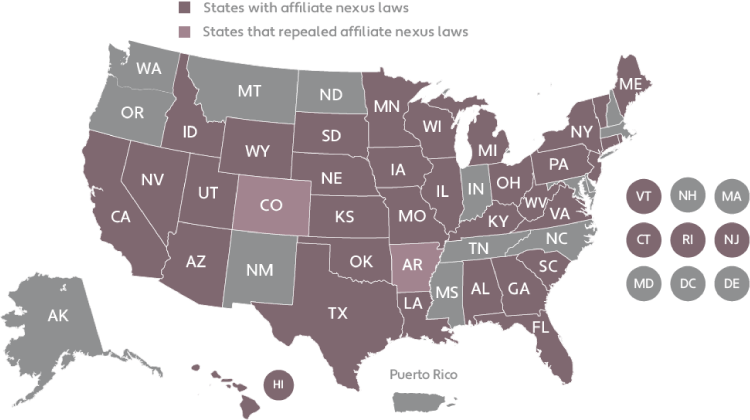

Affiliate nexus laws by state

as of May 6, 2019

Nexus is a connection between a state and a business that enables the state to impose a sales tax collection obligation on the business. For decades, nexus was limited to having a physical presence in a state. This prevented states from taxing the growing number of sales by out-of-state, internet sellers.

Affiliate nexus laws first emerged in 2008 as a creative response to the physical presence limitation. Under affiliate nexus laws, an out-of-state business establishes a physical connection through in-state affiliates, employees, representatives, or other entities. For there to be affiliate nexus, there needs to be a relationship between the entities — but the nature of the relationship varies a great deal from state to state.

More than 30 states have affiliate nexus laws, which may now be easier than ever to enforce. Although physical presence in a state still triggers nexus, states now also have the authority to tax remote sales: The physical presence limitation was overruled by the Supreme Court of the United States on June 21, 2018.

Below you’ll find a state-by-state breakdown of affiliate nexus laws. Bear in mind they’re subject to change, and affiliate nexus is just one of many ways to establish an obligation to collect and remit sales tax. For more information or assistance in determining your sales tax registration, collection, and remittance requirements, contact Avalara Professional Services.

Although we hope you’ll find the information helpful, this guide does not offer a substitute for professional legal or tax advice. If you have questions about your tax liability or concerns about compliance, please consult your qualified legal, tax, or accounting professional. This information was compiled in May 2019. Because states constantly update and amend their sales and use tax laws, see each state’s tax authority website for the most up-to-date and comprehensive information.

Reduce tax risk

Increase the accuracy of your tax compliance with up-to-date rates and rules with our cloud-based tax engine.

Alabama

Affiliate nexus may be established in Alabama when an out-of-state seller has ties to a business that maintains one or more locations in Alabama and engages in certain activities in the state, including: using a substantially similar name, trademark, or goodwill to develop, promote, or maintain sales; sharing a common business plan; or having the in-state affiliate provide services that benefit the out-of-state business’s ability to develop, promote, or maintain a market in Alabama. Learn more here and at Rule 810-6-2-.90.01.

Arizona

Affiliate nexus may be established in Arizona when an out-of-state seller uses independent contractors or other non-employee representatives in the state to establish and maintain a market for the out-of-state seller. Such representatives must be in the state for more than two days per year. In-state affiliates may also establish nexus for an out-of-state business by cross-promoting and advertising the business, by taking orders or accepting returns on behalf of the business, or by engaging in certain other activities. Learn more here.

Arkansas

Affiliate nexus may be established in Arkansas when an out-of-state seller has ties to businesses or affiliates in Arkansas that engage in certain activities in the state, including: selling a substantially similar line of products; using similar trademarks; or having in-state affiliates advertise, facilitate, provide services, or promote sales in the state on behalf of the seller. Learn more here.

Repealed effective July 1, 2019.

California

Affiliate nexus may be established in California when an out-of-state seller has ties to businesses or affiliates in California that engage in certain activities in the state, including: having a representative in the state to assemble, deliver, install, sell, or take orders for property; or being a member of a commonly controlled group that helps the seller establish or maintain a California market for sales of tangible personal property. Learn more here.

Colorado

Affiliate nexus may be established in Colorado when an out-of-state seller is part of a controlled group of corporations with a component member in Colorado that engages in certain activities, including: selling tangible personal property under a similar name, using a substantially similar trademark or trade names, or allowing customers to pick up property sold by the out-of-state retailer at a place of business in Colorado. Learn more here.

Connecticut

Affiliate nexus may be established in Connecticut when an out-of-state retailer has certain arrangements with affiliates located in Connecticut, including being directly or indirectly owned by a retailer engaged in a similar line of business in Connecticut. Learn more here.

Florida

Affiliate nexus may be established in Florida when an out-of-state retailer is a member of an affiliated group of corporations that has other members with nexus in Florida. This statute pertains specifically to mail-order sales. Learn more here.

Georgia

Affiliate nexus may be established in Georgia when an out-of-state retailer has certain arrangements with affiliates located in Georgia, including: selling the same line of products under a similar name; providing assembly, delivery, or maintenance services for the remote vendor’s Georgia customers; or conducting any other activities significantly associated with the out-of-state seller’s establishment or maintenance of a Georgia market. Learn more here.

Hawaii

Affiliate nexus may be established in Hawaii when an out-of-state retailer has an affiliate or representative in Hawaii that participates in a mutual merchandise return and loyalty points program with the out-of-state retailer. Learn more here.

Idaho

Affiliate nexus may be established in Idaho when an out-of-state retailer and an in-state business are related parties; in-state affiliates use a substantially similar name, trade name, or trademark, or provide services to help the out-of-state business develop, promote, or maintain the in-state market; and the out-of-state retailer had at least $100,000 in Idaho sales during the previous year. Learn more here.

Illinois

Affiliate nexus may be established in Illinois when an out-of-state retailer has a contract with a person in Illinois under which the out-of-state vendor sells a substantially similar line of products and uses a substantially similar name, trade name, or trademark as an in-state person; the out-of-state retailer pays a commission or other consideration to the person located in Illinois based on its sales of tangible personal property; and cumulative gross receipts from such contracts to Illinois customers exceed $10,000 during the preceding four quarterly periods. Learn more here.

Repealed effective June 28 2019; reinstated effective January 1, 2020.

Iowa

Affiliate nexus may be established in Iowa when a person with substantial nexus in Iowa engages in certain activities, including: selling a similar line of products as the remote retailer under a similar business name; using substantially similar trademarks, trade names, etc. as the remote retailer; or conducting any other activities in Iowa significantly associated with the remote retailer’s ability to establish and maintain a market in Iowa. Learn more here.

Kansas

Affiliate nexus may be established in Kansas when any person that makes taxable sales and has nexus in Kansas engages in certain activities, including: selling a similar line of products as the remote retailer under a similar business name; maintaining a location in Kansas to deliver or facilitate the sale or delivery of property sold by the remote retailer to consumers in Kansas; or conducting any other activities in the state significantly associated with the remote retailer’s ability to establish and maintain a market in the state. Learn more here.

Kentucky

Affiliate nexus may be established in Kentucky when an out-of-state retailer uses a representative in Kentucky to establish or maintain a marketplace for tangible personal property or digital property in the state for the out-of-state retailer. Learn more here.

Louisiana

Affiliate nexus may be established in Louisiana when an out-of-state retailer sells a substantially similar line of products as a Louisiana retailer; solicits business and develops and maintains a market in Louisiana through an affiliated agent who refers business for consideration of any kind; or holds a substantial ownership interest, directly or through a subsidiary, in a retailer maintaining sales locations in Louisiana, or by a parent or subsidiary thereof. Learn more here.

Maine

Affiliate nexus may be established in Maine when a person affiliated with an out-of-state retailer has a substantial physical presence in Maine or engages in certain activities in Maine, including: selling a similar line of products under a similar name; delivering, installing, or providing maintenance services for the remote seller’s customers in Maine; or conducting any activities in Maine that are significantly associated with the remote seller’s ability to establish and maintain a market in the state. Learn more here.

Michigan

Affiliate nexus may be established in Michigan when a person affiliated with an out-of-state retailer has a substantial physical presence in Michigan or engages in certain activities in the state, including: selling a similar line of products under a similar name; delivering, installing, or providing maintenance services for the remote seller’s customers in Michigan; or conducting any activities in Michigan that are significantly associated with the remote seller’s ability to establish and maintain a market in the state. Learn more here.

Minnesota

Affiliate nexus may be established in Minnesota when an in-state entity affiliated with an out-of-state retailer promotes or provides services for the remote retailer by engaging in certain activities in Minnesota. These include selling a similar line of products under a similar name; facilitating the delivery of tangible personal property to the remote retailer’s customers by allowing them to pick up the property at a business maintained by the entity; or sharing management, business systems, or employees with the remote retailer. Learn more here.

Missouri

Affiliate nexus may be established in Missouri when a person with nexus in Missouri engages in certain activities in the state on behalf of an out-of-state seller. These include selling a similar line of products under a similar name; facilitating the delivery of tangible personal property to the retailer’s customers by allowing them to pick up the property at a business location; or conducting any other activities in Missouri that enable the remote vendor to establish or maintain a market in the state. Learn more here.

Nebraska

Affiliate nexus may be established in Nebraska when an out-of-state seller is owned or controlled by the same interests that own or control any retailer engaged in business in the same or similar line of business in Nebraska. Learn more here.

Nevada

Affiliate nexus may be established in Nevada when an out-of-state retailer is part of a controlled group of business entities that has a component member with a physical presence in Nevada; and the component member engages in certain activities relating to the ability of the retailer to make retail sales to Nevada residents; and the component member conducts any other activities in Nevada that are significantly associated with the retailer’s ability to establish and maintain a market in Nevada. Learn more here.

New Jersey

Affiliate nexus may be established in New Jersey when an out-of-state retailer has independent contractors or other representatives acting as agents of the business in New Jersey. Learn more here.

New York

Affiliate nexus may be established in New York when a New York affiliate who is a sales tax vendor uses a trademark, service mark, or trade name that is the same as that used in New York by the remote affiliate; or a New York affiliate engages in activities in New York that help the remote affiliate develop or maintain a market for its goods or services in New York. Learn more here.

Ohio

Affiliate nexus may be established in Ohio when an out-of-state retailer is affiliated with an Ohio entity that engages in certain activities in Ohio. These include having any person, other than a common carrier acting as such, facilitate delivery by allowing a buyer to pick up the seller’s property at a place of business; or regularly using a person in Ohio to conduct business on behalf of the seller. Learn more here.

Oklahoma

Affiliate nexus may be established in Oklahoma when a person with substantial nexus in Oklahoma engages in certain activities in the state. These include using a similar trademark, service mark, or trade name as the out-of-state seller; selling a similar line of products under a similar name; or engaging in activities in Oklahoma that help the remote retailer develop or maintain a market for its products in Oklahoma. Learn more here.

Pennsylvania

Affiliate nexus may be established in Pennsylvania when an in-state entity affiliated with an out-of-state retailer promotes the remote retailer’s business or engages in certain activities in Pennsylvania. These include selling a similar line of products under a similar name as the remote retailer; or delivering the remote retailer’s property in Pennsylvania if delivery includes unpacking, positioning, or assembly. Learn more here.

Rhode Island

Affiliate nexus may be established in Rhode Island when an out-of-state retailer is related to a person with a physical presence in Rhode Island that engages in certain activities in the state. These include selling a similar line of products under a similar name as the remote retailer; delivering, installing, or providing maintenance services for the remote seller’s customers in Rhode Island; or sharing business activities and resources that help the remote seller establish or maintain a market in Rhode Island. Learn more here.

South Carolina

Affiliate nexus may be established in South Carolina when an out-of-state business is affiliated with an entity in South Carolina that sells similar tangible personal property or services in the state as the out-of-state seller and uses a common trade name, trademark, or logo; or accepts returns, takes orders, or performs customer service duties; or distributes advertising materials on behalf of the out-of-state business. Learn more here.

South Dakota

Affiliate nexus may be established in South Dakota when an out-of-state retailer holds a substantial ownership interest in or is owned in whole or in substantial part by, a retailer maintaining a place of business in South Dakota and the retailer engages in certain activities in the state. These include selling a substantially similar line of products under a substantially similar business name; or advertising, promoting, or facilitating sales by the retailer to a consumer in South Dakota. Learn more here.

Texas

Affiliate nexus may be established in Texas when an out-of-state retailer is affiliated with a retailer maintaining a place of business in Texas and the in-state affiliate engages in certain activities in the state. These include selling a similar line of products under a similar business name; advertising, promoting, or facilitating sales or doing other activities to establish or maintain a market in Texas for the retailer; or maintaining a distribution center or similar in Texas from which it delivers property sold by the out-of-state retailer. Learn more here.

Utah

Affiliate nexus may be established in Utah when an out-of-state retailer is affiliated with a retailer maintaining a place of business in Utah and the in-state and out-of-state businesses sell a similar line of products under a similar name; or the in-state affiliate advertises, promotes, or assists sales by the remote seller to a buyer in Utah; or if either the out-of-state or in-state retailer has more than 10 percent interest in the other or the affiliate wholly owns the retailer. Learn more here.

Vermont

Affiliate nexus may be established in Vermont if an out-of-state retailer owns or controls a person that is engaged in a similar line of business in Vermont. Learn more here.

Virginia

Affiliate nexus may be established in Virginia when an out-of-state retailer and a retailer maintaining a place of business in Virginia belong to a commonly controlled group, and the in-state entity maintains a distribution center, fulfillment center, office, warehouse, or other location in Virginia that facilitates the delivery of property sold in Virginia by the out-of-state retailer. Learn more here.

West Virginia

Affiliate nexus may be established in West Virginia when an in-state entity related to an out-of-state retailer engages in certain activities in the state, including: maintaining a distribution center, office, warehouse, or other place of business in West Virginia pursuant to an agreement with the remote retailer; performing services in connection with the sale of property or services by the remote retailer in West Virginia; or soliciting business on behalf of the remote retailer in West Virginia. Learn more here.

Wisconsin

Affiliate nexus may be established in Wisconsin if an out-of-state business is related to an affiliate in Wisconsin and the in-state affiliate uses employees or facilities in Wisconsin to advertise, promote, or facilitate the establishment of a market for the out-of-state retailer. It may also be established when an in-state affiliate provides services to Wisconsin purchasers on behalf of the out-of-state business. Learn more here.

Wyoming

Affiliate nexus may be established in Wyoming if an out-of-state business has a subsidiary in the state that advertises, solicits sales, or sells tangible personal property in Wyoming on behalf of the out-of-state seller. Learn more here.

Keep up with nexus obligations as your business changes

Affiliate nexus is one of the many ways your business can establish nexus: an obligation to register, collect, and remit sales tax in a jurisdiction. To see the other sales tax laws and nexus rules by state, view our sales tax laws by state resource.

If you’ve determined you have a new sales tax obligation due to affiliate nexus laws, the typical next step is to register your business with the jurisdiction. Avalara Licensing can help with that.